Continuing to beef up its expansion strategies, this bee-loved fast food chain reached a Uniform ROA of 5%, not 1%

This company isn’t just the top fast-food chain in the Philippines—it is also receiving recognition in the global arena. For example, its Chickenjoy was recently named the best fried chicken in the U.S. by Eater.com, a Vox Media website. However, its as-reported metrics make it appear as if there is nothing to be jolly about in terms of profitability.

Also below, Uniform Accounting Embedded Expectations Analysis and the Uniform Accounting Performance and Valuation Tearsheet for the company.

Philippine Markets Newsletter:

Wednesday Uniform Earnings Tearsheets – Philippine-listed Focus

Powered by Valens Research

An ice cream plant visit prompted Tony Tan Caktiong to open his own ice cream parlors in 1975. Eventually, he would add hot meals such as burgers and sandwiches to the menu due to customer demand.

The hot meals turned out to be a crowd favorite, resulting in ice cream taking a backseat as the shop’s main product. This would prove accretive in the long run as the business was able to expand with its fried chicken, also known as Chickenjoy, at the core.

Thus, Jollibee was born.

The name Jollibee comes from the words “Jolly” – synonymous with happiness, and “Bee” – the hard-working insects.

Over the years, Jollibee has been dominating the Philippine market as it continues to outperform other fast-food giants like McDonald’s and KFC. Meanwhile, it has acquired or established partnerships with other fast-food chains in the process such as Chowking, Greenwich, Red Ribbon, and Mang Inasal.

However, even the Filipino staple was not spared from the negative impact of the pandemic. Owing to quarantine restrictions, the company had to adapt in order to survive and grow. It had to find ways to deliver more of its products, alter its offerings as read-to-cook meals, and close non-performing stores.

Yet, these strategies were not enough to even breakeven in 2020.

Fortunately, with the successful rollout of vaccines and the eventual reopening of the global economy, demand across the world recovered. In the first half of 2022, Jollibee as a corporation saw over 350% earnings growth.

In addition, the fast-food chain is ramping up its growth efforts, not just in the Philippines, but also in North America. It aims to open 500 stores in the next five to seven years in the U.S. and Canada. As of now, there are 70 Jollibee stores in North America.

In the Philippines, the company recently entered into a franchise agreement to operate and further grow the Yoshinoya brand in the Philippines. This strategic partnership is expected to be accretive to the company’s earnings, especially with Filipinos’ increasing demand for affordable Japanese meals.

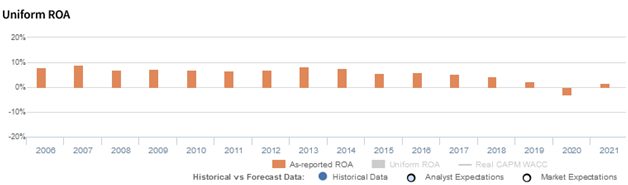

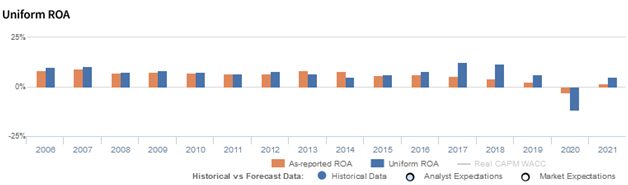

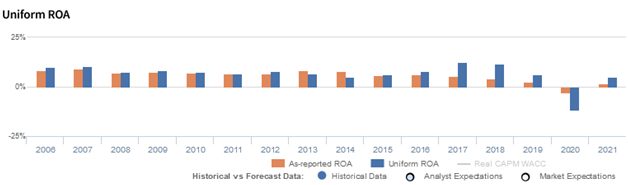

Looking at as-reported metrics, it appears that Jollibee has inflected positively in 2021, with return on assets (ROAs) recovering from a historical trough in the pandemic.

While this positive inflection is true, the company’s expansion strategy actually resulted in better numbers than presented, with Uniform ROAs performing slightly above cost of capital levels at 5%.

The distortion between Uniform and as-reported ROAs comes from as-reported metrics failing to consider the amount of goodwill on Jollibee’s balance sheet.

In recent years, goodwill sits at about PHP 62.9 billion, which is about 30% of the company’s total assets, arising from acquisitions made to expand its market reach.

Goodwill is an intangible asset that is purely accounting-based and unrepresentative of the company’s actual operating performance. When as-reported accounting includes this in a company’s balance sheet, it creates an artificially inflated asset base.

As a result, as-reported ROAs are not capturing the strength of Jollibee’s earning power. Adjusting for goodwill, we can see that the company isn’t producing paltry returns. In fact, it has been the opposite, with the company earning 2x greater returns.

Jollibee’s earning power is stronger than you think

As-reported metrics distort the market’s perception of the firm’s recent profitability. If you were to just look at as-reported ROA, you would think that Jollibee’s profitability was not that bad in 2020, and managed to simply turn positive in 2021.

Through Uniform Accounting, we can see that not only have the company’s true ROAs been inaccurate over the past decade, but its recent profitability inflection is more profound than investors may think. For example, as-reported ROA was 1% in 2021 from -3% in 2020, but its Uniform ROA was actually higher at 5%, coming from a much lower -12% in 2020.

Jollibee’s asset turns are more efficient than you think

Trends in Uniform ROA have been driven by trends in Uniform asset turns, as is expected from a fast-food chain. For more than two decades, as-reported metrics have understated Jollibee’s asset efficiency, a key driver of profitability.

Moreover, as-reported asset turnover has exceeded only up to 1.8x over the past decade. In comparison, Uniform turns have reached up to 3.2x over the same time period. This shows Jollibee really is a more efficient business than the as-reported metrics highlight.

SUMMARY and Jollibee Foods Corporation Tearsheet

As our Uniform Accounting tearsheet for Jollibee Foods Corporation (JFC:PHL) highlights, the company trades at a Uniform P/E of 39.8x, above the global corporate average of 19.3x, and around its historical P/E of 38.9x.

High P/Es require high EPS growth to sustain them. In the case of Jollibee, the company has recently shown an 89% Uniform EPS decline.

Sell-side analysts provide stock and valuation recommendations that in general provide very poor guidance or insight. However, sell-side analysts’ near-term earnings forecasts tend to have relevant information.

We take sell-side forecasts for Philippine Financial Reporting Standards (PFRS) earnings and convert them to Uniform earnings forecasts. When we do this, Jollibee’s sell-side analyst-driven forecast is to see a Uniform earnings decline of 371% in 2022 and a growth of 45% in 2023.

Based on current stock market valuations, we can use earnings growth valuation metrics to back into the required growth rate to justify Jollibee’s PHP 228.00 stock price. These are often referred to as market embedded expectations.

The company is currently being valued as if Uniform earnings were to grow 25% annually over the next three years. What sell-side analysts expect for Jollibee’s earnings growth is well below what the current stock market valuation requires in 2022, but above the requirement in 2023.

However, the company’s earning power is below the long-run corporate average. Moreover, cash flows and cash on hand are below total obligations—including debt maturities, capex maintenance, and dividends. Together, this signals high credit risk.

To conclude, Jollibee’s Uniform earnings growth is below its peer averages, but above its average peer valuations.

About the Philippine Markets Newsletter

“Wednesday Uniform Earnings Tearsheets – Philippine-listed Focus”

Some of the world’s greatest investors learned from the Father of Value Investing or have learned to follow his investment philosophy very closely. That pioneer of value investing is Professor Benjamin Graham. His followers:

Warren Buffett and Charles Munger of Berkshire Hathaway; Shelby C. Davis of Davis Funds; Marty Whitman of Third Avenue Value Fund; Jean-Marie Eveillard of First Eagle; Mitch Julis of Canyon Capital; just to name a few.

Each of these great investors studied security analysis and valuation, applying this methodology to manage their multi-billion dollar portfolios. They did this without relying on as-reported numbers.

Uniform Adjusted Financial Reporting Standards (UAFRS or Uniform Accounting) is an answer to the many inconsistencies present in GAAP and IFRS, as well as in PFRS.

Under IFRS, each company’s financial statements are rebuilt under a consistent set of rules, resulting in an apples-to-apples comparison. Resulting UAFRS-based earnings, assets, debts, cash flows from operations, investing, and financing, and other key elements become the basis for more reliable financial statement analysis.

Every Wednesday, we focus on one Philippine-listed company that’s particularly interesting from a UAFRS vs as-reported standpoint. We highlight one adjustment that illustrates why the as-reported numbers are unreliable.

This way, we gain a better understanding of the factors driving a particular stock’s returns, and whether or not the firm’s true profitability is reflected in its current valuations.

Hope you’ve found this week’s Uniform Earnings Tearsheet on a Philippine company interesting and insightful.

Stay tuned for next week’s Philippine company highlight!

Regards,

Angelica Lim

Research Director

Philippine Markets Newsletter

Powered by Valens Research

www.valens-research.com