MONDAY MACRO: Local recovery rates from COVID-19 are improving, but this Uniform Accounting rate is still declining at 56%

2020 has been a year of declines for economies around the world…declining GDP rates across the globe, declining interest rates from central banks, to name a few.

This often overlooked indicator is also on a decline, which is something to be concerned about especially in periods of economic turmoil such as today.

Philippine Markets Daily:

The Monday Macro Report

Powered by Valens Research

To control the spread of the coronavirus, many countries all over the world resorted to strict quarantine measures. These restrictions hampered GDP growth around the world as businesses operated at minimum capacity. Though many countries are still experiencing economic setbacks, there are some that have begun to recover, such as China and Japan recently.

Japan officially entered into a recession in Q1 2020 after recording a GDP contraction since Q4 2019. Prior to the pandemic, the third largest economy in the world had already been experiencing economic difficulties. Its GDP contracted further in Q2 2020 by 7.8%, its worst performance historically.

However, thanks to the Japanese government’s efforts, their economy exceeded expectations in Q3 2020 and rebounded with a 5% growth.

This improvement is a result of the government’s $296 billion stimulus funds, which accelerated domestic demand and exports. Stimulus funds are government expenditures that are given to the public in order to improve consumer spending. This type of fiscal policy improves business revenues when spent by the public, and stimulates economic activity in the process.

That said, analysts still remain cautious as Japan’s recovery could still weaken amidst a resurgence of the coronavirus infections in the country.

On the other hand, with arguably the world’s longest quarantine, the Philippines continued to struggle in Q3 2020 with GDP contracting by 11.5%.

With three consecutive quarters of negative GDP growth, various experts and local economic managers have forecasted an annual contraction of 7.8% to 9.5% for the Philippine economy in 2020. Experts are still expecting strong economic recovery in 2021 and 2022, however, as economic activities in the country pick up and a vaccine becomes available.

For now, the Philippine government’s fiscal prudence and slow spending have enabled monetary policy from the Bangko Sentral ng Pilipinas (BSP) to remain active amidst this economic recession. Because of this, analysts still expect the BSP to slash more interest rates similar to other central banks that have supported their economies by using expansionary policies.

In our previous Monday Macro report on inflation, we mentioned that the BSP has slashed rates five times this year. The cumulative 200bps rate cut has resulted in a historically low rate of 2%.

Unfortunately, lower interest rates may still not be enough to accelerate the Philippines’ economic recovery, especially given the local banks’ conservative approach to lending despite increased loan demand from businesses. Consumers, on the other hand, remain hesitant to borrow amid the uncertainty surrounding the pandemic.

We also mentioned that a low interest rate environment can significantly boost the economy because of lower borrowing costs, and businesses are more likely to expand their operations when the cost of acquiring funds is cheaper.

However, one of the drawbacks to having low borrowing costs is the amount of increasing debt. Normally that would be a reason for worry, but since banks have continued to tighten credit standards, quickly rising debt levels in the near term is unlikely.

Although we might not be expecting a spike in lending activities, we still need to watch out for the current level of debt against the assets that companies own. If businesses had to let go of some of their assets just to be able to continue operating, this might mean trouble for them if the economy continues to worsen.

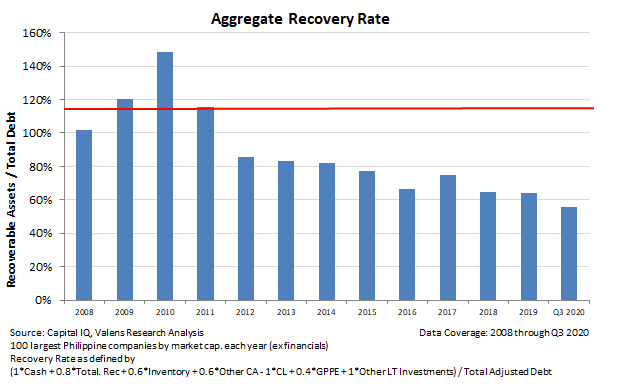

Using Uniform Accounting, we take a look at aggregate recovery rate, or firms’ ability to cover debt payments using their recoverable assets.

Recoverable assets, which include cash, total receivables, inventory, other current assets (less current liabilities), gross PP&E, and other long-term investments, are the numerator, while the denominator is total adjusted debt.

After expanding from 102% in 2008 to a peak of 148% in 2010, Philippine companies’ aggregate recovery rate remained above 60% through 2019. Thereafter, the rate declined to an all-time low of 56% as of Q3 2020. The recent decline was caused by the contraction of firms’ recoverable assets outpacing total debt contraction.

With limited alternatives because of the pandemic, companies are expected to turn to debt to survive. It’s important to note though a declining aggregate recovery rate increases the risk of higher loss given default (LGD), or the losses that lenders incur when borrowers default on their loans. The higher LGD will likely cause problems in the future because creditors may shy away from the increased credit risk, and businesses will have less accessibility to credit markets for additional capital.

So far, the BSP has been one of the most aggressive central banks in the world in terms of rate cuts. It has been actively adjusting its monetary policies to aid the country’s economic recovery.

Other monetary policies the BSP still has in its arsenal is the reserve requirement ratio (RRR) of 12%. Banks are currently required to hold a minimum of 12% of deposits that cannot be lended out. This is still a conservative rate, higher than neighboring countries’ single-digit rates. This means the BSP could still choose to adjust this rate lower to entice banks to increase their lending activities.

Though we continue to monitor the declining aggregate recovery rate, we remain positive about Philippine companies’ ability to bounce back from the recession. Philippine corporations still have ample amounts of liquidity from potential earnings and outlays to pay their financial obligations in the future. Combined with monetary tools from the BSP, the Philippines has the potential to recover from this recession faster than in previous recessions.

About the Philippine Market Daily

“The Monday Macro Report”

When just about anyone can post just about anything online, it gets increasingly difficult for an individual investor to sift through the plethora of information available.

Investors need a tool that will help them cut through any biased or misleading information and dive straight into reliable and useful data.

Every Monday, we publish an interesting chart on the Philippine economy and stock market. We highlight data that investors would normally look at, but through the lens of Uniform Accounting, a powerful tool that gets investors closer to understanding the economic reality of firms.

Understanding what kind of market we are in, what leading indicators we should be looking at, and what market expectations are, will make investing a less monumental task than finding a needle in a haystack.

Hope you’ve found this week’s macro chart interesting and insightful.

Stay tuned for next week’s Monday Macro report!

Regards,

Angelica Lim

Research Director

Philippine Markets Daily

Powered by Valens Research

www.valens-research.com