Smart acquisitions paired with a trendy marketing strategy brought this company back in style with Uniform ROAs that have gone up to new highs

Globalization has made it possible for companies to appeal to as many consumer groups as they want to. That means a one-size-fits-all marketing strategy isn’t an effective approach—different consumer groups require their own specific marketing message.

This clothing retail company follows a consumer-centric approach with its tiered-branding strategy. It has a myriad of brands, separate from its main brand, each tailored to a specific demographic.

While the impact of this strategy is not visible when looking at as-reported returns, Uniform Accounting shows that this has helped the company profitably tap into a larger consumer base, with Uniform ROAs that are twice the as-reported numbers.

Also below, Uniform Accounting Embedded Expectations Analysis and the Uniform Accounting Performance and Valuation Tearsheet for the company.

Philippine Markets Daily:

Thursday Uniform Earnings Tearsheets – Global Focus

Powered by Valens Research

For many years, fashion companies have used the one-size-fits-all marketing approach that tries to appeal to as many markets as possible. This is prevalent in leading apparel companies that rely on their brand values to provoke consumer recall and sentiment.

However, in this day and age of globalization and multiculturalism, this marketing approach no longer works because customers are now looking for products and services that help reflect their different personalities and beliefs.

This change in consumer behavior led to a shift to a consumer-centric marketing strategy that caters to people’s individualistic nature. This strategy targets specific consumer categories in order to provide them a personalized experience.

A straightforward example of this shift is the “one size fits most” sizing in clothing retailers such as Brandy Melville and Victoria’s Secret, among others. Because these companies carry only small sizes and are slow to embrace body inclusivity, competitors that adopted a consumer-centric approach like Aerie and ThirdLove, who have an extensive range of sizes, have gained market share.

Some companies like Lululemon (LULU) focus on providing an experiential element to customer shopping by enabling customers to interact with each other as well as with the business to create a sense of community. It’s marketing practices like these that open up new target demographics and potential for new revenue streams.

PVH Corp. (PVH) is also a company that uses this approach, although somewhat differently.

Originally a shirt-making business that started in 1881, PVH Corp. has established itself as one of the biggest players in the apparel industry. Under the brand are well-known names such as Tommy Hilfiger, Calvin Klein, Arrow, and IZOD, with the first two brands being major contributors to PVH’s growth.

Tommy Hilfiger is a high-end clothing brand known for its classic American preppy style. Its products also include fragrances, eyewear, watches, and furniture. It was acquired by PVH Corp. for approximately $3 billion in 2010, which then became the key to PVH’s entry into the premium lifestyle market.

Tommy Hilfiger currently uses the tiered branding strategy where a brand pulls in customers from different demographics by having several distinct lines under one name.

- Tommy Hilfiger is the main brand that targets consumers between 25 to 40 years old

- Hilfiger Denim is the more casual line that targets consumers between 18 to 30 years old

- Hilfiger Collection is a contemporary clothing line specifically targeted to women aged 25 to 40

- Tommy Hilfiger Tailored is similar to the Hilfiger Collection brand but is targeted for men

Calvin Klein, a fashion house under the Warnaco Group acquired by PVH in 2013, also uses the same branding strategy but serves a wider demographic range.

Calvin Klein has about 11 distinct brands including ones specifically for luxury wear, sportswear, casual wear, golf, home accessories, underwear, fragrances, and jewellery. Each of these lines enables the brand to be accessible to different consumer groups.

Overall, a consumer-centric approach to marketing works better than a one-size-fits-all approach when it comes to addressing as many consumer groups as possible.

Instead of having to rely on only one brand that may not be inclusive of the potential target markets, having multiple brands each tailored to a consumer group helps better connect with consumers personally. Today, this is what actually drives strong brand loyalty.

The Tommy Hilfiger and Calvin Klein acquisitions enabled PVH to execute this marketing strategy and subsequently tap into a larger consumer base and additional revenue streams. Those were also expected to translate into higher returns for the company.

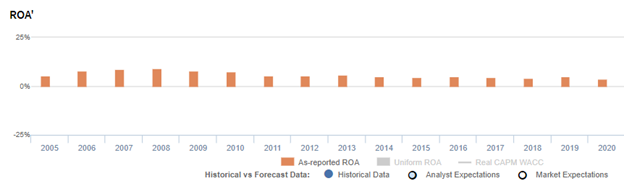

Upon looking at as-reported metrics, it seems that the major acquisitions and the execution of the marketing strategy have not translated into improving returns. Furthermore, return on assets (ROA) fell to around 4%-5% levels post-acquisition.

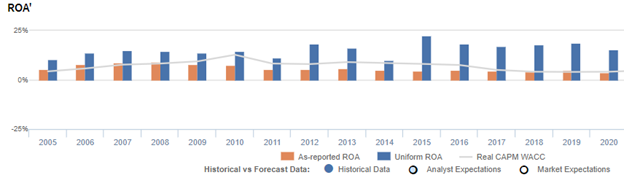

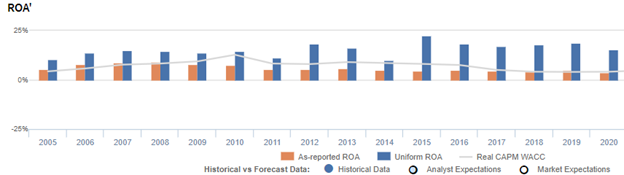

In reality, Uniform ROAs have gone up to new highs, rising to as much as 22% thanks to the brand acquisitions’ marketing success.

The distortion between Uniform and as-reported ROAs comes from as-reported metrics failing to consider the amount of goodwill on PVH’s balance sheet. The company’s goodwill sits at about $3 billion-$4 billion due to the aforementioned acquisitions and other acquisitions over the course of its operations.

Goodwill is an intangible asset that is purely accounting-based and unrepresentative of the company’s actual operating performance. When as-reported accounting includes this in a company’s balance sheet, it creates an artificially inflated asset base.

As a result, as-reported ROAs are not capturing the strength of PVH’s earning power. Adjusting for goodwill, we can see that the company isn’t actually displaying lackluster performance. In fact, it is the opposite, with returns that are around 3x greater.

PVH’s earning power is actually more robust than you think

As-reported metrics distort the market’s perception of the firm’s recent profitability. If you were to just look at as-reported ROA, you would think that the company is a much weaker business than real economic metrics highlight.

PVH’s Uniform ROA has actually been higher than its as-reported ROA in the past sixteen years. For example, as-reported ROA was 4% in 2019, but its Uniform ROA was actually significantly higher at 15%. When Uniform ROA peaked at 22% in 2015, as-reported ROA was only at 5%.

Specifically, PVH’s Uniform ROA has ranged from 10%-22% in the past sixteen years, while as-reported ROA has ranged only from 4%-9% in the same timeframe.

After expanding from 10% in 2005 to 15% levels in 2007-2008, Uniform ROA compressed to 11% in 2011, before jumping to 18% in 2012. Thereafter, Uniform ROA dropped back to 10% in 2014, before rebounding to 22% in 2015 and compressing to 17% in 2017. Then, Uniform ROA recovered to 19% in 2019, before declining to 15% in 2020.

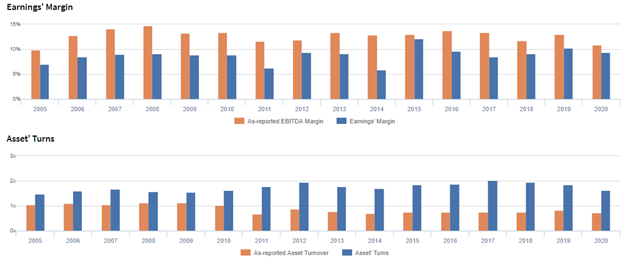

PVH’s earnings margins are overstated while asset turns are understated

PVH’s profitability has been driven by trends in both Uniform earnings margins and Uniform asset turns.

Uniform margins rose from 7% in 2005 to 9% levels in 2006-2014, excluding a 6% underperformance in 2011 and 2014, before further jumping to a peak of 12% in 2015. Then, Uniform margins fell to 9% in 2017 and recovered to 10% in 2019, before compressing back to 9% in 2020.

Meanwhile, after improving from 1.5x in 2005 to 1.7x in 2007, Uniform turns declined to 1.6x in 2008-2010, before rebounding to 2.0x in 2012. Subsequently, Uniform turns contracted to 1.7x in 2014, before expanding back to 2.0x in 2017 and finally falling to 1.6x by 2020.

At current valuations, markets are pricing in expectations for both Uniform earnings margin and Uniform asset turns to continue declining.

SUMMARY and PVH Corp’s Tearsheet

As the Uniform Accounting tearsheet for the PVH Corp. (PVH) highlights, its Uniform P/E trades at -105.2x, which is far below corporate average valuation levels and its own recent history.

Negative P/Es imply negative EPS growth. In the case of PVH, the company has recently shown a 3% Uniform EPS decline.

Wall Street analysts provide stock and valuation recommendations that in general provide very poor guidance or insight. However, Wall Street analysts’ near-term earnings forecasts tend to have relevant information.

We take Wall Street forecasts for GAAP earnings and convert them to Uniform earnings forecasts. When we do this, PVH’s Wall Street analyst-driven forecast is a 234% and a 156% EPS shrinkage in 2021 and 2022, respectively.

Based on current stock market valuations, we can use earnings growth valuation metrics to back into the required growth rate to justify PVH’s $84 stock price. These are often referred to as market embedded expectations.

The company can have Uniform earnings decline 3% each year over the next three years and still justify current prices. What Wall Street analysts expect for PVH’s earnings growth is far below what the current stock market valuation requires in 2021 and 2022.

Furthermore, the company’s earning power is 3x the corporate average. That said, intrinsic credit risk is 200bps above the risk-free rate. Together, this signals a moderate credit risk.

To conclude, PVH’s Uniform earnings growth is far below its peer averages in 2021, and the company is also trading far below average peer valuations.

About the Philippine Markets Daily

“Thursday Uniform Earnings Tearsheets – Global Focus”

Some of the world’s greatest investors learned from the Father of Value Investing or have learned to follow his investment philosophy very closely. That pioneer of value investing is Professor Benjamin Graham. His followers:

Warren Buffett and Charles Munger of Berkshire Hathaway; Shelby C. Davis of Davis Funds; Marty Whitman of Third Avenue Value Fund; Jean-Marie Eveillard of First Eagle; Mitch Julis of Canyon Capital; just to name a few.

Each of these great investors studied security analysis and valuation, applying this methodology to manage their multi-billion dollar portfolios. They did this without relying on as-reported numbers.

Uniform Adjusted Financial Reporting Standards (UAFRS or Uniform Accounting) is an answer to the many inconsistencies present in GAAP and IFRS, as well as in PFRS.

Under UAFRS, each company’s financial statements are rebuilt under a consistent set of rules, resulting in an apples-to-apples comparison. Resulting UAFRS-based earnings, assets, debts, cash flows from operations, investing, and financing, and other key elements become the basis for more reliable financial statement analysis.

Every Thursday, we focus on one multinational company that’s particularly interesting from a UAFRS vs as-reported standpoint. We highlight one adjustment that illustrates why the as-reported numbers are unreliable.

This way, we gain a better understanding of the factors driving a particular stock’s returns, and whether or not the firm’s true profitability is reflected in its current valuations.

Hope you’ve found this week’s Uniform earnings tearsheet on a multinational company interesting and insightful.

Stay tuned for next week’s multinational company highlight!

Regards,

Angelica Lim

Research Director

Philippine Markets Daily

Powered by Valens Research

www.valens-research.com