MONDAY MACRO: Have Philippine airline stocks been able to fly to recovery after the recent market selloff? Are they cheap now relative to the market?

This industry was one of the first affected by the outbreak of the novel coronavirus more than two months ago. When the COVID-19 pandemic was declared a global health emergency, this industry took an even greater hit as demand for domestic and international travel drastically declined.

Companies in this industry have already laid off a sizable percentage of their workforce to combat rising costs. However, with no clear timeline as to when the health crisis will be resolved, this industry may continue to suffer large losses indefinitely.

Below, we’ll take a look at two main players in this industry and how they fared during the recent Philippine stock market selloff.

Philippine Markets Daily:

The Monday Macro Report

Powered by Valens Research

Globally, the airline industry is one of the hardest hit by the COVID-19 pandemic.

Air travel was identified as one of the ways that the virus spread across different countries more than two months ago. Numerous countries and territories closed their borders as a precautionary measure against the spread of the disease.

Travel bans, coupled with steep declines in demand, have made it impossible for airlines to operate normally. With a limited source of revenue, airlines have to find ways to offset their massive fixed costs in order to survive this crisis.

Cebu Air, Inc. (CEB:PHL) and PAL Holdings Inc. (PAL:PHL), two of the main players in the Philippine domestic market, announced in March that they will cut down their workforce by over 150 and by 300 employees, respectively.

For Cebu Air, this cost reduction initiative was implemented to a lesser extent as prior to their lay-off announcement, its executives voluntarily took pay cuts.

Normally, if management thinks they can weather through the headwinds, one of the last actions they would take to manage their costs is lay off their employees.

Mass layoffs would cost the company more in the long-run due to the need to foster new talents and increase workforce as operation level improves. Workforce reduction, particularly during this time, implies management’s negative outlook in both the near and medium term.

However, the uncertainty surrounding this health crisis has raised concerns beyond simply the economic impact of temporarily suspending most airline operations.

Another area of concern is how soon leisure travel will return to its pre-COVID-19 norm.

According to the Philippine Department of Tourism, China is the second largest major consumer in the Philippine international travel volume, with 18% share of the total travel volume in 2018.

Since China is the original epicenter of the novel coronavirus, travel demand to China may take some time to recover to its original level even after regulatory restrictions are lifted.

Given the near-term dire outlook for air travel, what does this mean for the Philippine airline industry? Is the recent market selloff justifiable?

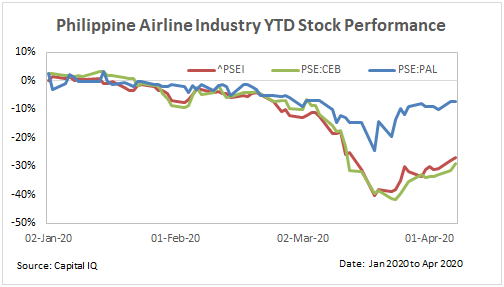

Market sentiments show limited concerns on industry-specific weaknesses. Year to date, Cebu Air’s stock price performance is in line with the Philippine stock market, even in March when the industry faced regulatory restrictions.

Cebu Air accumulated a loss of 59% in its market capitalization. PAL Holdings’ drop is much more limited, reaching a low of -36% in the same time period.

One would expect that these listed airline companies, particularly PAL Holdings, would drop much more than the Philippine stock index as travelling increases the risk of exposure of the virus.

Instead, the market appears to think that budget airline Cebu Air will suffer more losses than full-serviced airline PAL Holdings.

We take a look at the two companies’ historical ROA (return on assets) to understand how well or poorly managed they have been historically.

Cebu Air, Inc.

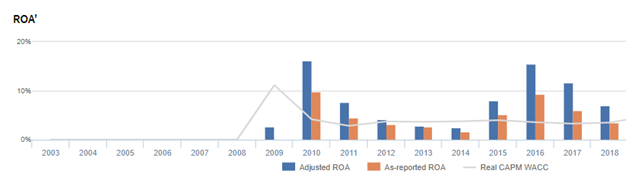

Cebu Air is more profitable when we use Uniform Accounting (blue bars) compared to the Philippine Financial Reporting Standards (PFRS, orange bars). The company has generally kept ROA above its cost of capital levels in seven out of ten years.

Although both Uniform and as-reported ROA have followed the same trend, Uniform ROA has always been higher than as-reported ROA. Quite notably, its latest Uniform ROA is double what as-reported metrics show.

Since 2015, Uniform ROA levels have grown above cost of capital levels and ranged from 7% to 15% whereas as-reported ROAs of the same period have a lower range of 4% to 9%.

PAL Holdings Inc.

PAL Holdings, however, has a different storyline, with ROAs generating consistently below cost of capital levels, making it more difficult for the company to absorb the economic shock or expand in normal conditions.

In five out of the last thirteen years, the company has experienced negative profitability, with a Uniform ROA ranging from -7% to 4%. Latest annual data shows the company had a 1% Uniform ROA in 2018.

Slower economic growth in the near to medium-term is highly likely given the current global health crisis. However, given the impact that the airline industry has on the Philippine economy, it is highly unlikely these companies will be left without any support.

According to the International Air Transport Association (IATA), the country could lose more than 400,000 jobs in the aviation industry. This is equivalent to reducing gross domestic product (GDP) by up to $3.75 billion.

If this industry is unable to get tax breaks or subsidies from the Philippine government, their capital-intensive nature may allow them to gain temporary liquidity relief through collateralization or disposition of their fleets.

The airline industry will continue to face challenges this year in terms of sales generation as overall travel demand recovery is expected to remain slow. Consumers are expected to take extra precautions, even after regulatory restrictions are lifted. International travel demand is also dependent on other countries’ ability to counter the pandemic.

However, bankruptcy risk is low for the industry even under this situation. It is likely that the government will intervene on some level given the industry’s contribution to the economy’s growth pre-COVID-19 and that there is room to further scale down their operations.

About the Philippine Market Daily

“The Monday Macro Report”

When just about anyone can post just about anything online, it gets increasingly difficult for an individual investor to sift through the plethora of information available.

Investors need a tool that will help them cut through any biased or misleading information and dive straight into reliable and useful data.

Every Monday, we publish an interesting chart on the Philippine economy and stock market. We highlight data that investors would normally look at, but through the lens of Uniform Accounting, a powerful tool that gets investors closer to understanding the economic reality of firms.

Understanding what kind of market we are in, what leading indicators we should be looking at, and what market expectations are, will make investing a less monumental task than finding a needle in a haystack.

Hope you’ve found this week’s macro chart interesting and insightful.

Stay tuned for next week’s Monday Macro report!

Regards,

Angelica Lim & Joel Litman

Research Director & Chief Investment Strategist

Philippine Markets Daily

Powered by Valens Research

www.valens-research.com