With a 4% Uniform margin, this casual dining restaurant chain might need more preparation to serve high quality returns

The House That Fried Chicken Built.

Every Filipino knows where this slogan comes from. As the owner of one of the oldest restaurants in the Philippines, this company leads the casual dining market today through the expansion of its leading brand and the acquisition of other well-known brands.

Despite the company’s growth, Uniform Accounting shows that its true margins continue to range near historical lows, far lower than what as-reported metrics portray.

Also below, Uniform Accounting Embedded Expectations Analysis and the Uniform Accounting Performance and Valuation Tearsheet for the company.

Philippine Markets Daily:

Tuesday Uniform Earnings Tearsheets – Philippine-listed Focus

Powered by Valens Research

The beginnings of Max’s Group Inc. (PSE:MAXS) can be traced back to the establishment of Max’s of Manila in 1945, a company known today for being “the house that fried chicken built”.

It started with a man named Maximo Gimenez, who had managed to befriend American troops stationed in his city. He would welcome them to his home, always offering them food and drinks.

Later on, his friends would begin insisting that they pay for the hospitality. Maximo, realizing the opportunity here, decided to open a café to cater the troops.

Back then, the café only offered drinks, steak, and its signature chicken, but the chicken quickly became an instant favorite. People began dining at the cafe just for the chicken, inspiring Maximo to turn the place into a restaurant.

The huge success of Max’s Restaurant led the company to build more branches across the country and even open up to franchising in 1997. 9 years later, Max’s Group, Inc. was founded after obtaining the Philippine licenses to major foreign brands, Krispy Kreme and Jamba Juice.

The revenues from the new portfolio gave the company an opportunity to acquire Pancake House Inc. in 2014, which included the Pancake House, Teriyaki Boy, and Yellow Cab Pizza brands.

As a result of the 2014 acquisition, Max’s Group became the leader in the Philippine casual dining restaurant category with over 700 restaurants as of 2019. In fact, its continued expansion has helped the company generate almost consistent sales growth since 2005, peaking at 109% in 2015.

Unfortunately with the COVID-19 pandemic, the company’s sales growth record is likely to come to an end. Over the first half of 2020, the company has just been able to generate PHP 3.8 billion of revenue, 54% lower than the same period last year.

Furthermore, the company has been forced to miss its store openings target this year. As of June 30, 2020, the firm has 686 sites in the country and 59 stores abroad, still far from the company’s 1,000 total outlets goal by the end of 2020.

However, even with its robust sales growth and experience in the restaurant industry, Max’s Group has been unable to grow its margins. As-reported metrics claim the company’s EBITDA margins to be at 9% in 2019, but Uniform margins are actually lower at 4%.

Competing in a highly competitive market, the company has little power to raise prices without negatively impacting sales. In addition, it has been unable to limit its food and beverage costs, its biggest expense item.

Fundamentals aside, as-reported metrics are also allowing accounting distortions to impact the margin computation. One of the most significant distortions pertains to the treatment of special items.

Special Items are accounting events or transactions that are unusual in nature and infrequent in occurrence that can cause volatility in a company’s earnings. Examples of these types of items include one-time legal or restructuring charges, gains/losses from sale of assets, and asset write-downs.

Non-recurring income and expenses do not come about as a result of the company’s actual operations. Therefore, the after-tax effect of these are added back or subtracted to the firm’s earnings.

In ten of the past sixteen years, Max’s Group has been recognizing gains from the sale of assets. In 2019 specifically, the company gained PHP 327.6 million from the sale of assets.

Reversing the distortion along with the other changes Valens makes, Max’s Group’s 9% as-reported EBITDA margin and PHP 721.0 million net income are adjusted to reveal a TRUE Uniform earnings margin of 4% and Uniform earnings of only PHP 510.9 million.

Max’s Group’s earning power has eroded much worse than you think

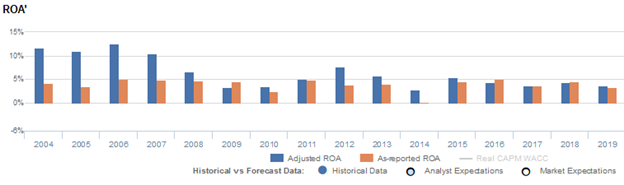

As-reported metrics distort the market’s perception of the firm’s historical profitability. If you were to just look at as-reported ROA, you would think that the company has had more stable profitability than real economic metrics highlight in the past sixteen years.

Max’s Group’s true profitability has been understated in twelve of the past sixteen years. Since 2004, as-reported ROA has only reached as high as 5%, while Uniform ROA has been able to peak at 13%.

Since 2004, as-reported ROA has maintained 3%-5% levels, excluding 2% and 0% underperformance in 2010 and 2014, respectively.

Meanwhile, after improving from 12% in 2004 to a peak of 13% in 2006, Uniform ROA declined to 4% in 2010, but recovered to 8% in 2012. Thereafter, Uniform ROA fell to its lowest at 3% in 2014, before rebounding to 4%-5% levels from 2015-2019.

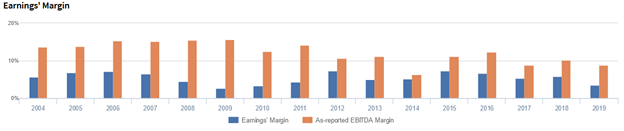

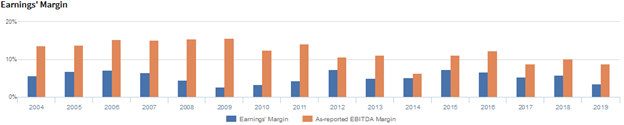

Max’s Group’s historical margins are weaker than you think

Weakness in Uniform ROA has been driven by weak Uniform earnings margins. Uniform margins have been lower than as-reported EBITDA margins in each of the past sixteen years.

As-reported EBITDA margins rose from 14% in 2004 to 16% in 2008-2009, before contracting to 6% in 2014. Thereafter, as-reported EBITDA margins expanded to 12% in 2016, before declining to 9% in 2019.

Meanwhile, Uniform margins improved from just 6% in 2004 to its peak of 7% in 2006, before regressing to its lowest at 3% in 2009. Though it gradually recovered back to 7% in 2012 and 2015-2016, Uniform margins have fallen to 4% in 2019.

Looking at the firm’s margins alone, the as-reported metrics are making the firm appear to be a more cost-efficient business than is accurate.

SUMMARY and Max’s Group, Inc. Tearsheet

As the Uniform Accounting tearsheet for Max’s Group (MAXS:PHL) highlights, the Uniform P/E trades at -59.2x, which is well below corporate average valuation and its own history.

Negative P/Es imply negative EPS growth. In the case of Max’s Group, the company has recently shown a 70% Uniform EPS decline.

Sell-side analysts provide stock and valuation recommendations that in general provide very poor guidance or insight. However, sell-side analysts’ near-term earnings forecasts tend to have relevant information.

We take sell-side forecasts for Philippine Financial Reporting Standards (PFRS) earnings and convert them to Uniform earnings forecasts. When we do this, Max’s Group’s sell-side analyst-driven forecast calls for a 674% and 99% Uniform EPS decline in 2020 and 2021, respectively.

Based on current stock market valuations, we can use earnings growth valuation metrics to back into the required growth rate to justify Max’s Group’s PHP 4.91 stock price. These are often referred to as market embedded expectations.

The company can have its EPS shrink by 2% each year over the next three years and still justify current valuations. What sell-side analysts expect for Max’s Group’s earnings growth is well below what the current stock market valuation requires in 2020 and 2021.

That said, the company’s earning power is below the long-run corporate average and intrinsic credit risk is 1,100bps above the risk-free rate. Together, this signals high credit and dividend risk.

To conclude, Max’s Group’s Uniform earnings growth is well below peer averages in 2020, and the company is trading below its peer average valuations.

About the Philippine Market Daily

“Tuesday Uniform Earnings Tearsheets – Philippine-listed Focus”

Some of the world’s greatest investors learned from the Father of Value Investing or have learned to follow his investment philosophy very closely. That pioneer of value investing is Professor Benjamin Graham. His followers:

Warren Buffett and Charles Munger of Berkshire Hathaway; Shelby C. Davis of Davis Funds; Marty Whitman of Third Avenue Value Fund; Jean-Marie Eveillard of First Eagle; Mitch Julis of Canyon Capital; just to name a few.

Each of these great investors studied security analysis and valuation, applying this methodology to manage their multi-billion dollar portfolios. They did this without relying on as-reported numbers.

Uniform Adjusted Financial Reporting Standards (UAFRS or Uniform Accounting) is an answer to the many inconsistencies present in GAAP and IFRS, as well as in PFRS.

Under IFRS, each company’s financial statements are rebuilt under a consistent set of rules, resulting in an apples-to-apples comparison. Resulting UAFRS-based earnings, assets, debts, cash flows from operations, investing, and financing, and other key elements become the basis for more reliable financial statement analysis.

Every Tuesday, we focus on one Philippine-listed company that’s particularly interesting from a UAFRS vs as-reported standpoint. We highlight one adjustment that illustrates why the as-reported numbers are unreliable.

This way, we gain a better understanding of the factors driving a particular stock’s returns, and whether or not the firm’s true profitability is reflected in its current valuations.

Hope you’ve found this week’s Uniform Earnings Tearsheet on a Philippine company interesting and insightful.

Stay tuned for next week’s Philippine company highlight!

Regards,

Angelica Lim

Research Director

Philippine Markets Daily

Powered by Valens Research

www.valens-research.com