This coffee giant is brewing the perfect blend of good coffee, robust 28% Uniform earning power, and long-term growth.

Store closures across the Philippines and the US over the coronavirus are disrupting this coffee company’s operations. But their strong brand presence and customer loyalty will help them weather through these short-term disruptions.

From their friendly baristas to their seasonal drinks, this global coffee shop chain has become a cultural icon that managed to earn customer loyalty by focusing on personalization and simply knowing and giving what the customer wants.

Though as-reported metrics may signal that these strategies are not working, evidenced by declines in profitability, TRUE UAFRS-based (Uniform) analysis shows that this company has actually gone up to new highs and is expected to continue the trend in the future.

Also below, Uniform Accounting Embedded Expectations Analysis and the Uniform Accounting Performance and Valuation Tearsheet for the company.

Philippine Markets Daily:

Thursday Uniform Earnings Tearsheets – Global Focus

Powered by Valens Research

Why would anyone pay PHP 170 for a cup of coffee?

In 1971, Zev Siegel, Jerry Baldwin, and Gordon Bowker decided to open a coffee bean shop in Seattle.

After much brainstorming over what to call their store, they finally settled on Starbucks.

Starbucks’ initial focus was only to sell high-quality beans to customers who got used to drinking commercialized coffee.

When Howard Schultz joined the company a decade later as the Director of Retail Operations and Marketing, major shifts began to brew—literally!

In 1983, Schultz went to Italy to represent Starbucks at an international trade show. During his time there, he realized just how different the coffee culture was in America, compared to Europe’s.

Following his trip, he suggested the coffeehouse concept to the founders, which the latter agreed to as a test. Starbucks now had espresso bars and offered actual drinkable coffee.

The success of that initiative made Schultz realize the profit potential of a proper coffee shop. However, when the original owners decided not to continue the coffeehouse concept, he resigned from the company to start his own coffee business, Il Giornale.

When Starbucks began running into financial troubles due in part to its rapid expansion and the debt they took on when they acquired Peet’s, the founders decided to sell the company.

In 1987, Schultz and a few other local investors were able to raise the money and buy Starbucks for $3.8 million through Il Giornale. Keeping the name, Il Giornale was now Starbucks Corporation.

Still, even after all that, the coffee he’s selling is just coffee. But he’s not really selling coffee—he’s selling an experience.

Drinking coffee shouldn’t just be sipping on ground up beans mixed with hot water, some sugar, and cream. It should be an experience in a place for conversation that offers a sense of comfort and community.

Schultz knew that the social aspect of drinking coffee was the link he needed to spur growth. So he took what he learned and he applied it to every Starbucks store he owned.

Now, every Starbucks barista knows how to make small talk with customers and the stores always smell like brewed coffee.

The smell of coffee, in particular, is such an important aspect of the Starbucks experience that employees—or partners, as what they’re called—aren’t allowed to wear perfume. They also serve no food that could overpower the aroma.

This attention to detail is how the company was able to attract and retain customers—people are willingly buying PHP 170 cups of coffee because of the overall customer experience.

Starbucks understands that people want the customized, made-just-for-you experience.

You could just order your latte at the counter and the barista would hand it to you minutes later, but that wouldn’t spark the connection the company wants to make.

Instead, they ask for your name and your order then call it out after they’ve finished preparing your drink. You know that they do it for everyone, but hearing your name makes you feel like they know you—like you’re part of a community.

Store designs also have that personalized touch. The company sets up interiors that reflect the neighbourhood surrounding the store so it would give off that local, cozy, cafe-round-the-corner feel.

The premium associated with the brand is also part of the reason why customers keep coming back. This becomes even more obvious around the holiday season with the Starbucks planner promotions.

It’s hard enough justifying PHP 170 for a cup of coffee, but spending that much for 18 cups just to get a planner is an even crazier notion—and people still do it.

It’s because the planner is seen as something that’s of limited supply. Not everyone will have it, and not everyone can get it, which is why people want it. The planner is sort of a prize for your loyalty.

Starbucks has masterfully executed the art of customer retention which is why their Uniform return on assets (ROA) is as robust as it is.

While short-term, COVID-19-related disruptions in the form of store closures are affecting the company’s operations across the Philippines and the US, their strong brand presence and sticky customer loyalty will help maintain strong ROAs in the long term.

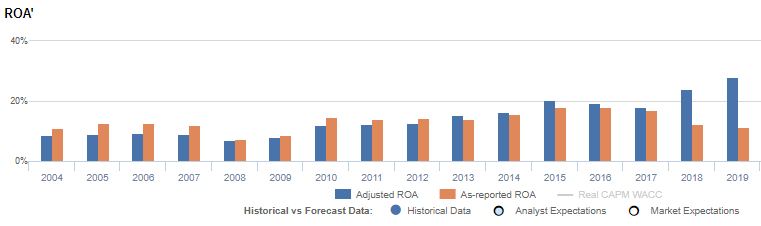

Furthermore, Uniform ROAs have been above cost-of-capital since 2004, excluding the recession years, and have climbed to a peak of 28% in 2019.

For the last seven years, Uniform metrics show profitability that is a lot stronger than what as-reported data state, with Uniform ROA being 2x more robust than as-reported ROA in the recent years.

What as-reported metrics fail to do is to consider excess cash on the balance sheet. While most companies inherently need some level of cash to operate, the portion of that balance that is earning limited or no return—or excess cash—ends up diluting as-reported ROAs.

As in the case of Starbucks, a substantial amount of cash received in 2018 from Nestle for the right to sell Starbucks’ products, materially overstates the company’s cash balances. As a result, as-reported ROA was at 12% in 2018, half of TRUE Uniform ROA of 24%.

With robust Uniform ROAs, although the company isn’t cheap at a 35.1x Uniform P/E, strong forecast earnings growth justify these valuations.

These forecasts can be actualized, despite the disruptions, as long as the company can carry out its growth initiatives—new roasteries, drive-thrus, and expansion plans for their food and beverage menus.

Starbucks’ earning power is still actually more robust than you think

As-reported metrics are understating Starbucks Corporation’s (SBUX:USA) profitability.

For example, as-reported ROA for Starbucks was 11% in 2019, which is materially lower than its Uniform ROA of 28%. Uniform ROA has been higher than as-reported ROA in seven of the past sixteen years.

As-reported metrics distort the market’s perception of the firm’s historical profitability trends. If you were to just look at as-reported ROA, you would think that the company is a much weaker business than real economic metrics highlight.

Starbucks’ Uniform ROA ranged from 7% to 28% over the past sixteen years. From a historical low of 7% in 2008, Uniform ROA expanded to 12% in 2010. It remained in the 12% to 16% levels in 2010 to 2014, and then jumped to 20% in 2015. Uniform earning power grew to 24% in 2018, and further increased to 28% in 2019.

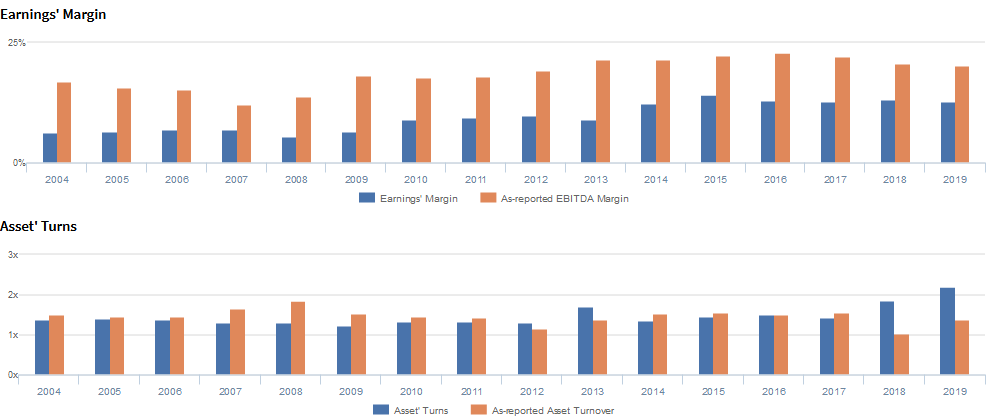

Starbucks’ Uniform ROA is driven by robust Uniform asset turns

Trends in Starbucks’ Uniform ROA have largely been driven by its stability in Uniform earnings margin and trends in Uniform asset turns.

From 2009-2015, Uniform earnings margins improved markedly from 6% to 14%, before stabilizing to 13% levels in 2019.

Meanwhile, after falling from 1.7x in 2013 to 1.3x in 2014, Uniform asset turns improved to 2.2x levels in 2019.

At current valuations, markets are pricing in expectations for both Uniform earnings margins and Uniform asset turns to climb to new peaks.

SUMMARY and Starbucks Tearsheet

As the Uniform Accounting tearsheet for Starbucks highlights, the Uniform P/E trades at 29.9x, which is above corporate average valuation levels but around its own recent history.

High P/Es require high EPS growth to sustain them. In the case of Starbucks, the company has recently shown a 12% Uniform EPS growth.

Wall Street analysts provide stock and valuation recommendations that in general provide very poor guidance or insight. However, Wall Street analysts’ near-term earnings forecasts tend to have relevant information.

We take Wall Street forecasts for GAAP earnings and convert them to Uniform earnings forecasts. When we do this, Starbucks’ Wall Street analyst-driven forecast is a 5% shrinkage in 2020, and a 20% growth in 2021.

Based on current stock market valuations, we can use earnings growth valuation metrics to back into the required growth rate to justify Starbucks’ $66 stock price. These are often referred to as market embedded expectations.

In order to justify current stock prices, the company would need to have Uniform earnings grow by 5% each year over the next three years. What Wall Street analysts expect for Starbucks’ earnings growth is above what the current stock market valuation requires.

The company’s earning power is 5x the corporate averages. Also, cash flows are about 2x their total obligations—including debt maturities, capex maintenance, and dividends. Together, this signals low credit risk and dividend risk.

To conclude, Starbucks’ Uniform earnings growth is below peer averages in 2020. Also, the company is trading above average peer valuations.

About the Philippine Market Daily

“Thursday Uniform Earnings Tearsheets – Global Focus”

Some of the world’s greatest investors learned from the Father of Value Investing or have learned to follow his investment philosophy very closely. That pioneer of value investing is Professor Benjamin Graham. His followers:

Warren Buffett and Charles Munger of Berkshire Hathaway; Shelby C. Davis of Davis Funds; Marty Whitman of Third Avenue Value Fund; Jean-Marie Eveillard of First Eagle; Mitch Julis of Canyon Capital; just to name a few.

Each of these great investors studied security analysis and valuation, applying this methodology to manage their multi-billion dollar portfolios. They did this without relying on as-reported numbers.

Uniform Adjusted Financial Reporting Standards (UAFRS or Uniform Accounting) is an answer to the many inconsistencies present in GAAP and IFRS, as well as in PFRS.

Under UAFRS, each company’s financial statements are rebuilt under a consistent set of rules, resulting in an apples-to-apples comparison. Resulting UAFRS-based earnings, assets, debts, cash flows from operations, investing, and financing, and other key elements become the basis for more reliable financial statement analysis.

Every Thursday, we focus on one multinational company that’s particularly interesting from a UAFRS vs as-reported standpoint. We highlight one adjustment that illustrates why the as-reported numbers are unreliable.

This way, we gain a better understanding of the factors driving a particular stock’s returns, and whether or not the firm’s true profitability is reflected in its current valuations.

Hope you’ve found this week’s Uniform earnings tearsheet on a multinational company interesting and insightful.

Stay tuned for next week’s multinational company highlight!

Regards,

Angelica Lim & Joel Litman

Research Director & Chief Investment Strategist

Philippine Markets Daily

Powered by Valens Research

www.valens-research.com