Its soup may have gone cold, but this company has found other ways to reheat its business, leading to Uniform ROAs that have reached new highs

Success in the food industry is defined by how well the company can adapt to the ever-changing consumer taste.

So when demand for this company’s canned soup began to decline, it ventured into the “trendier” health food market, and even more successfully, into the fast-growing snacking market.

While as-reported metrics suggest that this move crushed company returns, Uniform Accounting reveals the opposite, with Uniform returns that have actually gone up to new highs.

Also below, Uniform Accounting Embedded Expectations Analysis and the Uniform Accounting Performance and Valuation Tearsheet for the company.

Philippine Markets Daily:

Thursday Uniform Earnings Tearsheets – Global Focus

Powered by Valens Research

Earlier civilizations have had to hunt for their food in order to survive, using wood and stones to fashion spears and kill large animals. Once the meat was carved off, humans would have had to cook and consume it immediately before it went bad—that is, until food preservation techniques were developed.

Many cultures have used methods such as drying meat and vegetables under the sun, and some civilizations living in colder climates used refrigeration by digging snow pits to store food in.

While we still use these methods today, albeit using machines rather than nature, technological advancements have increased the number of ways we can preserve food. The most notable and common of which is canning.

It’s fair to say that canned goods have become a household staple in any country. In the Philippines, for example, canned sardines, corned beef, and luncheon meat are some of the Filipino favorites.

Canned goods have become a necessity in the kitchen because of its convenience and long shelf-life. There is a broad range of food products that are canned today, including tomatoes, mushroom, chicken, fish—you name it.

In the United States, one of the top-selling canned foods is soup from the Campbell Soup Company (CPB:USA).

In 1897, Dr. John T. Dorrance, former Campbell president and chemist, invented the process of condensing soup to utilize cans as a smaller form of packaging. This built the foundation of what is now one of the largest processed food companies in the United States.

Over the last decade, however, Campbell’s processed food sales have been struggling as consumers, especially millennials, began gravitating towards more fresh, organic, and unprocessed foods.

In response, the company expanded its product portfolio by acquiring other food companies. Beyond soup, it now also offers healthy beverages, salad dressings, hummus and salsa, and biscuits following the acquisitions of Bolthouse Farms, Kelsen Group, and Garden Fresh Gourmet.

Still, its push into healthier markets failed to gain traction as the company continued to suffer from consistently declining sales.

Because of this, the company decided to focus on the faster-growing snacking market and acquired snacks company, Snyder-Lance in 2017. The acquisition strengthened the company’s snacking division, which previously only consisted of its Pepperidge Farm brands.

Apart from shifting its focus away from its core soup business, the company also divested most of its other processed food brands including Bolthouse Farms and Garden Fresh Gourmet in 2019. Both of these strategies aimed to generate cash flows and new revenue streams to help ease the debt load it had taken from its acquisition sprees.

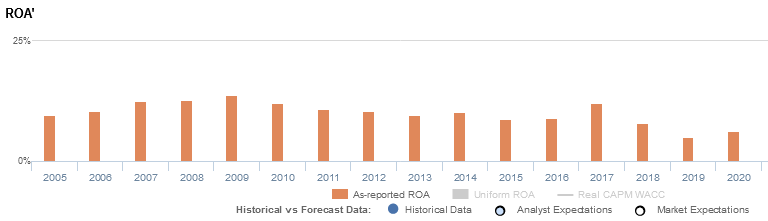

That being said, analysts who take a look at Campbell’s as-reported financials would think the company’s focus on snacking away from its core soup business wasn’t the right move, with return on assets (ROAs) falling from 14%-18% historically to just 5%-8% following the Snyder’s-Lance acquisition.

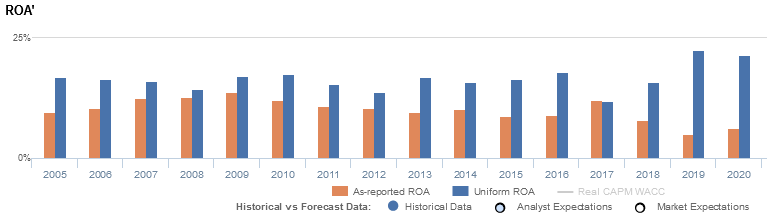

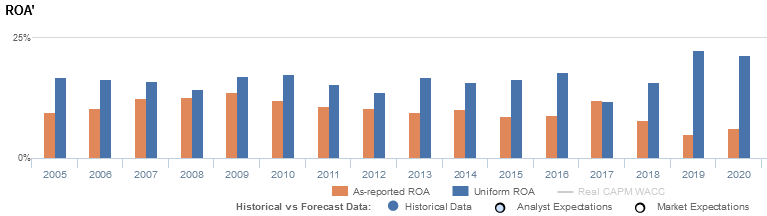

In reality, Campbell’s strategic decisions were the right choice, with Uniform ROAs that have actually improved to 20% levels post-acquisition and post-divestitures.

The distortion between Uniform and as-reported ROAs comes from as-reported metrics failing to consider the amount of goodwill on Campbell’s balance sheet. In recent years, goodwill sits at about $4 billion, or around a third of its total assets, stemming from the company’s string of acquisitions.

Goodwill is an intangible asset that is purely accounting-based and unrepresentative of the company’s actual operating performance. When as-reported accounting includes this in a company’s balance sheet, it creates an artificially inflated asset base.

As a result, as-reported ROAs are not capturing the strength of Campbell’s earning power. Adjusting for goodwill, we can see that the company isn’t actually performing poorly. In fact, it has been the complete opposite, with returns that are around 3x-4x higher than what is reported.

Campbell is actually more profitable than you think it is

As-reported metrics distort the market’s perception of the firm’s recent profitability. If you were to just look at as-reported ROA, you would think the company is a much weaker business than real economic metrics highlight.

Campbell’s Uniform ROA has actually been higher than its as-reported ROA in fifteen of the past sixteen years. For example, Uniform ROA was at 20% in 2020, while as-reported ROA was only at 6%.

Specifically, Campbell’s Uniform ROA has ranged from 12%-22% in the past sixteen years while as-reported ROA has ranged from only 5%-14% levels in the same timeframe.

Looking at the trend, Uniform ROA ranged from 14%-18% levels in 2005-2016, before briefly dropping to 12% in 2017. Thereafter, Uniform ROA rebounded to a peak of 22% in 2019, before slightly compressing to 20% in 2020.

Campbell’s Uniform earnings margin is weaker than you think, but its Uniform asset turns make up for it

Trends in Uniform ROA have been primarily driven by trends in Uniform asset turns, coupled with generally stable Uniform earnings margin.

Uniform turns were maintained at 1.6x-1.8x levels from 2005-2009, before fading to 1.3x levels in 2011-2012. Then, after recovering to 1.5x in 2016, Uniform turns regressed to a low of 1.0x in 2017 and rebounded to 1.8x highs in 2019-2020.

Meanwhile, Uniform margins gradually rose from 10% levels in 2005-2007 to a high of 15% in 2018, before falling to 11% in 2020.

At current levels, the market is pricing in expectations for both Uniform turns and Uniform margins to remain near current levels.

SUMMARY and Campbell Soup Company Tearsheet

As the Uniform Accounting tearsheet for Campbell Soup Company (CPB:USA) highlights, the Uniform P/E trades at 20.4x, which is around the global corporate average and its historical Uniform P/E of 21.9x.

Average P/Es require average EPS growth to sustain them. In the case of Campbell, the company has recently shown a 6% decline in Uniform EPS.

Wall Street analysts provide stock and valuation recommendations that provide very poor guidance or insight in general. However, Wall Street analysts’ near-term earnings forecasts tend to have relevant information.

We take Wall Street forecasts for GAAP earnings and convert them to Uniform earnings forecasts. When we do this, Campbell’s Wall Street analyst-driven forecast is a 2% EPS shrinkage in 2021 and a 1% EPS growth in 2022.

Based on current stock market valuations, we can use earnings growth valuation metrics to back into the required growth rate to justify Campbell’s $40 stock price. These are often referred to as market embedded expectations.

The company is currently being valued as if Uniform earnings were to have little to no growth annually over the next three years. What Wall Street analysts expect for Campbell’s earnings growth is below what the current stock market valuation requires in 2021 but above its requirement in 2022.

Furthermore, the company’s earning power is 3x the corporate average. However, cash flows and cash on hand are below its total obligations—including debt maturities, capex maintenance, and dividends. Together, this signals a high credit and dividend risk.

To conclude, Campbell’s Uniform earnings growth is above its peer averages. That said, the company is also trading below average peer valuations.

About the Philippine Market Daily

“Thursday Uniform Earnings Tearsheets – Global Focus”

Some of the world’s greatest investors learned from the Father of Value Investing or have learned to follow his investment philosophy very closely. That pioneer of value investing is Professor Benjamin Graham. His followers:

Warren Buffett and Charles Munger of Berkshire Hathaway; Shelby C. Davis of Davis Funds; Marty Whitman of Third Avenue Value Fund; Jean-Marie Eveillard of First Eagle; Mitch Julis of Canyon Capital; just to name a few.

Each of these great investors studied security analysis and valuation, applying this methodology to manage their multi-billion dollar portfolios. They did this without relying on as-reported numbers.

Uniform Adjusted Financial Reporting Standards (UAFRS or Uniform Accounting) is an answer to the many inconsistencies present in GAAP and IFRS, as well as in PFRS.

Under UAFRS, each company’s financial statements are rebuilt under a consistent set of rules, resulting in an apples-to-apples comparison. Resulting UAFRS-based earnings, assets, debts, cash flows from operations, investing, and financing, and other key elements become the basis for more reliable financial statement analysis.

Every Thursday, we focus on one multinational company that’s particularly interesting from a UAFRS vs as-reported standpoint. We highlight one adjustment that illustrates why the as-reported numbers are unreliable.

This way, we gain a better understanding of the factors driving a particular stock’s returns, and whether or not the firm’s true profitability is reflected in its current valuations.

Hope you’ve found this week’s Uniform earnings tearsheet on a multinational company interesting and insightful.

Stay tuned for next week’s multinational company highlight!

Regards,

Angelica Lim

Research Director

Philippine Markets Daily

Powered by Valens Research

www.valens-research.com