Japan’s largest beer company is giving the world a taste of its products through international acquisitions, resulting in a 9% Uniform ROA

Going to an izakaya, Japan’s version of pubs, has become a cultural unwinding habit in the country. With the help of a drink or two, izakayas have been a place for Japanese salarymen to let go of their pressures from work. This culture is one of the reasons why beer has become such a staple in the country.

This Japanese beer company went from almost experiencing bankruptcy to being Japan’s largest beer brand in terms of market share. Uniform Accounting reveals the success in its acquisition strategies that expanded its international exposure, with a Uniform ROA of 9% more than double what is reported.

Also below, Uniform Accounting Embedded Expectations Analysis and the Uniform Accounting Performance and Valuation Tearsheet for the company.

Philippine Markets Daily:

Wednesday Uniform Earnings Tearsheets – Asia-listed Focus

Powered by Valens Research

During the late 20th century, beer had begun overtaking sake as Japan’s most favored alcoholic beverage. Its rise to popularity is one of the sole reasons why Japanese beer brands have become so popular worldwide.

From a series of failed attempts at marketing and selling its brand, this sensational Japanese beer company has not only become the largest in market share in Japan’s beer industry, but has also become popular in the overseas beer industry as well.

The 1960s bore an economic boom within Japan, to which its beer industry saw a rapid increase in sales. Family incomes increased, changing consumption patterns. Consumers also started storing beers in their homes as electric appliances, like refrigerators, became more prevalent in Japanese households.

However, even during this time, Asahi continued to tap into restaurants, nightclubs, and izakayas for bulk orders instead of reaching out to retail consumers. In addition to that, Asahi did not have a concrete marketing strategy for selling their brand. As a result, inventories were just piling up and the company’s salespeople would resort to desperate attempts at approaching major clients to purchase bulk orders of their Asahi Gold.

Asahi Gold already had a bad reputation, having been described as having a rotten smell. The company continued to suffer from the sales slump and ultimately lost market share to Kirin Beer.

As Kirin Beer dominated the beer market in the 1970s-1980s, Asahi’s decline continued despite its marketing and sales efforts.

Asahi was already on the verge of bankruptcy before it released its game changer. Under new leadership during the 1980s, extensive research was conducted in order to adapt to the continuous evolution of consumer behavior.

In 1987, Asahi released its new beer, Asahi Super Dry, and the “nation’s beer landscape was transformed forever.” Not only was this particular beer aggressively advertised, but it was also the first Asahi beer produced from selected strains of yeast that provided outstanding fermentation. Consumers found the taste and aroma of Asahi Super Dry to be significantly more pleasant compared to the prior beers released.

After the release of the Asahi Super Dry, Asahi’s main strategy is to acquire several competitors in line with their plan to expand internationally. It started when the company released a low-malt beer Happo-syu that claimed it the top spot for shares of Japanese beer and low-malt markets.

Asahi’s thirst for success didn’t stop there as it continued its expansion by acquiring shochu and wine brands in 2002 to widen their market share. A year later, Asahi indulged itself into the foods and health care industries.

The firm’s M&A strategies extended outside of Japan. In 2009, it started acquiring multiple companies like Schweppes in Australia, Flavoured Beverages Groups Holdings Limited and Charlie’s Group Limited in New Zealand, and Etika Beverages Sdn Bhd in Malaysia.

To keep up with its goals for globalization, in 2016, former COO Akiyoshi Koji was appointed president, while then-president Naoki Izumiya was appointed Chairman. Yashushi Shingai, a former executive behind Japan Tobacco’s M&A strategies, joined Asahi’s board.

Just this June, Asahi completed its $11 billion purchase of AB InBev’s Australian unit Carlton & United Breweries. Today, Asahi is looking to expand its European beer portfolio, even after it purchased AB InBev’s European assets for $10 billion in 2016.

Owing to the firm’s strategy of mergers and acquisitions, it remains the #1 beer company in Japan.

Looking at Asahi’s results under as-reported metrics, it looks like its mergers and acquisitions did not translate to earnings for the company. Its as-reported ROA is currently below cost of capital at 4%.

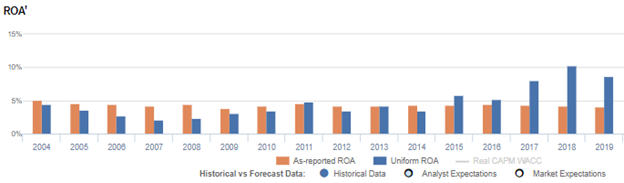

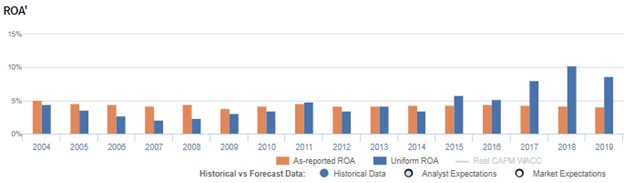

However, Uniform Accounting shows a more accurate representation of Asahi’s profitability. Although its Uniform ROAs were also below cost-of-capital levels in earlier years, the company is currently harvesting the fruits of its strategies as its Uniform ROA began surpassing cost-of-capital levels in 2015.

This proves that Asahi’s M&A strategies are now translating to profitability. Through this, the company now has a wider portfolio of brands and has expanded its global reach.

Because of these acquisitions, Asahi’s goodwill and other intangibles have reached an average of JPY 1.6 trillion in recent years, which is about half of Asahi’s total unadjusted assets. This is one of the things that as-reported metrics fail to consider.

Goodwill and other intangibles are purely accounting-based and unrepresentative of the company’s actual operating performance. When as-reported accounting includes this in a company’s balance sheet, it creates an artificially inflated asset base.

As a result, as-reported ROAs are not showing Asahi’s real earning power. After goodwill, other intangible assets, and other significant adjustments are made, the company actually had a 9% Uniform ROA in 2019, which is stronger than its below cost of capital as-reported ROA of 4%.

Asahi’s profitability is much better than you think it is

As-reported metrics are distorting the market’s perception of the firm’s profitability.

If you were to just look at as-reported ROA, you would think that the company is a weaker business than real economic metrics highlight.

Asahi’s Uniform ROA has been higher than its as-reported ROA in the past five years. For example, Uniform ROA is 9% in 2019, more than twice its as-reported ROA of 4%. When Uniform ROA was at 10% in 2018, as-reported ROA was only 4%.

The company’s Uniform ROA for the past five years has ranged from 5% to 10%, while as-reported ROA remained at 4% levels in the same time frame.

From 4% in 2004, Uniform ROA fell to 2% in 2008, before reaching a peak of 10% in 2018. Uniform ROA then reverted back to 9% in 2019.

Asahi’s Uniform earnings margins are weaker than you think but its robust Uniform asset turns make up for it

Volatility in Uniform ROA has been driven by trends in Uniform asset turns, and to a lesser extent by Uniform earnings margins, with peaks and troughs lining up historically with that of Uniform ROA.

From 6% in 2004, Uniform earnings margins declined to 3% in 2007, before peaking at 7% in 2018. It then fell to 6% in 2019.

Meanwhile, Uniform asset turns gradually expanded from 0.8x in 2004 to a peak of 1.5x in 2019.

SUMMARY and Asahi Group Holdings, Ltd. Tearsheet

As the Uniform Accounting tearsheet for Asahi Group Holdings, Ltd. (2502:JPN) highlights, its Uniform P/E trades at 26x, which is around corporate average valuation levels, but below its own recent history.

Average P/Es require average EPS growth to sustain them. In the case of Asahi, the company has recently shown a 21% Uniform EPS shrinkage.

Sell-side analysts provide stock and valuation recommendations that in general provide very poor guidance or insight. However, sell-side analysts’ near-term earnings forecasts tend to have relevant information.

We take sell-side forecasts for Japan’s Modified International Standards (JMIS) earnings and convert them to Uniform earnings forecasts. When we do this, Asahi’s sell-side analyst-driven forecast is a 35% earnings shrinkage in 2020, followed by a 49% earnings growth in 2021.

Based on the current stock market valuations, we can use earnings growth valuation metrics to back into the required growth rate to justify Asahi’s JPY 3,566 stock price. These are often referred to as market embedded expectations.

Asahi can have no Uniform earnings growth each year over the next three years and still justify current market expectations. What sell-side analysts expect for Asahi’s earnings is below what the current stock market valuation requires in 2020, but well above that requirement in 2021.

The company’s earning power is higher than the corporate average. Additionally, cash flows and cash on hand are below its total obligations. Together, this signals a high credit and dividend risk.

To conclude, Asahi’s Uniform earnings growth is below its peer averages in 2020. However, the company is trading in line with its peer valuations.

About the Philippine Market Daily

“Wednesday Uniform Earnings Tearsheets – Asia-listed Focus”

Some of the world’s greatest investors learned from the Father of Value Investing or have learned to follow his investment philosophy very closely. That pioneer of value investing is Professor Benjamin Graham. His followers:

Warren Buffett and Charles Munger of Berkshire Hathaway; Shelby C. Davis of Davis Funds; Marty Whitman of Third Avenue Value Fund; Jean-Marie Eveillard of First Eagle; Mitch Julis of Canyon Capital; just to name a few.

Each of these great investors studied security analysis and valuation, applying this methodology to manage their multi-billion dollar portfolios. They did this without relying on as-reported numbers.

Uniform Adjusted Financial Reporting Standards (UAFRS or Uniform Accounting) is an answer to the many inconsistencies present in GAAP and IFRS, as well as in PFRS.

Under UAFRS, each company’s financial statements are rebuilt under a consistent set of rules, resulting in an apples-to-apples comparison. Resulting UAFRS-based earnings, assets, debts, cash flows from operations, investing, and financing, and other key elements become the basis for more reliable financial statement analysis.

Every Wednesday, we focus on one company listed in Asia that’s relevant to the Philippines and that’s particularly interesting from a UAFRS vs as-reported standpoint. We highlight one adjustment that illustrates why the as-reported numbers are unreliable.

This way, we gain a better understanding of the factors driving a particular stock’s returns, and whether or not the firm’s true profitability is reflected in its current valuations.

Hope you’ve found this week’s Uniform Earning Tearsheet on an Asian company interesting and insightful.

Stay tuned for next week’s Asia company highlight!

Regards,

Angelica Lim

Research Director

Philippine Markets Daily

Powered by Valens Research

www.valens-research.com