This IT company has made revolutionary contributions to the Chinese government, with a Uniform ROA that’s almost 6x what is reported!

This Chinese corporation is known to have developed Intelligent Tax, a software that helps adhere to the Golden Tax System in China utilized by their State Taxation Administration. This system makes it almost impossible to cheat the taxation process.

The company has also enhanced its business by entering into partnerships with corporations from different countries. However, as-reported metrics do not translate its success in these partnerships, making it look like a weaker business. Uniform Accounting shows that this business is actually far more robust than what we think it is.

Also below, Uniform Accounting Embedded Expectations Analysis and the Uniform Accounting Performance and Valuation Tearsheet for the company.

Philippine Markets Daily:

Wednesday Uniform Earnings Tearsheets – Asia-listed Focus

Powered by Valens Research

Nowadays, daily activities are often executed through one’s phone or computer. Anyone can order their food, hail a ride, transfer funds from one bank to another, or hold online classes through different platforms made available by distinct companies.

Even with all these improvements, there are still other new developments that have been launched or are in the works to not only better people’s way of living, but also upgrade businesses’ operating systems.

One trend is the deployment of the Internet of Things (IoT).

As an example, Amazon has launched “Amazon Go” which allows consumers to buy products without the need for checking out manually by using IoT and machine vision. We’ve also previously discussed companies in Asia that incorporate IoT to enhance their offerings: Haier, Midea, and Fibocom.

Developments are also pursued using artificial intelligence (AI), including Siri, Alexa, and Google Assistant, which are helpful for simple tasks such as playing a specific song or looking for a good restaurant near one’s location.

In China, scientists and different institutions are using AI to improve the country’s taxing system to prohibit businesses from cheating taxes.

Aisino Corporation developed the Intelligent Tax program in compliance with China’s Golden Tax System. The Golden Tax is a VAT monitoring system required to be used by all businesses in mainland China. The Intelligent Tax software can spot the existence of tax evasion, which is a problem in existing methods of detection due to the lack of manpower to check tax reports.

Moreover, the company incorporates IoT to address voting problems, such as election fraud and duplicate registration, with its national citizen voting fingerprint application solution.

Furthermore, Aisino has entered into strategic partnerships in the past five years to improve its services and expand its reach in the banking industry.

In November 2016, Aisino finalized its joint venture with Diebold Nixdorf, an American corporation that specializes in the banking and retail industry by providing softwares, hardwares, and security. This venture allowed Aisino to enter a bigger banking business and offer IT solutions, specifically to the banking and retail businesses in China.

The company also formed a strategic alliance with Coupa Software, an American Corporation specializing in Business Spending Management, in November 2017. This alliance provides assistance to global companies that have expanded in China through Coupa’s unified platform that incorporates the country’s Golden Tax System.

Moreover, the alliance allows multinational companies to manage their business expenses while adhering to China’s taxing requirements.

In 2018, Aisino then entered into a business partnership with IBM Hong Kong Corporation, enabling the former to incorporate IBM’s systems, softwares, and cloud offerings into its system, as well as be a reseller of these offerings.

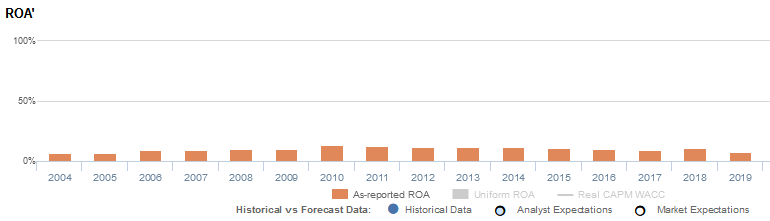

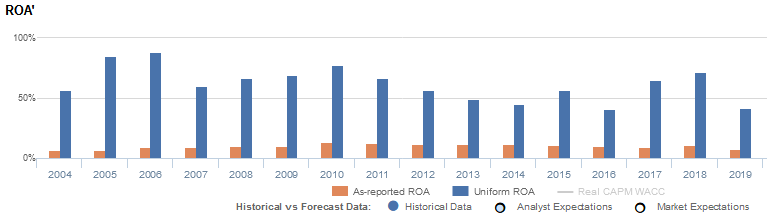

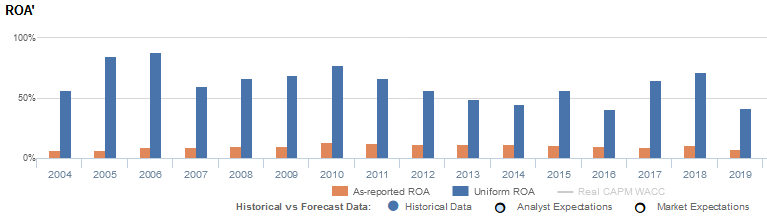

Even with its one-of-a-kind tax system and its big partnerships across the globe, as-reported metrics make it look like these initiatives haven’t been translating into profitable returns. For the past sixteen years, as-reported ROAs have been lackluster, ranging only from 7% to 13%.

This is not the real case for Aisino. Uniform Accounting shows that its alliances with different companies have resulted in significantly more robust returns than what as-reported metrics show.

In reality, Aisino has had a strong performance for the past sixteen years, with Uniform ROAs that have been 4x to 12x stronger than what the market thinks.

What as-reported metrics fail to do is to consider the company’s excess cash on the balance sheet. While most companies inherently need some level of cash to operate, the portion of that balance that is earning limited or no return—or excess cash—ends up diluting as-reported ROAs.

When excess cash remains included in the company’s asset base in computing its performance metrics, the company’s profitability and capital efficiency may appear weaker than it actually is. Removing excess cash allows investors to see through the distortions that come from management carrying much more cash on the balance sheet than what is operationally required.

From 2004 to 2019, Aisino has had a significant amount of excess cash sitting idly in its balance sheet, ranging from 41% to 61% of its as-reported total assets.

After excess cash and other significant adjustments are made, we can see that Aisino’s returns are actually a lot stronger than what as-reported metrics show. Without these adjustments, it appears that the company hasn’t been benefiting from its global partnerships, leading to poorer valuations.

Aisino Corporation’s Uniform valuation is cheaper than you think

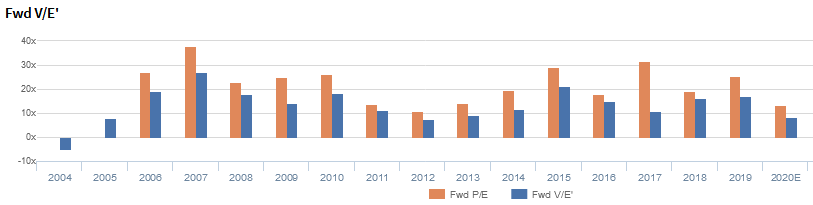

Aisino Corporation (600271:CHN) currently trades below corporate and historical averages with an 8.5x Uniform P/E (blue bars), which is also below its as-reported P/E of 13.2x (orange bars).

At these levels, the market is pricing in expectations for Uniform ROA to decrease from 41% in 2019 to 14% in 2024, accompanied by an 8% Uniform asset growth going forward.

However, analysts have less bearish expectations, projecting Uniform ROA to only decrease to 38% in 2021, accompanied by an 8% Uniform asset growth.

Aisino Corporation’s profitability is much better than you think

As-reported metrics are distorting the market’s perception of the firm’s profitability. If you were to just look at as-reported ROA, you would think that the company is a weaker business than real economic metrics highlight.

Aisino’s Uniform ROA has been higher than its as-reported ROA in the past sixteen years. For example, when Uniform ROA peaked at 88% in 2006, as-reported ROA was only 9%.

The company’s Uniform ROA for the past eight years has ranged from 41% to 88%, while as-reported ROA remained only between 7% and 13% in the same time frame.

From 56% in 2004, Uniform ROA reached a peak of 88% in 2006 before declining to 60% in 2007. Uniform ROA then increased to 77% in 2010 before gradually decreasing to 41% in 2016, excluding a 57% outperformance in 2015. Thereafter, Uniform ROA elevated to 72% in 2018 before compressing back to 41% in 2019.

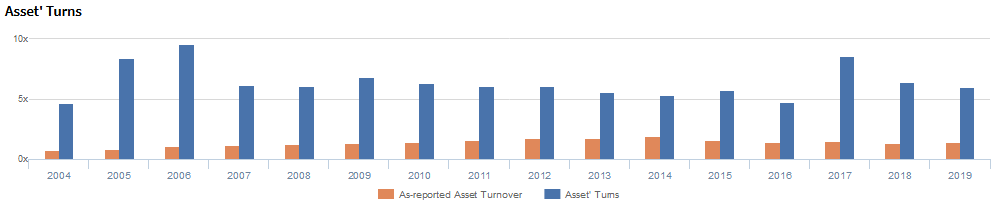

Aisino Corporation’s Uniform asset turns are more robust than you think

Volatility in Uniform ROA has been driven by trends in Uniform asset turns.

Uniform turns rose from 4.6x in 2004 to a peak of 9.6x in 2006. It then fell to 6.1x-6.3x levels in 2007-2012, excluding a 6.9x outperformance in 2009. Uniform turns then further declined to 4.8x in 2016, before jumping to 8.6x in 2017 and decreasing to 6.0x in 2019.

SUMMARY and Aisino Corporation Tearsheet

As the Uniform Accounting tearsheet for Aisino Corporation (600271:CHN) highlights, its Uniform P/E trades at 8.5x, which is below corporate average valuation levels and its own recent history.

Low P/Es require low EPS growth to sustain them. In the case of Aisino, the company has recently shown a 33% Uniform EPS shrinkage.

Sell-side analysts provide stock and valuation recommendations that in general provide very poor guidance or insight. However, sell-side analysts’ near-term earnings forecasts tend to have relevant information.

We take sell-side forecasts for Chinese Accounting Standards (CAS) earnings and convert them to Uniform earnings forecasts. When we do this, Aisino’s sell-side analyst-driven forecast is a 1% earnings shrinkage in 2020, followed by a 24% earnings growth in 2021.

Based on the current stock market valuations, we can use earnings growth valuation metrics to back into the required growth rate to justify Aisino’s CNY 12 stock price. These are often referred to as market embedded expectations.

Aisino can have a 13% Uniform earnings shrinkage for each of the next three years and still justify current market expectations. What sell-side analysts expect for Aisino’s earnings is above what the current stock market valuation requires in 2020 and 2021.

The company’s earning power is 7x the corporate average. Additionally, cash flows and cash on hand are 6x its total obligations. Together, this signals a low credit and dividend risk.

To conclude, Aisino’s Uniform earnings growth is below its peer averages in 2020, and the company is trading well below its peer valuations.

About the Philippine Market Daily

“Wednesday Uniform Earnings Tearsheets – Asia-listed Focus”

Some of the world’s greatest investors learned from the Father of Value Investing or have learned to follow his investment philosophy very closely. That pioneer of value investing is Professor Benjamin Graham. His followers:

Warren Buffett and Charles Munger of Berkshire Hathaway; Shelby C. Davis of Davis Funds; Marty Whitman of Third Avenue Value Fund; Jean-Marie Eveillard of First Eagle; Mitch Julis of Canyon Capital; just to name a few.

Each of these great investors studied security analysis and valuation, applying this methodology to manage their multi-billion dollar portfolios. They did this without relying on as-reported numbers.

Uniform Adjusted Financial Reporting Standards (UAFRS or Uniform Accounting) is an answer to the many inconsistencies present in GAAP and IFRS, as well as in PFRS.

Under UAFRS, each company’s financial statements are rebuilt under a consistent set of rules, resulting in an apples-to-apples comparison. Resulting UAFRS-based earnings, assets, debts, cash flows from operations, investing, and financing, and other key elements become the basis for more reliable financial statement analysis.

Every Wednesday, we focus on one company listed in Asia that’s relevant to the Philippines and that’s particularly interesting from a UAFRS vs as-reported standpoint. We highlight one adjustment that illustrates why the as-reported numbers are unreliable.

This way, we gain a better understanding of the factors driving a particular stock’s returns, and whether or not the firm’s true profitability is reflected in its current valuations.

Hope you’ve found this week’s Uniform Earning Tearsheet on an Asian company interesting and insightful.

Stay tuned for next week’s Asia company highlight!

Regards,

Angelica Lim

Research Director

Philippine Markets Daily

Powered by Valens Research

www.valens-research.com