This Chinese company is taking advantage of the biotech trends in its home country through acquisitions and partnerships, resulting in a 39% ROA

With the expansion trend of Chinese CMOs, this company took part in strategic joint ventures and acquisitions aimed to put the company in a favorable position to compete in China’s pharmaceutical market.

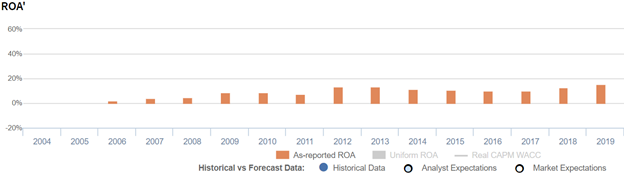

However, as-reported metrics are indicating a lackluster performance, with return on assets (ROA) just above cost of capital. With Uniform Accounting, we can see an entirely different story, with Uniform returns reflecting more than double the as-reported returns.

Also below, Uniform Accounting Embedded Expectations Analysis and the Uniform Accounting Performance and Valuation Tearsheet for the company.

Philippine Markets Daily:

Wednesday Uniform Earnings Tearsheets – Asia-listed Focus

Powered by Valens Research

In one of our previous PMDs, we mentioned that China’s pharmaceutical industry is the second largest in the world in terms of annual pharmaceutical revenues. The industry is said to garner more than 10% of the total sales worldwide.

We also mentioned that around 25 biologics and biosimilar products were approved in China in 2020, and that there are approximately 1,000 clinical trials that investigate several biologics and biosimilars focusing on treating a number of diseases.

China’s pharmaceutical industry has seen continuous growth, and the demand for biopharmaceuticals around the world is also increasing. These factors have led to the rise of China-based contract development and manufacturing organizations (CDMOs) and contract manufacturing organizations (CMOs).

China-based CMOs have begun expanding their manufacturing-related capabilities in order to attract global clients and keep up with the highly competitive market. Partnering with these China-based service providers means foreign companies may enjoy benefits like relatively low labor costs, access to a huge consumer base, and a more lenient regulatory environment.

Through these efforts, a number of joint ventures, partnerships, and strategic acquisitions were made.

Today’s company is participating in that trend.

Changchun High & New Technology Industries Inc. (CCHT) is a China-based company that engages in research development, production, and sale of biopharmaceuticals and proprietary Chinese medicines.

One of CCHT’s subsidiaries, Changchun BCHT Biotechnology, known for developing biological vaccines and genetically engineered drugs, has been involved in international partnerships. In 2014, it partnered with Mucosis B.V., a biotech company in the Netherlands, for its SynGEM® prefusion F vaccine and the Mimopath® platform.

Historically, the company has invested through private placements with several other Chinese biopharmaceutical and biotechnology companies, like Guangzhou Si’anxin Biotechnology Co., Shanghai RuiZhouBio Biotechnology Co., and Xian Aidewansi Medical Technology Co., to name a few.

As for partnerships with foreign companies, CCHT has employed a mix of private placements, acquisitions, and joint ventures.

In 2019, CCHT established a joint venture with Alvotech, which strategically enables the latter company to conduct operations in China. Through the Alvotech & CCHT Biopharmaceutical JV, Alvotech could develop, manufacture, and commercialize its biosimilar portfolio in China.

In exchange, Alvotech reportedly contributed capital and authorizations in six drug markets amounting to USD 100 million, for the development of monoclonal antibodies used in advanced therapy for cancer and several autoimmune illnesses.

That same year, CCHT acquired GeneScience Pharmaceuticals (GenSci), which already has an established presence in several international markets like Hong Kong, Pakistan, Peru, Macau, among others.

In 2020, CCHT agreed to invest USD 28.3 million in the U.S.-based company Brillian Pharma Inc.

Given the company’s strategic partnerships and acquisition in order to take advantage of the current manufacturing trend, high returns can be reasonably expected. However, as-reported metrics make it seem that CCHT’s acquisitions have not been synergistic, with as-reported ROAs ranging only from 2% to 16% levels since 2006.

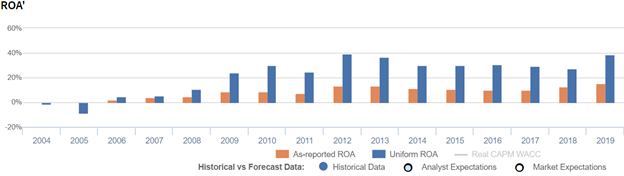

However, Uniform Accounting reveals that Uniform returns have been consistently more robust than what the market thinks. This is evident when Uniform ROA was actually at 39% in 2019, which is more than double the as-reported numbers.

One key metric that is causing distortions in as-reported ROAs is minority interest expense.

Minority interest expense is the portion of the company’s total earnings that is attributed to its minority shareholders. These minority shareholders are investors or other organizations that own less than 50% of the company.

CCHT regularly reports minority interest expenses, which are deducted from the company’s total earnings. This is done to account for the part of the earnings that is allocated to the company’s minority shareholders.

However, removing minority interest expenses from a company’s net income does not show its performance as a whole, making the company’s profitability appear substantially weaker than it actually is. By adding it back to the company’s net income, we can see the company’s true earning power as a whole and not just a part of it.

After adjusting for minority interest expense and applying other adjustments, we can see that CCHT’s ROA doesn’t just perform at 16% levels. In fact, its Uniform returns are more than 2x stronger than what the market thinks.

CCHT’s profitability is more robust than you think

As-reported metrics are distorting the market’s perception of the firm’s profitability. If you were to just look at as-reported ROA, you would think that the company is a weaker business than real economic metrics reveal.

CCHT’s Uniform ROA has been higher than its as-reported ROA in fourteen of the past sixteen years. For example, when Uniform ROA peaked at 40% in 2012, as-reported ROA was only 14%.

The company’s Uniform ROA for the past sixteen years has ranged from -8% to 40%, while as-reported ROA has ranged only from 0% to 16% in the same timeframe.

Specifically, Uniform ROA fell from -2% in 2004 to -8% in 2005, before rising to a peak of 40% in 2012. It then declined to 27% in 2018, before rebounding to 39% in 2019.

Changchun’s Uniform earnings margins are generally weaker than you think, but its Uniform asset turns make up for it

Volatility in Uniform ROA has been driven by trends in Uniform earnings margins, with peaks and troughs lining up historically with that of Uniform ROA.

From -3% in 2004, Uniform margins fell to -14% in 2005, before rising to 23%-28% levels from 2012-2018. It then peaked at 34% in 2019.

Meanwhile, Uniform turns have been consistently higher than as-reported metrics, ranging at 0.5x to 1.7x levels in the past sixteen years.

SUMMARY and Changchun High & New Technology Industry (Group) Inc. Tearsheet

As the Uniform Accounting tearsheet for Changchun High & New Technology Industry (Group) Inc. (000661:CHN) highlights, the Uniform P/E trades at 43.1x, which is above the global corporate average of 25.2x and its own historical average of 24.7x.

High P/Es require high EPS growth to sustain them. That said, in the case of CCHT, the company has recently shown an 83% Uniform EPS growth.

Sell-side analysts provide stock and valuation recommendations that in general provide very poor guidance or insight. However, sell-side analysts’ near-term earnings forecasts tend to have relevant information.

We take sell-side forecasts for Chinese Accounting Standards (CAS) earnings and convert them to Uniform earnings forecasts. When we do this, CCHT’s sell-side analyst-driven forecast is a 37% EPS decline in 2020 and a 25% EPS growth in 2021.

Based on the current stock market valuations, we can use earnings growth valuation metrics to back into the required growth rate to justify CCHT’s CNY 463 stock price. These are often referred to as market embedded expectations.

CCHT is currently being valued as if Uniform earnings were to grow 28% annually over the next three years. What sell-side analysts expect for CCHT’s earnings growth is below what the current stock market valuation requires in 2020 and 2021.

Furthermore, the company’s earning power is 6x above the long-run corporate average. Also, cash flows and cash on hand are significantly above its total obligations—including debt maturities, capex maintenance, and dividends. All in all, this signals a low credit and dividend risk.

To conclude, CCHT’s Uniform earnings growth is below its peer averages but the company is trading above its average peer valuations.

About the Philippine Markets Daily

“Wednesday Uniform Earnings Tearsheets – Asia-listed Focus”

Some of the world’s greatest investors learned from the Father of Value Investing or have learned to follow his investment philosophy very closely. That pioneer of value investing is Professor Benjamin Graham. His followers:

Warren Buffett and Charles Munger of Berkshire Hathaway; Shelby C. Davis of Davis Funds; Marty Whitman of Third Avenue Value Fund; Jean-Marie Eveillard of First Eagle; Mitch Julis of Canyon Capital; just to name a few.

Each of these great investors studied security analysis and valuation, applying this methodology to manage their multi-billion dollar portfolios. They did this without relying on as-reported numbers.

Uniform Adjusted Financial Reporting Standards (UAFRS or Uniform Accounting) is an answer to the many inconsistencies present in GAAP and IFRS, as well as in PFRS.

Under UAFRS, each company’s financial statements are rebuilt under a consistent set of rules, resulting in an apples-to-apples comparison. Resulting UAFRS-based earnings, assets, debts, cash flows from operations, investing, and financing, and other key elements become the basis for more reliable financial statement analysis.

Every Wednesday, we focus on one company listed in Asia that’s relevant to the Philippines and that’s particularly interesting from a UAFRS vs as-reported standpoint. We highlight one adjustment that illustrates why the as-reported numbers are unreliable.

This way, we gain a better understanding of the factors driving a particular stock’s returns, and whether or not the firm’s true profitability is reflected in its current valuations.

Hope you’ve found this week’s Uniform Earning Tearsheet on an Asian company interesting and insightful.

Stay tuned for next week’s Asia company highlight!

Regards,

Angelica Lim

Research Director

Philippine Markets Daily

Powered by Valens Research

www.valens-research.com