This firm simplifies mutual fund investing with Seedbox, and Uniform Accounting shows its fund has double-digit growth potential

Innovation has become a game-changer especially in the fast-paced environment we are in. Brokerages, investment houses, and banks are finding new and creative ways to attract a wider audience and grab a larger market share.

One of the Philippines’ largest asset management firms launched an innovative investing platform a few years back, making mutual fund investing simple and easy.

One of this investment innovator’s equity mutual funds is now up 211% since 2004.

As expected, under as-reported financial metrics, the investments in this fund’s portfolio looks average with limited growth. However, UAFRS-based financial metrics are saying otherwise.

We also dig through one of the fund’s largest holdings, providing you with the current Uniform Accounting Performance and Valuation Tearsheet for that company.

Philippine Markets Daily:

Friday Uniform Portfolio Analytics

Powered by Valens Research

The rapid advancement in technology has driven companies to level up their games for good reason.

Firms who managed to ride this wave were able to keep themselves afloat. Unfortunately, those who failed to do so lost momentum and were unable to catch up. Even the previous market leaders who failed to adapt to the ever changing marketplace found themselves lurking in the shadow of their former glory.

The thing that helped firms successfully navigate through the precarious technological advancements is innovation. Innovation encompasses each and every industry, even the field of asset management—which has been transforming into a more competitive landscape over the past few years.

ATR Asset Management (ATRAM) dreamt of revolutionizing mutual fund investing in the advent of web platforms and mobile applications.

They aimed to provide Filipinos easy access and a simple approach to investing. The firm resolved to help investors improve their investment habits and leverage the advantages of equity investing.

In January 2016, ATRAM and Indivara Group, an Indonesian-based IT company, formed Seedbox Technologies, Inc. to develop an online investment platform. A few months later, Seedbox Philippines went live.

Seedbox, which can be accessed through both computers and smartphones, promises a user-friendly end-to-end digital investment experience. Through this platform, investing in ATRAM mutual funds can now be done in a few clicks.

Also, Seedbox enables users to plan their life goals, determines which mutual fund would best suit their personal aspirations and risk appetite, and visualizes how their investments would grow in a specified timeframe.

There are currently nine ATRAM funds in the platform, including one of the firm’s largest mutual funds—the ATRAM Philippine Equity Opportunity Fund.

ATRAM Philippine Equity Opportunity Fund buys fundamentally attractive stocks and holds them in a span of three to five years.

Recently, they made efforts to track the performance of the Philippine Stock Exchange Index (PSEi), capping the performance deviation at 5%.

Fund manager Phillip Frederick S. Hagedorn and his team performs deep in-house fundamental research around performance, valuation, and growth prospects. They also place a premium to companies with a high-quality management team and solid environmental, social, and corporate governance (ESG).

We’ve conducted a portfolio audit of ATRAM Philippine Equity Opportunity Fund’s holdings, focusing on their major non-financial holdings.

The table shows the top non-financial holdings of ATRAM Philippine Equity Opportunity Fund, as well as their Uniform ROA (ROA′), as-reported ROA, and ROA distortion.

Looking solely at the as-reported ROAs, which are found in various financial databases, you may wonder why most of these companies were picked in the first place, having as-reported ROAs below global average returns of 6%.

Unfortunately, as-reported financial statements and the metrics derived from there, such as ROA, are distorted. The existing financial reporting standards are marred with inconsistencies and miscategorizations that blur the underlying performance and valuation of companies.

Uniform Accounting, on the other hand, addresses these flaws and helps investors see and understand the true earning power and relative worth of firms across industries, geographies, and even time.

While as-reported numbers present average returns for this fund, which has generated 211% return since ATRAM took over the management of the fund in November 2004, Uniform ROA paints a much clearer picture.

Based on Uniform Accounting, the fund’s average ROA′ is around 10%, which is contrary to what as-reported numbers suggest. These companies are actually profitable with real earnings greater than cost-of-capital levels.

As such, it should not be surprising that when analyzing the non-financial holdings of ATRAM Philippine Equity Opportunity Fund, the figure that stands out is the huge discrepancy between ROA′ and as-reported ROA.

The distortion in percentage ranges from 21% to 155% and is attributable to the gross understatement of companies’ profitability. Ayala Corporation (AC:PHL), International Container Terminal Services, Inc. (ICT:PHL), and Eagle Cement Corporation (EAGLE:PHL) all have distortions greater than a hundred percent.

As-reported numbers incorrectly indicate that AC is a subpar company with an ROA of 4%. However, when accounting distortions are removed, AC is actually profitabile with 10% Uniform ROA. Similarly, ICT is not an average firm with 6% ROA, but in fact, a high quality firm with 14% Uniform ROA. As-reported accounting also understates the earning power of EAGLE with 8% ROA, when in reality, it’s a high performing firm having a Uniform ROA consistently above 16% for the past five years.

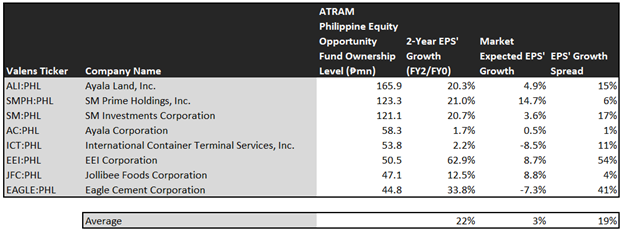

Furthermore, as-reported accounting also distorts a company’s earnings growth as shown above. This table has three interesting data points:

- The 2-year Uniform EPS growth represents the Uniform earnings growth the company is likely to have for the next two years. The earnings number used is the value of when we convert consensus sell-side analyst estimates to the Uniform Accounting framework.

- The market expected Uniform EPS growth represents what the market thinks Uniform earnings growth is going to be for the next two years. Here, we show by how much the company needs to grow Uniform earnings in the next two years to justify the current stock price of the company. This is the market’s embedded expectations for Uniform earnings growth.

- The Uniform EPS growth spread is the difference between the 2-year Uniform EPS growth and market-expected Uniform EPS growth.

On average, Philippine companies are expected to have 6% annual Uniform earnings growth over the next few years. Meanwhile, ATRAM’s major holdings are forecast to surpass that with 22% projected Uniform earnings growth in the next two years. Meanwhile, the market is seeing these companies expand by 3% a year, understating their growth by an average of 19%.

These are the kinds of companies that have growth potential, which would remain hidden underneath faulty as-reported financials.

Without Uniform Accounting, the as-reported numbers would leave everyone in the dark.

EEI Corporation (EEI:PHL) is one of the companies that have an understated earnings growth. The market is pricing the earnings of this construction firm to expand by 9% over the next two years. Contrary to that, the analysts are seeing a 63% Uniform earnings growth.

Another company with understated earnings growth is Eagle Cement Corporation. The market is pricing the cement producer’s earnings to shrink by 7% in the next two years. The analysts forecast otherwise, seeing a massive 34% Uniform earnings growth on the back of increasing sales volume, rising average selling price, aggressive expansion efforts, and steadying domestic demand.

Overall, with an average as-reported ROA of 5% and market-expected earnings growth of 3% annually, one might think that this portfolio has average returns with subpar earnings growth potential, which does not match ATRAM’s growth strategy.

However, looking through the lens of Uniform Accounting, for the most part, the ATRAM Philippine Equity Opportunity Fund comprises firms with robust returns and undervalued earnings growth potential—exactly the type of companies ATRAM looks for.

Eagle Cement Tearsheet

Today, we’re highlighting one of the largest individual stock holding in the ATRAM Philippine Equity Opportunity Fund—Eagle Cement Corporation.

As the Uniform Accounting tearsheet for Eagle Cement (EAGLE:PHL) highlights, Uniform P/E trades at 6.8x, well below market average valuations and slightly below its historical averages.

Low P/Es require low, and even negative, EPS growth to sustain them. In the case of Eagle Cement, their Uniform EPS declined by 1% over the past year.

Sell-side analysts provide stock and valuation recommendations that in general provide very poor guidance or insight. However, sell-side analysts’ near-term earnings forecasts tend to have relevant information.

We take sell-side forecasts for Philippine Financial Reporting Standards (PFRS) earnings and convert them to Uniform earnings forecasts. When we do this, Eagle Cement’s sell-side analyst-driven forecast shows an earnings growth of 48% in 2019 and 21% in 2020.

Based on the current stock market valuations, we can back into the required earnings growth rate that would justify PHP 10.30 per share. These are often referred to as market embedded expectations. Even if Eagle Cement’s Uniform earnings decline by 11% over the next three years, they will meet their current market valuation levels.

What sell-side analysts expect for Eagle Cement’s earnings growth is well above what the current stock market valuation requires.

To conclude, Eagle Cement’s Uniform earnings growth is well above peer averages in 2020. Moreover, the company is trading well below average valuations of their peers.

The company has an earning power that at least doubles the corporate average returns based on its Uniform ROA calculation. Together, this signals a low cash flow risk to the current dividend level in the future.

About the Philippine Markets Daily

“Friday Uniform Portfolio Analytics”

Investors who don’t engage in the buying or selling of securities for a living oftentimes rely on professionals to manage their own investments within the scope of their investment policies.

These portfolio managers either take on an active role in trading securities or take on a more passive role by putting additional investments in funds.

With so many funds and managers out there, it can get confusing and difficult to decide which one best suits your needs as an investor.

Sometimes, it might look like the manager is buying stocks that don’t seem like high-quality firms. Other times, it might look like the manager is taking a very long-term position on a stock that has not moved for a long time.

Every Friday, we focus on one fund in the Philippines and take a deeper look into their current holdings. Using Uniform Accounting, we identify the high-quality stocks in their portfolio which may not be obvious using the as-reported numbers.

We also identify which holdings may be problematic for the fund’s returns that they would need to reconsider from a UAFRS perspective.

To wrap up the fund analysis, we highlight one of their largest holdings and focus on key metrics to watch out for, accessible in our tearsheets.

Hope you’ve found this week’s focus on the ATRAM Philippine Equity Opportunity Fund interesting and insightful.

Stay tuned for next week’s Friday Uniform Portfolio Analytics!

Regards,

Angelica Lim & Joel Litman

Research Director & Chief Investment Strategist

Philippine Markets Daily

Powered by Valens Research

www.valens-research.com