This cement company’s product innovations strategy brought Uniform earnings margin of 6%, not 19%

Today’s company participated in the Philippines’ construction boom by providing innovative building solutions through its concrete technology cement brands.

However, despite the strong cement demand and the firm’s innovation strategy, higher cement imports and tighter industry competition have disrupted the firm’s profitability, yet as-reported metrics continue to tag the company as a strong performing business.

Also below, Uniform Accounting Embedded Expectations Analysis and the Uniform Accounting Performance and Valuation Tearsheet for the company.

Philippine Markets Daily:

Tuesday Uniform Earning Tearsheets – Philippine-listed Focus

Powered by Valens Research

In the past decade, we have seen a continuing upward trend on the Philippine government’s construction activities even as the economy experienced several ups and downs. Amid the volatility, the cement industry has always been early beneficiaries from its recovery.

In our previous Philippine Market Daily articles, we’ve discussed the strategies of two major contributors of construction materials in the Philippines: Eagle Cement (EAGLE:PHL) with its focus on production, and CEMEX Holdings (CHP:PHL) with its product differentiation.

Today, we are going to talk about another major contributor, Holcim Philippines, Inc. (HLCM:PHL).

Holcim has an extensive portfolio of innovative solutions and a wide range of products from structuring to finishing applications. These products help local builders efficiently execute projects from massive infrastructure to simple home repairs.

With cement manufacturing facilities in La Union, Bulacan, Misamis Oriental, and Davao, as well as aggregates and dry mix business and technical support facilities for building solutions, Holcim’s operations are spread all over the country.

One of Holcim’s major clients is the Philippine government. So when the government cut back on infrastructure spending in 2011, the company’s as-reported earnings margin shrank from 30% in 2010 to 19%.

In 2014, the Philippine government increased its budget allocation for infrastructure development to PHP 399.4 billion, an increase of 36% compared to the previous year’s number.

Holcim took advantage of this growth opportunity by reactivating its cement grinding facility in Batangas and preparing for a new production line in Bulacan.

In addition, Holcim’s management improved their operational efficiencies and cost management. As a result, Holcim’s as-reported margins improved to 26% that year and then slightly improved to 27% in 2016.

In 2017, the new administration launched the “Build Build Build” program in an attempt to accelerate infrastructure projects in the country and attract more foreign investments.

Unfortunately, more foreign investments coming in meant more competition for the cement industry. Holcim’s cement prices plunged due to the influx of imported cement, causing its revenues to fall by 13.9% to PHP 34.7 billion.

As a result of these challenges, Holcim shifted its focus from improving production and distribution to concentrating on product innovations and customer-focused solutions.

In 2018, the firm launched its concrete technology cement brand, Superfast-Crete, a one-day concrete technology for quick road repairs in highly-urban areas.

Then, in 2019, it introduced Holcim Solido, a higher-quality alternative for infrastructure building over the commonly used ordinary portland cement in terms of strength, durability, workability and sustainability.

These efforts helped the company partially recover its profitability in 2019.

Furthermore, in January 2020, the company launched its first digital platform, EasyBuild, to increase its customer engagement and service to cater to the trend of online e-commerce opportunities.

However, the pandemic halted construction activities for much of the year, disrupted supply chains, and lowered cement prices, causing Holcim’s margins to decline in 2020.

Despite the recent setbacks, the firm’s innovation strategy and series of product launches would make it seem like it is a strong-performing business, with as-reported earnings margin reaching a peak of 33% levels in the past sixteen years.

In reality, higher cement imports and tighter industry competition have actually disrupted the firm’s profitability, with Uniform earnings margin only reaching a peak of 15% in the same time frame.

When the government cut its infrastructure budget allocation in 2011, margins didn’t shrink to 19% from 30%, it actually fell to 4% from 11%. When business improved in 2016, margins actually improved to just 15%, not 27%.

What as-reported financials have gotten wrong is the depreciation of the company’s fixed assets.

Depreciation expense is a non-cash expense, meaning it does not represent an actual outlay of cash. Also, it can be easily manipulated by changing the asset’s life. As such, depreciation expense should be removed from earnings.

As a capital-intensive firm, Holcim needs to spend on maintaining its facilities. However, for other industries, this expense barely shows up on the balance sheet.

To arrive at an estimate of the firm’s maintenance capex, what is done instead is smoothing as-reported depreciation expense over a few years, adjusting for inflation and asset impairments.

In 2020 alone, Holcim recorded PHP 2 billion of depreciation expense, but its substantial growth in assets that year warranted PHP 478 million in maintenance capex.

Adding back depreciation expense and subtracting maintenance capex, along with the many other necessary adjustments made leads to just PHP 1.6 billion in Uniform earnings and a 6% Uniform earnings margin in 2020, much lower than as-reported earnings of PHP 2.1 billion and 19% EBITDA margin.

Holcim’s earning power has historically been weaker than you think

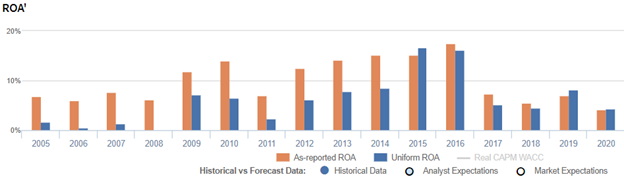

As-reported metrics distort the market’s perception of the firm’s historical profitability. If you were to just look at as-reported ROA, you would think Holcim’s profitability has been stronger than real economic metrics have highlighted in thirteen of the past sixteen years.

In reality, Holcim’s true profitability has generally been lower than its as-reported ROA from 2005-2018 excluding outperformance in 2015. Meanwhile, in the last two years, Uniform ROA has been slightly above as-reported ROA.

Holcim’s earnings margin is weaker than you think

Trends in Uniform ROA have been primarily driven by trends in Uniform earnings margin.

After falling from 33% in 2005 to 23% in 2008, as-reported margins jumped to 30%-31% levels in 2009-2010. Then, as-reported margins compressed again to 19% in 2011 before improving to 27% levels by 2016. Thereafter, as-reported margins declined to 14% before bouncing back to 21% in 2019. Since then, as-reported margins dropped yet again to 19% in 2020.

Meanwhile, Uniform margins plunged from 5% in 2005 to immaterial levels in 2008, before expanding to 12% in 2009 and sinking again to 4% in 2011. Since then, Uniform margins soared to 15% levels in 2015-2016 before gradually declining to 6% in 2020.

Looking at the firm’s margins alone, as-reported data makes the firm appear to be less efficient with its cost than real economic metrics highlight.

SUMMARY and Holcim Philippines, Inc. Tearsheet

As the Uniform Accounting tearsheet for Holcim Philippines, Inc. (HLCM:PHL) highlights, it trades at a Uniform P/E of 18.6x, below the global corporate average of 23.7x and its historical average of 27.3x.

Low P/Es require low EPS growth to sustain them. In the case of Holcim, the company has recently shown a 50% Uniform EPS decline.

Sell-side analysts provide stock and valuation recommendations that in general provide very poor guidance or insight. However, sell-side analysts’ near-term earnings forecasts tend to have relevant information.

We take sell-side forecasts for PFRS earnings and convert them to Uniform earnings forecasts. When we do this, Holcim’s sell-side analyst-driven forecast calls for an immaterial EPS growth in 2021 followed by a 2% EPS growth in 2022.

Based on current stock market valuations, we can use earnings growth valuation metrics to back into the required growth rate to justify Holcim’s PHP 5.47 stock price. These are often referred to as market embedded expectations.

Holcim is currently being valued as if Uniform earnings were to shrink by 3% annually over the next three years. What sell-side analysts expect for the company’s earnings growth is above what the current stock market valuation requires in 2021 and 2022.

Holcim’s earning power is below the long-run corporate average. Furthermore, cash flows and cash on hand are 3x its total obligations—including debt maturities, capex maintenance, and dividends. Also, intrinsic credit risk is 300bps above the risk free rate. Together, this signals a low dividend risk and moderate credit risk.

To conclude, Holcim’s Uniform earnings growth is below peer averages in 2020 and the company is trading in line with its average peer valuations.

About the Philippine Markets Daily

“Tuesday Uniform Earnings Tearsheets – Philippine-listed Focus”

Some of the world’s greatest investors learned from the Father of Value Investing or have learned to follow his investment philosophy very closely. That pioneer of value investing is Professor Benjamin Graham. His followers:

Warren Buffett and Charles Munger of Berkshire Hathaway; Shelby C. Davis of Davis Funds; Marty Whitman of Third Avenue Value Fund; Jean-Marie Eveillard of First Eagle; Mitch Julis of Canyon Capital; just to name a few.

Each of these great investors studied security analysis and valuation, applying this methodology to manage their multi-billion dollar portfolios. They did this without relying on as-reported numbers.

Uniform Adjusted Financial Reporting Standards (UAFRS or Uniform Accounting) is an answer to the many inconsistencies present in GAAP and IFRS, as well as in PFRS.

Under IFRS, each company’s financial statements are rebuilt under a consistent set of rules, resulting in an apples-to-apples comparison. Resulting UAFRS-based earnings, assets, debts, cash flows from operations, investing, and financing, and other key elements become the basis for more reliable financial statement analysis.

Every Tuesday, we focus on one Philippine-listed company that’s particularly interesting from a UAFRS vs as-reported standpoint. We highlight one adjustment that illustrates why the as-reported numbers are unreliable.

This way, we gain a better understanding of the factors driving a particular stock’s returns, and whether or not the firm’s true profitability is reflected in its current valuations.

Hope you’ve found this week’s Uniform Earnings Tearsheet on a Philippine company interesting and insightful.

Stay tuned for next week’s Philippine company highlight!

Regards,

Angelica Lim

Research Director

Philippine Markets Daily

Powered by Valens Research

www.valens-research.com