Philip Morris extinguishing their core product might be the key to sustaining robust ROA levels of 50%

With increasing regulations against smoking in the Philippines and globally, this company was able to turn a $3 billion alternative-to-cigarettes research venture into a lifeline for smokers everywhere.

As they continue to transition into non-smoking alternatives, their campaign strategy against their own product has been gaining momentum and TRUE UAFRS-based (Uniform) return on assets shows it.

Also below, Uniform Accounting Embedded Expectations Analysis and the Uniform Accounting Performance and Valuation Tearsheet for the company

Philippine Markets Daily:

Thursday Uniform Earnings Tearsheets – Global Focus

Powered by Valens Research

Philip Morris has to kill its main product in order to survive. That is, if it wants to survive in the long run.

It has long been proven that cigarette smoking provides no health benefits whatsoever. In fact, it provides the opposite. Frequent smoking can cause mild complications, organ failures, and even death.

So why do people continue to smoke?

The main ingredient of cigarettes is nicotine, a highly addictive substance that sends signals to activate dopamine, a “feel good” chemical in the brain. Most smokers continue to smoke because this sensation of happiness helps them forget for a moment the immense stress they are experiencing.

There are no universally easy and surefire ways to break the habit, but regulatory measures have been taken in order to lessen the use of cigarettes.

Cigarette advertising, for example, has been banned from most media platforms in countries like Brazil, Colombia, and the Philippines.

When it comes to packaging, some jurisdictions are stricter than others. Australia enacted a law that standardized the design of the boxes: olive-colored with only the brand name and health warnings printed on.

The Philippines has taken a similar route, though cigarette companies can keep its packaging with the caveat that photos of health complications be printed on the front.

Excise taxes have also been used as a prime tool for stifling cigarette demand.

In the back half of 2019, the Philippine Senate passed a bill increasing the excise tax on cigarettes. A pack now costs P5 more, to be increased by P5 annually until 2023. By 2024, price increases will be ramped up to 5% per year.

Other legislations are much harsher, however, going to lengths that outright ban the production and sale of cigarettes. Bhutan is the only country known to do so.

In the Philippines, smoking laws are less strict, but are strict nonetheless. Smoking in all public areas is now banned. A violation of this law could cost a hefty fine of P10,000 and prison time of up to a year.

With regulations becoming increasingly more strict, tobacco companies have to develop much less harmful, smoke-free alternatives to sustain operations.

In the case of Philip Morris, they’ve moved away from traditional cigarettes and into e-cigarettes—the IQOS.

This heated-not-burned tobacco device, although not risk-free, is the company’s solution towards a smoke-free future.

Last year, the company launched their “UnSmoke Your World” campaign, calling for non-smokers to stay away from cigarettes, for smokers to quit, and those who can’t quit to change.

Their anti-smoking efforts may seem counterintuitive to their business, when it’s really about them navigating consumers away from cigarettes and into IQOS. That way, regulatory scrutiny would lessen to a degree.

The transition from cigarettes to e-cigarettes has been successful. Over the course of three years, cigarette shipment volumes were down by 60 billion units while e-cigarettes have nearly doubled by the same amount.

While as-reported metrics don’t exactly show a company building a better, more sustainable business, Uniform metrics do.

As-reported ROA has come down from peak 24% levels in 2012 to just 16% in 2019. In reality, Philip Morris was able to sustain earning power with a robust Uniform ROA of 56%-58%.

Government intervention may have scared investors into thinking that the company’s earning power is weakening. But with IQOS serving as their lifeline, TRUE Uniform metrics would argue in favor of the company’s survivability.

Philip Morris’ earning power is actually more robust than what as-reported metrics would have you believe

As-reported metrics significantly understate Philip Morris International Inc.’s (PM:USA) profitability. For example, as-reported ROA for Philip Morris was 16% in 2019, which is about 4x lower than Uniform ROA of 56%, making Philip Morris appear to be a much weaker business than real economic metrics highlight

Moreover, as-reported ROA has slightly decreased from 20% in 2006 to current 16% levels, while Uniform ROA has expanded from 46% to 56% over the same period, significantly distorting the market’s perception of the firm’s historical profitability trends.

Historically, Philip Morris has seen robust, overall improving profitability. Uniform ROA increased from 48% in 2005 to peak 51%-62% levels in 2010-2012. It then fell to 42% in 2017 before rebounding to 56% in 2019.

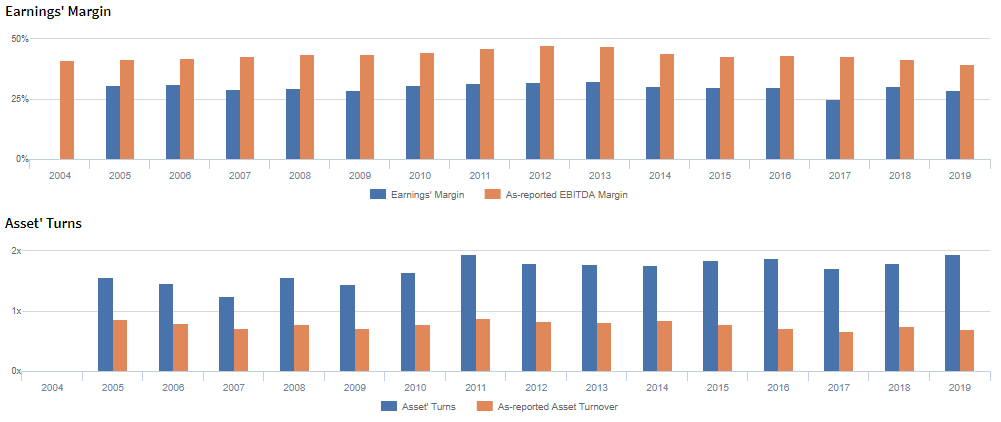

Philip Morris’ Uniform ROA is driven by significantly more robust Uniform asset turns but is offset by Uniform earnings margins

Trends in Uniform ROA have largely been driven by stability in Uniform Earnings Margin and trends in Uniform Asset Turns.

Since 2005, Uniform Margins have remained stable at 29%-33% levels, currently sitting at 29% in 2019.

Meanwhile, after falling from 1.6x in 2005 to 1.3x in 2007, Uniform Turns improved to 1.7x-1.9x levels from 2011 to 2019.

At current valuations, markets are pricing in expectations for continued stability in Uniform Margins, coupled with slight improvements in Uniform Turns.

SUMMARY and Philip Morris Tearsheet

As the Uniform Accounting tearsheet for Philip Morris highlights, the Uniform P/E trades at 17.9x, well below corporate average valuation levels and its own recent history.

Low P/Es require low EPS growth to sustain them. In the case of Philip Morris, the company has recently shown a 1% Uniform EPS growth.

Wall Street analysts provide stock and valuation recommendations that in general provide very poor guidance or insight. However, Wall Street analysts’ near-term earnings forecasts tend to have relevant information.

We take Wall Street forecasts for GAAP earnings and convert them to Uniform earnings forecasts. When we do this, Philip Morris’ Wall Street analyst-driven forecast is -7% into 2019. That rebounds with 24% growth in earnings from 2019 to 2020.

Based on current stock market valuations, we can use earnings growth valuation metrics to back into the required growth rate to justify Philip Morris’ $86 stock price. These are often referred to as market embedded expectations.

In order to justify current stock prices, the company would need to have Uniform earnings sustain the 2% decline each year over the next three years.

What Wall Street analysts expect for Philip Morris’ earnings growth falls far below what the current stock market valuation requires.

The company’s earning power, based on its Uniform return on assets calculation, is above average as well. Together, this signals low cash flow risk to the current dividend level in the future.

To conclude, Philip Morris’ Uniform earnings growth is slightly below peer averages in 2020. Also, the company is trading below average peer valuations.

About the Philippine Markets Daily

“Thursday Uniform Earnings Tearsheets – Global Focus”

Some of the world’s greatest investors learned from the Father of Value Investing or have learned to follow his investment philosophy very closely. That pioneer of value investing is Professor Benjamin Graham. His followers:

Warren Buffett and Charles Munger of Berkshire Hathaway; Shelby C. Davis of Davis Funds; Marty Whitman of Third Avenue Value Fund; Jean-Marie Eveillard of First Eagle; Mitch Julis of Canyon Capital; just to name a few.

Each of these great investors studied security analysis and valuation, applying this methodology to manage their multi-billion dollar portfolios. They did this without relying on as-reported numbers.

Uniform Adjusted Financial Reporting Standards (UAFRS or Uniform Accounting) is an answer to the many inconsistencies present in GAAP and IFRS, as well as in PFRS.

Under UAFRS, each company’s financial statements are rebuilt under a consistent set of rules, resulting in an apples-to-apples comparison. Resulting UAFRS-based earnings, assets, debts, cash flows from operations, investing, and financing, and other key elements become the basis for more reliable financial statement analysis.

Every Thursday, we focus on one multinational company that’s particularly interesting from a UAFRS vs as-reported standpoint. We highlight one adjustment that illustrates why the as-reported numbers are unreliable.

This way, we gain a better understanding of the factors driving a particular stock’s returns, and whether or not the firm’s true profitability is reflected in its current valuations.

Hope you’ve found this week’s Uniform earnings tearsheet on a multinational company interesting and insightful.

Stay tuned for next week’s multinational company highlight!

Regards,

Angelica Lim & Joel Litman

Research Director & Chief Investment Strategist

Philippine Markets Daily

Powered by Valens Research

www.valens-research.com