As-reported ROA of 11% implies this caustic soda manufacturer has a clean-cut way to profitability, but 7% TRUE Uniform ROA tells otherwise

Being the only local producer of a product is the ideal scenario for many businesses, especially when the product is in high demand.

This manufacturer is the only Philippine producer of caustic sodas, a chemical every household and business uses in one form or another. However, Uniform Accounting shows the firm isn’t as successful as people think in capitalizing on its advantage.

Also below, Uniform Accounting Embedded Expectations Analysis and the Uniform Accounting Performance and Valuation Tearsheet for the company.

Philippine Markets Daily:

Tuesday Uniform Earnings Tearsheets – Philippine-listed Focus

Powered by Valens Research

Since ancient times, sodium hydroxide has been one of the most widely used chemicals. Although only scientifically identified in the 1800s, it has been commonly referred to as lye or caustic soda.

Its first discovered use was as a soap, and it still remains the main ingredient for that today. Back then, people noticed how easier it was to wash with lye and water. Substances that normally didn’t combine with water such as fats and oils suddenly became soluble when lye was applied.

As nations across the world industrialized, people found another use for lye. In its purer form, lye has been effective as a drain cleaner, detergent, and bleach

Furthermore, lye has been important in the production of paper, as it has made it easier to separate the wood pulp. It is also because of this chemical process that paper nowadays is more commonly white.

Strangely enough, lye has culinary uses as well, but only in small amounts. In the Philippines particularly, food-grade lye water is a key ingredient in making desserts like kutsinta and pichi-pichi.

Despite the widespread use of lye or caustic soda, only Mabuhay Vinyl Corporation (MVC:PHL) produces the chemical in the country. The company supplies the majority of the Philippines’ caustic soda and hydrochloric acid demand.

One might assume Mabuhay Vinyl has been seeing great success due to its near-monopoly position and considering the use of its product. Looking at the as-reported metrics, this assumption seems right.

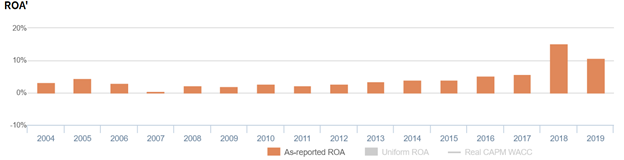

Mabuhay Vinyl has been profitable each year since 2004, with as-reported ROA rising in recent years as the company has expanded production.

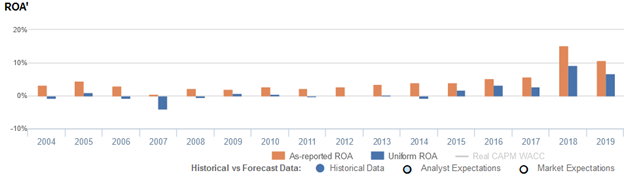

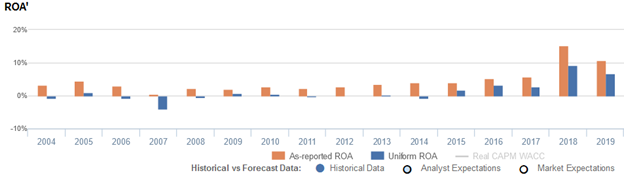

However, with Uniform Accounting, we see how the Philippine Financial Reporting Standards (PFRS) distorts the company’s real performance, overstating Mabuhay Vinyl’s true ROAs.

Observing Mabuhay Vinyl’s Uniform ROA, we see that the company’s true earning power has been lower than what as-reported metrics claim in each year since 2004. Moreover, the company had actually operated at a net loss in nearly half of those years.

While as-reported ROA was at 11% in 2019, Uniform ROA was only at 7% that year.

It seems Mabuhay Vinyl’s market power is weaker than we’re led to believe. While the company is the only local producer, it still has international competitors to contend with. Driving up the price too much will encourage customers to rely on imports instead.

The distortion in Mabuhay Vinyl’s ROA mainly comes from PFRS allowing the firm to extend the lives of its fixed assets, which allows the company’s old assets to still be in use.

Extending an asset’s life isn’t inherently an issue, but keeping its book value does. Without adjusting for inflation, a company looks more efficient than in reality when tying present-day cash flows to assets purchased years or decades ago.

In 2019, Mabuhay Vinyl’s total as-reported assets amounted to PHP 2.9 billion, but the company should be recognizing PHP 1.0 billion or a third more in assets when adjusting its PP&E for inflation.

Applying the inflation adjustment, along with many other necessary adjustments, leads to a 7% Uniform ROA in 2019, significantly lower than the as-reported ROA of 11%.

Mabuhay Vinyl’s historical earning power is weaker than you think

As-reported metrics distort the market’s perception of the firm’s historical profitability. If you were to just look at as-reported ROA, you would think Mabuhay Vinyl’s profitability has been stronger than real economic metrics have highlighted in the past sixteen years.

In reality, Mabuhay Vinyl’s true profitability has been lower than as-reported ROA since 2004. Specifically, as-reported ROA was 11% in 2019, but Uniform ROA was only 7% that year.

As-reported ROA improved from 3% in 2004 to 5% in 2005, before fading to a low of 1% in 2007 and subsequently expanding to a peak of 15% in 2018. Since then, as-reported ROA has fallen to 11% in 2019.

Meanwhile, after rising from -1% in 2004 to 1% in 2005, Uniform ROA dropped to -4% in 2007 and recovered to 1% in 2009. Uniform ROA then contracted to immaterial levels in 2010-2013, before rebounding to a high of 9% in 2018 and declining to 7% in 2019.

Mabuhay Vinyl’s margins are weaker than you think

Weakness in Uniform ROA has been driven primarily by trends in Uniform earnings margins. In fact, Uniform margins have been materially lower than as-reported margins in each of the past sixteen years.

As-reported margins faded from 14% in 2004 to 8% in 2007, before improving to 16% in 2010 and compressing to 12% levels in 2011-2012. Thereafter, as-reported margins recovered back to 16% in 2013, before shrinking to 13% in 2017 and jumping to a peak of 24% in 2019.

Meanwhile, Uniform margins were volatile from 2004-2014, positive in only four of eleven years while ranging from -7% to 2%. Since then, Uniform margins have slowly risen to 11%-12% highs in 2018-2019.

Looking at the firm’s margins alone, as-reported metrics are making the firm appear to be a more cost-efficient business than is accurate.

SUMMARY and Mabuhay Vinyl Corporation Tearsheet

As the Uniform Accounting tearsheet for Mabuhay Vinyl Corporation (MVC:PHL) highlights, the Uniform P/E trades at a 7.9x, which is well below corporate averages but above its own history.

Low P/Es require low EPS growth to sustain them. That said, in the case of Mabuhay Vinyl, the company has recently shown a 26% Uniform EPS decline.

Sell-side analysts provide stock and valuation recommendations that provide very poor guidance or insight in general. However, sell-side analysts’ near-term earnings forecasts tend to have relevant information.

We take sell-side forecasts for Philippine Financial Reporting Standards (PFRS) earnings and convert them to Uniform earnings forecasts. When we do this, Mabuhay Vinyl’s sell-side analyst-driven forecast calls for a 15% Uniform EPS growth in 2020 and an immaterial decline in 2021.

Based on current stock market valuations, we can use earnings growth valuation metrics to back into the required growth rate to justify Mabuhay Vinyl’s PHP 4.70 stock price. These are often referred to as market embedded expectations.

The company can have Uniform earnings shrink by 16% each year over the next three years and still justify current valuations. What sell-side analysts expect for Mabuhay Vinyl’s earnings growth is above what the current stock market valuation requires in 2020 and 2021.

Furthermore, the company’s earning power is above the long-run corporate average, and cash flows and cash on hand are well above its total obligations—including debt maturities, capex maintenance, and dividends. Together, this signals low credit and dividend risk.

To conclude, Mabuhay Vinyl’s Uniform earnings growth is above peer averages, but the company is trading below peer average valuations.

About the Philippine Market Daily

“Tuesday Uniform Earnings Tearsheets – Philippine-listed Focus”

Some of the world’s greatest investors learned from the Father of Value Investing or have learned to follow his investment philosophy very closely. That pioneer of value investing is Professor Benjamin Graham. His followers:

Warren Buffett and Charles Munger of Berkshire Hathaway; Shelby C. Davis of Davis Funds; Marty Whitman of Third Avenue Value Fund; Jean-Marie Eveillard of First Eagle; Mitch Julis of Canyon Capital; just to name a few.

Each of these great investors studied security analysis and valuation, applying this methodology to manage their multi-billion dollar portfolios. They did this without relying on as-reported numbers.

Uniform Adjusted Financial Reporting Standards (UAFRS or Uniform Accounting) is an answer to the many inconsistencies present in GAAP and IFRS, as well as in PFRS.

Under IFRS, each company’s financial statements are rebuilt under a consistent set of rules, resulting in an apples-to-apples comparison. Resulting UAFRS-based earnings, assets, debts, cash flows from operations, investing, and financing, and other key elements become the basis for more reliable financial statement analysis.

Every Tuesday, we focus on one Philippine-listed company that’s particularly interesting from a UAFRS vs as-reported standpoint. We highlight one adjustment that illustrates why the as-reported numbers are unreliable.

This way, we gain a better understanding of the factors driving a particular stock’s returns, and whether or not the firm’s true profitability is reflected in its current valuations.

Hope you’ve found this week’s Uniform Earnings Tearsheet on a Philippine company interesting and insightful.

Stay tuned for next week’s Philippine company highlight!

Regards,

Angelica Lim

Research Director

Philippine Markets Daily

Powered by Valens Research

www.valens-research.com