MONDAY MACRO: This chart shows how we’re not necessarily bound to repeat this particular history

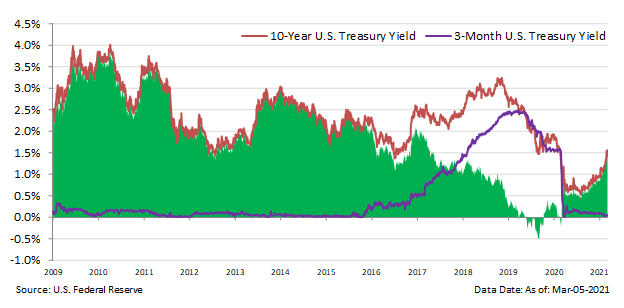

Last week, we discussed the rising bond yields and how it’s replicating the 2013 Taper Tantrum. Today, we’re taking a look at why such interest rates rose in 2013 and why they have been rising again in recent months.

While long-term U.S. interest rates then and now display similar behaviors, this chart shows that different circumstances caused them. As such, it’s unlikely we’ll see history repeat itself.

Philippine Markets Daily:

The Monday Macro Report

Powered by Valens Research

During the start of 2009, the United States continued to struggle amidst the Great Recession. GDP was contracting and unemployment was worsening, so the Federal Reserve reacted by drastically lowering the federal funds rate from 1.6% in February 2020 to 0.1% by April 2020.

The federal funds rate is the central bank’s main policy tool, mainly because it influences all other short-term interest rates in the United States. A lower federal funds rate means lower interest rates of bank loans. Corporations and households will then find it easier to borrow, which should stimulate economic growth.

However, the federal funds rate theoretically cannot go below zero. If banks needed to pay money to give out loans, then they would choose to not give out loans at all.

The federal funds rate during 2009 was already close to zero, but the economy was still contracting. This perplexed the Fed, so it resorted to adopting an unorthodox program at the time called Quantitative Easing (QE).

The aim of the QE program was to purchase large amounts of long-term bonds and other financial securities. By driving up demand for such financial assets, their prices rose and caused long-term interest rates (or yields) to fall.

In addition, the money supply circling in the economy expanded and pressured inflation to rise as a result. The combination of a lack of investment options due to low interest rates and rising inflation incentivized people to spend, which ultimately kick-started the U.S. economy’s recovery.

The QE program lasted for years. However, in 2013, Chairman of the Federal Reserve Ben Bernanke announced the possibility of reducing or tapering asset purchases starting in 2014.

This announcement took investors by surprise, leading many to think that the QE program would end earlier than expected. As discussed last week, the move led to a spike in the 10-year treasury yield from 1.7% in April 2013 to 3.0% in December 2013.

With investors expecting the long-term bond market to return to pre-QE levels, many exited their positions in other asset classes, causing the prices of other assets to fall massively. This event is known today as the 2013 Taper Tantrum.

The emerging markets, especially the Philippines, were one of the most affected by the 2013 Taper Tantrum. The Philippine Stock Exchange (PSE) saw its largest period of foreign selling during May 2013, with about PHP 148.2 billion leaving the country.

Furthermore, from the middle of May 2013 until the end of June 2013, the Philippine Stock Exchange Index (PSEi) lost 22% of its value.

Today, a lot of people are worried that another Taper Tantrum might occur. In April and May 2020, U.S. unemployment rate rose to historically high levels and the U.S. economy was headed towards deflation due to the COVID-19 pandemic.

Fortunately, the Federal Reserve quickly stepped in and executed another round of Quantitative Easing, which resulted in the 10-year U.S. treasury yields collapsing to a new historical low in 2020.

In 2021, 10-year U.S. treasury yields are once again creeping back up, from 0.9% at the start of the year to 1.6% currently. Meanwhile, the PSEi has declined 9% YTD. Both trends may be somewhat related, but it seems unlikely that we’ll see another Taper Tantrum with the same magnitude in 2013.

For one, the Federal Reserve has maintained the stance of continuing its asset purchases since its objectives have not yet been met. The U.S. unemployment rate remains above pre-pandemic levels and the U.S. inflation rate is still below the 2% target.

Moreover, foreign investors have mostly been net sellers (gray bars) in the PSE since mid-2019. Coupled with the fact that foreign ownership of PSE equities (yellow line) is near historical lows at 29%, there seems to be little room left for another foreign-driven sell-off. The PSEi (blue line) did make a rally in October 2020, but it was mostly driven by local investors.

Even when looking at the aggregate Uniform data of the PSE, we see that current Uniform P/Es (Fwd V/E’) are lingering below recent average valuations and 2013 levels specifically.

This is not to say that further downside is impossible. There are other matters that should be paid attention to such as the pace of COVID-19 vaccination, the return of certain quarantine restrictions, and high inflation, but it seems unlikely that any further downside will come from another Taper Tantrum event.

About the Philippine Market Daily

“The Monday Macro Report”

When just about anyone can post just about anything online, it gets increasingly difficult for an individual investor to sift through the plethora of information available.

Investors need a tool that will help them cut through any biased or misleading information and dive straight into reliable and useful data.

Every Monday, we publish an interesting chart on the Philippine economy and stock market. We highlight data that investors would normally look at, but through the lens of Uniform Accounting, a powerful tool that gets investors closer to understanding the economic reality of firms.

Understanding what kind of market we are in, what leading indicators we should be looking at, and what market expectations are, will make investing a less monumental task than finding a needle in a haystack.

Hope you’ve found this week’s macro chart interesting and insightful.

Stay tuned for next week’s Monday Macro report!

Regards,

Angelica Lim

Research Director

Philippine Markets Daily

Powered by Valens Research

www.valens-research.com