The merger between two powerhouse game developers won this Japanese company a Uniform return of 17%, more than 2x its as-reported!

It has been forty years since Pac-Man was released and yet it remains the best-selling arcade game series of all time.

The Japanese company behind Pac-Man believes that the engine of happiness revolves around dreams, fun, and inspiration. Its series of mergers and acquisitions through the years has allowed the firm to innovate in the gaming arena, supporting their core belief.

Even though the company has grown through strategic investments, its as-reported metrics can make investors think its acquisitions have not been synergistic. Uniform Accounting shows that this company has a stronger return on assets (ROA) than what the market thinks.

Also, below, Uniform Accounting Embedded Expectations Analysis and the Uniform Accounting Performance and Valuation Tearsheet for the company.

Philippine Markets Daily:

Wednesday Uniform Earnings Tearsheets – Asia-listed Focus

Powered by Valens Research

One of the industries doing well during the pandemic is gaming. Mobile games, online games, PC games…these are just some of the at-home activities that have seen spikes in users or sales amid the quarantines and lockdowns in various countries.

Even with all the new names, games, and technology popping out everywhere, there are still some classics that continue to do well in the digital age. Some of those classics even do well in their original consoles as people look back to retrogaming.

The 1980s was the golden age of arcade video games. People didn’t have personal devices for their games—they had to go to arcades to play games such as Pac-Man and Galaga as after school or work leisure activities.

The nostalgia for arcade games has paved the way for these to transition into PC and mobile games. For example, Apple recently launched Apple Arcade where consumers are given access to over 100 arcade games from various developers through a subscription service. In addition, Steam offers arcade games such as Tekken, which has an average of around 3,000 players daily.

Behind all of these known arcade games such as Pac-Man, Galaga, and Tekken is Bandai Namco Holdings Inc.

Bandai Namco Holdings Inc. is a corporate merger between Namco and Bandai on March 31, 2006.

The merger was made to address the tightening competition in the space, Japan’s decreasing birth rate that resulted in the slow growth of target customers, and the diversification of people’s hobbies and interests.

That wasn’t the first time Bandai went into talks about mergers.

In 1997, Bandai was supposed to be bought by Sega for around $1 billion to combine its operations and rebrand as Sega Bandai Limited. Hayao Nakamaya, the previous Sega President, was optimistic about the merger, even predicting that Sega Bandai Ltd. would be the world’s second-best entertainment company, only behind Walt Disney Corporation.

However, with the popularity of Bandai’s Tamagotchi, which sold over 12 million units in 1997, Bandai deemed it would not need Sega’s help to dominate the market. Moreover, 80% of Bandai’s middle managers were actually concerned about the cultural differences between Sega and Bandai if the merger between the two companies were to happen.

With both factors coming into play, Bandai retracted its statement approving the merger—a day after their board of directors approved it.

Fast forward to 2005, Bandai once again entered into talks of a merger, but this time with Namco. Both companies wanted to leverage their individual core strengths—Bandai’s specialty in character profiling and Namco’s game development capabilities—to increase their relevance to newer generations of consumers.

In 2006, this merger was completed.

In 2016, Bandai Namco released its most successful video game launch in its history with Dark Souls 3. The game reached a total sales of three million copies worldwide and had chart-topping UK sales in its first week.

This year, Bandai Namco opened its office for BANDAI NAMCO Mobile (BNM) in Barcelona. According to Nakaoti Katashima, CEO of BNM, the company is looking to venture in creating a “more flexible and collaborative content creation and marketing activities” that suits the needs of western audiences.

Today, Bandai Namco provides entertainment products and services across various platforms. It has managed to continue innovating while maintaining profitability at the higher end of its historical range.

Bandai Namco’s real economic profitability is better reflected with Uniform Accounting adjustments, which show its TRUE earning power.

What as-reported metrics fail to do is to consider the company’s excess cash on the balance sheet. While most companies inherently need some level of cash to operate, the portion of that balance that is earning limited or no return—or excess cash—ends up diluting as-reported ROAs.

If excess cash remains included in the company’s asset base in computing its performance metrics, the company’s profitability and capital efficiency may appear weaker than it actually is.

From 2005 to 2020, Bandai Namco has had a significant amount of excess cash sitting idly in its balance sheet, ranging from 18% to 35% of its unadjusted total assets.

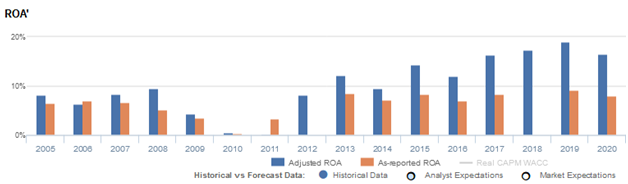

After excess cash and other significant adjustments are made, Bandai Namco’s Uniform ROA is at 17% in 2020, which is more than double its as-reported ROA of 8%.

Bandai Namco’s valuations are cheaper than you think

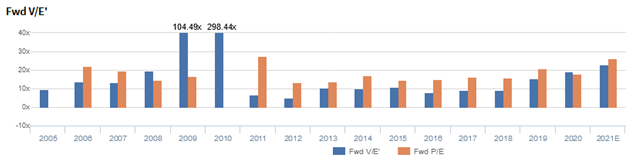

Bandai Namco Holdings Inc. (7832:JPN) currently trades around corporate averages, with a 22.9x Uniform P/E (blue bars), compared to its 26.1x as-reported P/E (orange bars).

At these levels, the market is pricing in expectations for Uniform ROA to stay at 17% levels in 2025, accompanied by a 2% Uniform asset growth going forward.

Meanwhile, analysts have more bullish expectations, projecting Bandai Namco’s Uniform ROA to improve to 19% by 2022, accompanied by a 2% Uniform asset shrinkage.

Bandai Namco’s profitability is much better than you think it is

As-reported metrics are distorting the market’s perception of the firm’s profitability.

If you were to just look at as-reported ROA, you would think that the company is a weaker business than real economic metrics highlight.

Bandai Namco’s Uniform ROA has actually been higher than its as-reported ROA in fifteen of the past sixteen years. For example, as-reported ROA was 8% in 2020, less than half its Uniform ROA of 17%. When Uniform ROA peaked at 19% in 2019, as-reported ROA was just at 9%.

The company’s Uniform ROA for the past four years has ranged from 16% to 19%, while as-reported ROA has ranged only from 0% to 9% in the same timeframe.

From immaterial levels in 2011, Uniform ROA gradually expanded to a peak of 19% in 2019, excluding 10% and 12% outliers in 2014 and 2016, respectively. Since then, Uniform ROA has declined to 17% in 2020.

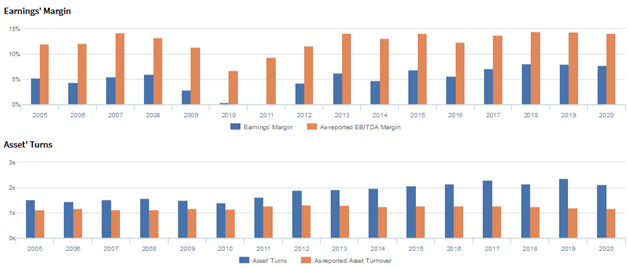

Bandai Namco’s Uniform earnings margins are weaker than you think but its robust Uniform asset turns make up for it

Volatility in Uniform ROA has been driven by trends in Uniform asset turns, with peaks and troughs lining up historically with that of Uniform ROA.

Uniform earnings margins fell from 5% in 2005 to immaterial levels in 2011, before rebounding to 8% peaks from 2018-2020.

Meanwhile, Uniform asset turns steadily rose from 1.5x in 2005 to 2.4x in 2019, before compressing to 2.1x in 2020.

SUMMARY and Bandai Namco Holdings Inc. Tearsheet

As the Uniform Accounting tearsheet for Bandai Namco Holdings Inc. (7832:JPN) highlights, the Uniform P/E trades at 22.9x, which is in line with corporate average valuation levels and below its own recent history.

Low P/Es require low EPS growth to sustain them. In the case of Bandai Namco, the company has recently shown a 6% Uniform EPS shrinkage.

Sell-side analysts provide stock and valuation recommendations that in general provide very poor guidance or insight. However, sell-side analysts’ near-term earnings forecasts tend to have relevant information.

We take sell-side forecasts for Japan’s Modified International Standards (JMIS) earnings and convert them to Uniform earnings forecasts. When we do this, Bandai Namco’s sell-side analyst-driven forecast is a 15% earnings shrinkage in 2021, followed by 39% growth in 2022.

Based on current stock market valuations, we can use earnings growth valuation metrics to back into the required growth rate to justify Bandai Namco’s JPY 6,491 stock price. These are often referred to as market embedded expectations.

Bandai Namco can have Uniform earnings grow by 2% in the next three years and still justify current prices. What sell-side analysts expect for Bandai Namco’s earnings is below what the current stock market valuation requires in 2021 but is above that requirement in 2022.

The company’s earning power is 3x the corporate average. Also, cash flows are 3x higher than its total obligations—including debt maturities, capex maintenance, and dividends. Together, this signals low credit and dividend risk.

To conclude, Bandai Namco’s Uniform earnings growth is well below its peer averages in 2020. However, the company is also trading above its peer valuations.

About the Philippine Markets Daily

“Wednesday Uniform Earnings Tearsheets – Asia-listed Focus”

Some of the world’s greatest investors learned from the Father of Value Investing or have learned to follow his investment philosophy very closely. That pioneer of value investing is Professor Benjamin Graham. His followers:

Warren Buffett and Charles Munger of Berkshire Hathaway; Shelby C. Davis of Davis Funds; Marty Whitman of Third Avenue Value Fund; Jean-Marie Eveillard of First Eagle; Mitch Julis of Canyon Capital; just to name a few.

Each of these great investors studied security analysis and valuation, applying this methodology to manage their multi-billion dollar portfolios. They did this without relying on as-reported numbers.

Uniform Adjusted Financial Reporting Standards (UAFRS or Uniform Accounting) is an answer to the many inconsistencies present in GAAP and IFRS, as well as in PFRS.

Under UAFRS, each company’s financial statements are rebuilt under a consistent set of rules, resulting in an apples-to-apples comparison. Resulting UAFRS-based earnings, assets, debts, cash flows from operations, investing, and financing, and other key elements become the basis for more reliable financial statement analysis.

Every Wednesday, we focus on one company listed in Asia that’s relevant to the Philippines and that’s particularly interesting from a UAFRS vs as-reported standpoint. We highlight one adjustment that illustrates why the as-reported numbers are unreliable.

This way, we gain a better understanding of the factors driving a particular stock’s returns, and whether or not the firm’s true profitability is reflected in its current valuations.

Hope you’ve found this week’s Uniform Earning Tearsheet on an Asian company interesting and insightful.

Stay tuned for next week’s Asia company highlight!

Regards,

Angelica Lim

Research Director

Philippine Markets Daily

Powered by Valens Research

www.valens-research.com