With an 18% TRUE earning power, this food and beverage subsidiary has actually outperformed its parent by nearly thrice as much

Normally, investing in a conglomerate is the only way to gain a piece of a well-performing private subsidiary. However, it would also lead to an exposure to the underperforming ones.

This conglomerate had that in mind when it utilized a strategy that allowed its food and beverage business to be solely invested in. As a market leader in many categories, this subsidiary has been able to create robust returns which as-reported metrics seem to be understating.

Also below, Uniform Accounting Embedded Expectations Analysis and the Uniform Accounting Performance and Valuation Tearsheet for the company.

Philippine Markets Daily:

Tuesday Uniform Earnings Tearsheets – Philippine-listed Focus

Powered by Valens Research

One of our U.S.-focused Investor Essentials Dailies last week talked about the concept of the conglomerate discount. It is a situation wherein a conglomerate stock is trading at valuations less than the sum of each division’s valuations.

The diversification benefits provided by the conglomerate supposedly does not compensate for the additional costs of managing various unrelated businesses. In addition, management is assumed to be operating less efficiently since their focus is split amongst the businesses.

In the United States and in Europe, the number of conglomerates has gone down over the years. Such business groups have addressed the valuation problem by either fully divesting the unwanted business or spinning it off into its own independent company.

In developing countries, on the other hand, the conglomerate discount seems to be less prevalent. For example, in the Philippines, of the many local companies we’ve written about, a good number of them are either conglomerates or companies owned by conglomerates.

Regardless, the diversified business groups in the country have resorted to an alternative way of solving the same valuation problem—through the additional public listing of the subsidiary.

Also called an equity carve-out, this strategy legally separates the subsidiary from the parent company, requiring its own management and financials. This gives the subsidiary some degree of independence, while the parent company provides strategic direction and maintains a controlling interest.

For investors, equity carve-outs are useful when a business unit’s performance is dragged down by the underperformance of others. This is particularly evident with SMFB or San Miguel Food and Beverage, Inc. (FB:PHL).

As the largest food and beverage company in the country, SMFB owns many of the country’s beloved brands.

Their Purefoods Corned Beef and Tender Juicy Hotdog are one of the most common breakfast foods. Meanwhile, the company’s Red Horse Beer and San Miguel Pale Pilsen continue to be the two most popular alcoholic drinks in the Philippines.

Recently, the firm has been rapidly scaling the volumes of their beverage business, while quickly capitalizing on opportunities in their food business to reduce exposure from the African Swine Flu. These actions helped the firm generate a record-high return in 2019.

However, one might not fully appreciate SMFB’s strong performance when looking from the lens of its parent company, San Miguel Corporation (SMC:PHL).

Although SMC has been more efficient in their asset utilization than what as-reported metrics imply, it has only resulted in a 7% Uniform ROA—just a third of SMFB’s profitability. Such disparity can be attributed to SMC’s largest business, Petron Corporation (PCOR:PHL).

With Petron representing half of SMC’s total sales, Petron’s struggles to generate economic value has impacted the parent company’s bottom line. As a result, SMC investors would have to tolerate the weakness of its Fuel and Oil segment, which offsets any benefits these investors might get from the strong results of its Food and Beverage segment.

Fortunately, San Miguel Food and Beverage (FB:PHL) has been trading separately from its parent company in the Philippine Stock Exchange since 1973. This means investors can avoid exposing themselves to SMC’s other businesses. Today, SMFB’s market capitalization is larger than the conglomerate’s own market capitalization.

Looking at the as-reported metrics though, investing solely in SMFB may not look as beneficial as it seems, with only a 12% as-reported ROA. However, the as-reported metrics can be misleading due to the number of accounting distortions present in the company’s financials.

For SMFB, the largest accounting distortion has been the treatment of minority interest expenses. With the firm also having its own set of subsidiaries, each subsidiary has investors that possess non-controlling stakes.

According to the Philippine Financial Reporting Standards (PFRS), the profits attributable to minority shareholders can be recognized under operating cash flow, leading people to think that it is essential to the firm’s core operations.

In reality, it should always be classified as a financing cash flow. Minority shareholders have provided capital to the subsidiaries in exchange for a piece of the company’s earnings. As a result, minority interest expense should not be subtracted from SMFB’s revenues when calculating its real core earnings.

In 2019, SMFB recognized PHP 14.0 billion in minority interest expense, resulting in an PHP 18 billion net profit and a 12% as-reported ROA. By adding the expense back alongside the other adjustments Valens makes, the company should actually be recognizing PHP 32.3 billion in earnings and an 18% Uniform earning power.

San Miguel Food and Beverage’s earning power is stronger than you think

As-reported metrics distort the market’s perception of the firm’s recent profitability. If you were to just look at as-reported ROA, you would think that the company is a much weaker business than real economic metrics highlight.

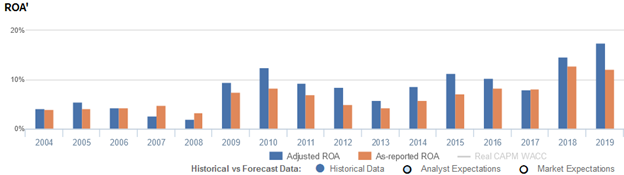

SMFB’s Uniform ROA has actually been significantly higher than its as-reported ROA since consolidating its food and beverage businesses in 2018. For example, as-reported ROA was 12% in 2019, but its Uniform ROA was stronger at 18%.

Through Uniform Accounting, we can see that the company’s true ROAs have actually been on a generally growing trend.

After fading from 6% in 2005 to a low of 2% in 2008, Uniform ROA soared to 13% in 2010 and fell back to 6% in 2013. Thereafter, Uniform ROA recovered to 11% in 2015, before declining to 8% in 2017 and subsequently rebounding to a peak of 18% in 2019.

San Miguel Food and Beverage is more efficient with its assets than you think

Overall strength in Uniform ROA has been driven by strength in Uniform asset turns. Since 2005, as-reported metrics have understated SMFB’s asset utilization, a key driver of profitability.

Uniform turns improved from 1.6x in 2004 to a high of 2.6x in 2010, before contracting to 1.7x in 2013. Then, Uniform turns improved to 2.4x in 2015, before receding to 1.3x in 2019.

Meanwhile, from 2004-2009, as-reported asset turnover sustained 1.8x-1.9x levels, before compressing to 1.4x levels in 2012-2013. Subsequently, Uniform turns recovered back to 1.8x in 2015, before declining again to 0.9x in 2019.

As-reported metrics have been making SFMB appear to be a far less asset efficient business than real economic metrics highlight.

SUMMARY and San Miguel Food and Beverage, Inc. Tearsheet

As the Uniform Accounting tearsheet for SFMB highlights, the Uniform P/E trades at 15.1x, which is below corporate average valuation levels but around its own history.

Low P/Es require low EPS growth to sustain them. In the case of SFMB, the company has recently shown a 137% Uniform EPS growth.

Sell-side analysts provide stock and valuation recommendations that in general provide very poor guidance or insight. However, sell-side analysts’ near-term earnings forecasts tend to have relevant information.

We take sell-side forecasts for PFRS earnings and convert them to Uniform earnings forecasts. When we do this, SFMB’s sell-side analyst-driven forecast calls for a 26% Uniform EPS decline in 2020 followed by a Uniform EPS growth of 20% in 2021.

Based on current stock market valuations, we can use earnings growth valuation metrics to back into the required growth rate to justify SFMB’s PHP 64.50 stock price. These are often referred to as market embedded expectations.

The company can have its Uniform earnings shrink by 4% each year over the next three years and still justify current valuations. What sell-side analysts expect for SFMB’s earnings growth is above what the current stock market valuation requires.

Furthermore, the company’s earning power is 3x the long-run corporate average. In addition, cash flows and cash on hand are above its total obligations—including debt maturities, capex maintenance, and dividends. Together, this signals low credit and dividend risk.

To conclude, SFMB’s Uniform earnings growth is well below peer averages, and the company is trading well below its peer average valuations.

About the Philippine Market Daily

“Tuesday Uniform Earnings Tearsheets – Philippine-listed Focus”

Some of the world’s greatest investors learned from the Father of Value Investing or have learned to follow his investment philosophy very closely. That pioneer of value investing is Professor Benjamin Graham. His followers:

Warren Buffett and Charles Munger of Berkshire Hathaway; Shelby C. Davis of Davis Funds; Marty Whitman of Third Avenue Value Fund; Jean-Marie Eveillard of First Eagle; Mitch Julis of Canyon Capital; just to name a few.

Each of these great investors studied security analysis and valuation, applying this methodology to manage their multi-billion dollar portfolios. They did this without relying on as-reported numbers.

Uniform Adjusted Financial Reporting Standards (UAFRS or Uniform Accounting) is an answer to the many inconsistencies present in GAAP and IFRS, as well as in PFRS.

Under IFRS, each company’s financial statements are rebuilt under a consistent set of rules, resulting in an apples-to-apples comparison. Resulting UAFRS-based earnings, assets, debts, cash flows from operations, investing, and financing, and other key elements become the basis for more reliable financial statement analysis.

Every Tuesday, we focus on one Philippine-listed company that’s particularly interesting from a UAFRS vs as-reported standpoint. We highlight one adjustment that illustrates why the as-reported numbers are unreliable.

This way, we gain a better understanding of the factors driving a particular stock’s returns, and whether or not the firm’s true profitability is reflected in its current valuations.

Hope you’ve found this week’s Uniform Earnings Tearsheet on a Philippine company interesting and insightful.

Stay tuned for next week’s Philippine company highlight!

Regards,

Angelica Lim

Research Director

Philippine Markets Daily

Powered by Valens Research

www.valens-research.com