MONDAY MACRO: Uniform Accounting shows this important economic metric could recover to pre-pandemic levels sooner rather than later

This well-known measure is an aggregate of the monetary value of a country’s activities. With quarantines implemented around the world, a lot of these activities have declined to a large extent as businesses could not operate the way they used to.

Though there are still problems in the business environment due to the pandemic, thoughts of recovery have been entertained by investors this week as the PSEi has now reached 6,400 levels coming from a range of 5,700 to 6,000 levels in the past three months.

Whether this is just euphoria that is pushing the market upward, this metric provides insights as to whether or not this recent market rally has any economic basis.

Philippine Markets Daily:

The Monday Macro Report

Powered by Valens Research

China’s economy improved once again in Q3 2020, seeing growth for a second consecutive quarter. After contracting 10% in Q1 2020 on a quarterly GDP basis, China’s GDP growth turned positive in Q2 2020 with an 11.5% growth rate, faster than their G20 peers who all experienced a contraction.

Early epidemic control via strict lockdowns, work resumption, and government support were largely credited as reasons for China’s economy bouncing back early in Q2 2020. Meanwhile, strong export performance and infrastructure and real estate investments were the driving force behind the country’s Q3 2020 growth. The continued growth of both industrial production and retail sales also played a large part in its recovery for both quarters.

However, analysts remain concerned about the sustainability of the recovery because of the tensions with the U.S., the decline in the services sector, as well as the continued rise in corporate and household debt.

Though that might be the case, China’s economic recovery is still a tailwind for its trading partners, including the Philippines.

China is one of the Philippines’ largest export markets, accounting for over 20% of the Philippines’ total trade. In 2019, the top exports to China were (1) electrical and electronic equipment with $4.12 billion, (2) machinery, nuclear reactors, and boilers with $1.69 billion, (3) ores slag and ash with $9.81 billion, (4) edible fruits, nuts, peel of citrus fruit, melons with $810.29 million, and (5) copper with $668.98 million.

Thanks to China’s Q2 2020 economic recovery, Philippine exports to China also recovered. The continued growth of Philippine export demand there is therefore likely for Q3 2020. This is crucial to the Philippine economy as it diversifies revenue opportunities.

The global economy is also starting to show signs of a potential recovery as its contraction is slowing down. In its October 2020 World Economic Outlook update, the IMF estimates that the global economy would see a 4.4% contraction in 2020, a 0.5 percentage point improvement from its June estimates. This is then followed by a 5.4% annual GDP growth in 2021.

The Bangko Sentral ng Pilipinas (BSP) is also expecting improved domestic economic conditions. The monetary authority estimates Philippines’ balance of payments (BOP) for 2020 to improve as it expects to see a trade surplus of $8.1 billion. This surplus is driven by a lower contraction in goods exports (-16%) versus goods imports (-20%).

As a recap, a trade surplus occurs when a country’s exports exceed its imports. Due to the quarantine measures, restricted activities, and lower purchasing power, consumer demand for imported goods declined. However, the BSP expects that once the global economy returns to its pre-pandemic conditions, this surplus would be at a lower level as demand for imports increase.

Another reason for the surplus is a lower expected contraction in OFW remittances. Instead of seeing 5% less remittances, the BSP is expecting just 2% lower remittances for the rest of the year as other countries start to reopen their economies.

Despite the less pessimistic expectations for the Philippine local economy in 2020, the country’s GDP is still expected to post a 6% decline for the year at best. This is due to high unemployment rate, low consumer confidence, and the appreciation of the Philippine Peso versus the U.S. Dollar.

As we’ve mentioned in the past, recessions (defined as at least two consecutive quarters of economic contraction) are normally credit-driven events. The chart below shows that in the past 30 years, the Philippines has only experienced a recession twice.

The Philippines faced a recession from 1984 to 1986 during the Marcos administration, brought about by an increasing budget deficit, the difficulty of securing new capital, and the collapse of confidence and credit ratings from international financial institutions.

In 1991, the country had another recession after suffering a power crisis that caused major nationwide outages.

However, the Philippines did not experience a recession during any of the recent global economic crises such as the Asian Financial Crisis in 1997-1998 and the Global Financial Crisis in 2008, because of the country’s strong credit fundamentals.

What this shows is how resilient the Philippine economy is; that even when neighboring countries and trade partners experienced recessions, the Philippines was not negatively affected the same way. This is the first time the country has experienced a recession along with the rest of the world. Even so, as this was not a credit-driven recession, it is not expected to last as long as previous recessions did globally.

Going forward, recovery from the slump in 2020 is expected in 2021, assuming that the virus would be controlled by then, leading to the resumption of consumption activities.

The Philippine government should be able to support the country’s consumption spending through their various policies such as the Financial Institutions Strategic Transfer (FIST) bill, the Corporate Recovery and Tax Incentives for Enterprises (CREATE) bill, and the passage of the 2021 national budget.

While the FIST bill helps keep the credit flowing, the CREATE bill provides corporate income tax rate gradual reductions to support businesses, help generate jobs, and reduce poverty in the country. Furthermore, the national budget provides necessary projects to address the pandemic by focusing on the country’s healthcare systems while advocating economic recovery.

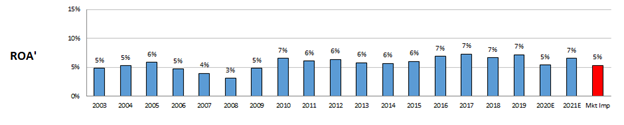

As previously mentioned in our August 10th Monday Macro on corporate debt, recovery from this recession is likely to be faster than credit-driven recessions the Philippines experienced in 1984-1986 and 1991. This is supported as well by the Uniform ROA, which points that overall Philippine corporate profitability is expected to recover to pre-pandemic levels by 2021.

With the combination of strong credit fundamentals and government support, the Philippines is capable of recovering fast as soon as the pandemic is controlled.

About the Philippine Market Daily

“The Monday Macro Report”

When just about anyone can post just about anything online, it gets increasingly difficult for an individual investor to sift through the plethora of information available.

Investors need a tool that will help them cut through any biased or misleading information and dive straight into reliable and useful data.

Every Monday, we publish an interesting chart on the Philippine economy and stock market. We highlight data that investors would normally look at, but through the lens of Uniform Accounting, a powerful tool that gets investors closer to understanding the economic reality of firms.

Understanding what kind of market we are in, what leading indicators we should be looking at, and what market expectations are, will make investing a less monumental task than finding a needle in a haystack.

Hope you’ve found this week’s macro chart interesting and insightful.

Stay tuned for next week’s Monday Macro report!

Regards,

Angelica Lim

Research Director

Philippine Markets Daily

Powered by Valens Research

www.valens-research.com