This Korean company is winning in esports and in its global partnerships, with stronger Uniform returns of 27%, not 10%!

This South Korean company is known for its popular game, Blade & Soul, and has gradually established its presence worldwide.

However, as-reported metrics don’t reflect just how much the company has benefited from expanding westward, showing returns just slightly above cost of capital. Uniform Accounting shows that this company’s Uniform return on assets (ROAs) are more robust than what the market thinks.

Also, below, Uniform Accounting Embedded Expectations Analysis and the Uniform Accounting Performance and Valuation Tearsheet for the company.

Philippine Markets Daily:

Wednesday Uniform Earnings Tearsheets – Asia-listed Focus

Powered by Valens Research

Over the years, one can see how games have shifted from typical board games or arcade games to digital, like consoles, PCs, and even mobile phones.

This change has positively impacted the gaming industry, with online gaming becoming one of the fastest growing industries garnering a global revenue of USD 152 billion in 2019. The industry surpassed other traditional forms of entertainment such as movies and recorded music, which earned USD 43 billion and USD 20.2 billion in 2019, respectively.

Online gaming’s success paved the way for the rise of esports, which has become a source of income for professional gamers around the world, as well as for streamers on YouTube and other streaming platforms like Twitch. In the United States, during this pandemic alone, YouTube Gaming saw a 15% audience increase while Twitch saw its audience grow by 10%.

Considered as one of the most lucrative and competitive businesses worldwide, companies in the gaming industry are expected to keep up with the industry’s growth by pushing the limits of technology and imagination.

After all, a gaming company’s future is only as good as the games it continues to release.

Since its inception in 1997, Ncsoft Corporation has created well-known massive multiplayer online role-playing games (MMORPG) in South Korea and Asia such as Lineage and Lineage II. Its biggest game, Blade & Soul, was an instant hit when it was introduced in South Korea in 2012.

In 2015, Blade & Soul attracted a lot of attention from the esports community during its beta tests in the west. Famous esports players and organizations were excited for a new MMORPG game, other than World of Warcraft, that they immediately started planning and forming a competitive scene for Blade & Soul.

This provided Ncsoft with a smooth transition towards further expansion overseas.

In 2016, the company established its esports presence in the west by officially launching Blade & Soul in the region. Its strategy took into consideration the different play styles of the two regions: North Americans leaned towards an aggressive approach while Koreans were more defensive in terms of play styles.

Since then, Ncsoft has continuously updated its games to incorporate the western gaming style. The company launched its next global game, Master X Master (MXM), in 2017, and instead of launching it first in its home region, the company introduced the game to the western market first.

The company believed this plan was fit for MXM as its modes of 5v5 competitions and Player-versus-Environment cooperation play were very much favored in the west. This strategy also allowed the company to gather initial feedback for the game from a different point of view.

Another notable strategy Ncsoft took was to put great value on the gamers’ bond with each other. After all, one of the most important aspects in the esports and online gaming world is the gamer community.

Ncsoft added a feature in MXM that allows gamers to interact with each other while in queue for the game itself. This can help keep players hooked to the game as they not only have the chance to have fun and enhance their skills as they play, but also establish a relationship with the gaming community.

Due to the rise of esports, the use of PC and video game consoles has elevated in the past decade. In 2018, Ncsoft partnered with Harmonix Music System Inc. to create a game suitable for these devices. Through this partnership, the company was able to branch out of the multiplayer gaming community and break into the digital entertainment industry.

The game publisher also strengthened its game content and presence in the digital media space through its numerous investments in webtoon and web novel platforms.

Ncsoft made an investment of KRW 25 billion in a web novel portal called Munpia, in addition to its earlier investments in Lezhin Comics, Jaedam Media, and RS Media, under which they incorporated their well-known games in the production of their own webtoon or web novels.

Through these partnerships and with the growing popularity of esports, Ncsoft has been able to expand its global reach, and one would expect that this has made the company’s profitability stronger.

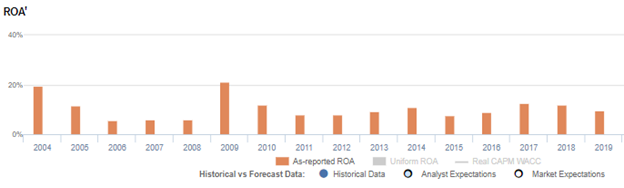

As-reported metrics show that the company’s returns have been just above cost-of-capital levels. However, for a company who has been benefitting from the growing popularity of esports all around the world and given the success of its partnerships, this as-reported ROA of 10% seems to be understated.

In reality, Ncsoft has profited a lot more thanks to its strategies, with Uniform ROAs that are more robust than what as-reported metrics show. Uniform ROA is currently at 27% levels, which is almost 3x stronger than what the market thinks.

What as-reported metrics fail to do is to consider the company’s excess cash on the balance sheet. While most companies inherently need some level of cash to operate, the portion of that balance that is earning limited or no return—or excess cash—ends up diluting as-reported ROAs.

When excess cash remains included in the company’s asset base in computing its performance metrics, the company’s profitability and capital efficiency may appear weaker than it actually is. Removing excess cash allows investors to see through the distortions that come from management carrying much more cash on the balance sheet than what is operationally required.

From 2004 to 2019, Ncsoft has had a significant amount of excess cash sitting idly in its balance sheet, ranging from 12% to 65% of its as-reported total assets.

After excess cash and other significant adjustments are made, Ncsoft’s success in expanding its global presence through partnerships is justified by its Uniform ROA, which is far more robust than its as-reported returns.

Ncsoft Corporation’s profitability is much better than you think it is

As-reported metrics are distorting the market’s perception of the firm’s profitability.

If you were to just look at as-reported ROA, you would think that the company is a weaker business than real economic metrics highlight. Ncsoft Corporation’s Uniform ROA has been higher than its as-reported ROA in fifteen of the past sixteen years. For example, when Uniform ROA peaked at 91% in 2004, as-reported ROA was just 20%.

The company’s Uniform ROA for the past six years has ranged from 19% to 64%, while as-reported ROA remained only between 8% and 12% in the same time frame.

After falling from a peak of 91% in 2004 to 10% in 2008, Uniform ROA rose to 33% in 2009 before declining again to 9% in 2013. Then, Uniform ROA elevated to 64% in 2017, before compressing to 27% in 2019.

Ncsoft Corporation’s Uniform earnings margins are weaker than you think but its robust Uniform asset turns make up for it

Volatility in Uniform ROA has been driven by trends in Uniform asset turns, and to a lesser extent by Uniform earnings margins, with peaks and troughs lining up historically with that of Uniform ROA.

After falling from 34% in 2004 to 17% in 2008, Uniform margins rose to 33% in 2009 before compressing to 12% in 2013. Since then, Uniform margins have expanded to 26% in 2019.

Meanwhile, Uniform turns fell from a peak of 2.7x in 2004 to 0.6x-1.0x levels in 2006 through 2016. It then jumped to 2.0x in 2017, before fading back to 1.0x in 2019.

SUMMARY and Ncsoft Corporation Limited Tearsheet

As the Uniform Accounting tearsheet for Ncsoft Corporation (036570:KOR) highlights, its Uniform P/E trades at 13.6x, which is below corporate average valuation levels, but around its own recent history.

Low P/Es require low EPS growth to sustain them. In the case of Ncsoft, the company has recently shown a 9% Uniform EPS decline.

Sell-side analysts provide stock and valuation recommendations that in general provide very poor guidance or insight. However, sell-side analysts’ near-term earnings forecasts tend to have relevant information.

We take sell-side forecasts for Korean International Financial Reporting Standards (K-IFRS) earnings and convert them to Uniform earnings forecasts. When we do this, Ncsoft’s sell-side analyst-driven forecast is a 92% and 48% earnings growth in 2020 and 2021, respectively.

Based on the current stock market valuations, we can use earnings growth valuation metrics to back into the required growth rate to justify Ncsoft’s KRW 828,000 stock price. These are often referred to as market embedded expectations.

The company needs Uniform earnings to grow 9% each year over the next three years to justify current prices. What sell-side analysts expect for Ncsoft’s earnings is well above what the current stock market valuation requires in 2020 and 2021.

The company’s earning power is 4x the corporate average. Additionally, cash flows and cash on hand are more than 7x its total obligations—including debt maturities, capex maintenance, and dividends. Together, this signals a low credit and dividend risk.

To conclude, Ncsoft’s Uniform earnings growth is well above its peer averages in 2020, and the company is trading in line with its peer valuations.

About the Philippine Market Daily

“Wednesday Uniform Earnings Tearsheets – Asia-listed Focus”

Some of the world’s greatest investors learned from the Father of Value Investing or have learned to follow his investment philosophy very closely. That pioneer of value investing is Professor Benjamin Graham. His followers:

Warren Buffett and Charles Munger of Berkshire Hathaway; Shelby C. Davis of Davis Funds; Marty Whitman of Third Avenue Value Fund; Jean-Marie Eveillard of First Eagle; Mitch Julis of Canyon Capital; just to name a few.

Each of these great investors studied security analysis and valuation, applying this methodology to manage their multi-billion dollar portfolios. They did this without relying on as-reported numbers.

Uniform Adjusted Financial Reporting Standards (UAFRS or Uniform Accounting) is an answer to the many inconsistencies present in GAAP and IFRS, as well as in PFRS.

Under UAFRS, each company’s financial statements are rebuilt under a consistent set of rules, resulting in an apples-to-apples comparison. Resulting UAFRS-based earnings, assets, debts, cash flows from operations, investing, and financing, and other key elements become the basis for more reliable financial statement analysis.

Every Wednesday, we focus on one company listed in Asia that’s relevant to the Philippines and that’s particularly interesting from a UAFRS vs as-reported standpoint. We highlight one adjustment that illustrates why the as-reported numbers are unreliable.

This way, we gain a better understanding of the factors driving a particular stock’s returns, and whether or not the firm’s true profitability is reflected in its current valuations.

Hope you’ve found this week’s Uniform Earning Tearsheet on an Asian company interesting and insightful.

Stay tuned for next week’s Asia company highlight!

Regards,

Angelica Lim

Research Director

Philippine Markets Daily

Powered by Valens Research

www.valens-research.com