The sole operator of 7-Eleven stores in Thailand continues to expand its stores around Asia, resulting in a 17% Uniform ROA!

This company is the sole operator of 7-Eleven convenience stores in Thailand. Recently, it acquired a master franchise agreement to also oversee 7-Eleven stores in both Cambodia and Laos.

However, as-reported metrics do not seem to agree that the company’s strategic store expansions are enough to lead to robust returns. Uniform Accounting shows that this company has stronger returns than what the market thinks.

Also below, Uniform Accounting Embedded Expectations Analysis and the Uniform Accounting Performance and Valuation Tearsheet for the company.

Philippine Markets Daily:

Wednesday Uniform Earnings Tearsheets – Asia-listed Focus

Powered by Valens Research

A trademark is a word, a phrase, or a symbol that makes a product recognizable and differentiated from other products of its kind in the market. In other words, it helps identify which company owns a specific product or service. It helps build customer trust, giving them the confidence that the product they are getting is authentic and of a certain quality.

Trademarks prohibit others from using a company’s products and services without its permission. For an individual or another business entity to use a trademark, a trademark licensing agreement is required.

A common type of licensing agreement is a franchising agreement.

A franchise is a license that allows the franchisee to use the franchisor’s trademarks (name, logo, phrase, etc.), business model, advertising and marketing, and other business elements associated with the franchisor’s operations. In return, the franchisor gets an initial payment for this and also succeeding license fees.

One of the most commonly franchised types of businesses are convenience stores. Previously, we’ve talked about two well-known convenience store brands originating from Japan, FamilyMart and Lawson.

Today we will discuss the company that was able to obtain a master franchise arrangement with 7-Eleven, Inc. Master franchising is a franchising agreement wherein the master franchisor grants the franchisee rights to develop its business in a certain region.

CP ALL Public Company Limited is the sole operator of 7-Eleven in Thailand.

As of 2019, Thailand is second in the world in terms of number of 7-Eleven stores, next to Japan. CP ALL has been able to continuously expand the number of 7-Eleven branches in Thailand, opening 724 stores in 2019 and bringing the total to more than 11,700 stores.

Since convenience store chains are a type of franchise business, it’s only normal for them to expand exponentially. However, what CP ALL has done differently is enhance its existing stores to retain customers, while at the same time broaden its network. The company also operates the businesses complementing 7-Eleven, such as bill payment collection services, logistics services, information technology services, and more.

Normally, in order for a brand to attract more customers, it must differentiate itself from its competitors. CP ALL differentiates its products and services in a way that is unique to other convenience stores in the country.

The company puts more focus on serving consumers’ needs by first, producing more food and drink products that have more nutritional value for the health-conscious customers. Second, CP ALL innovates its technology, facilities, and equipment within stores. Instead of just selling consumer goods, the company provides convenient services such as ATMs or allowing the customer to be able to pay utility bills or credit cards and bank loans.

Moreover, CP ALL has also kept up with technological advancements such as going cashless, providing its customers with alternative payment methods like Alipay, UnionPay, credit cards, or e-wallet mobile payment applications.

CP ALL also launched a 24-hour delivery service called “SPEED-D” and an “ALL Member” loyalty program for its customers.

With these strategies, one might expect the company to have generated robust profitability given its wide reach nationwide.

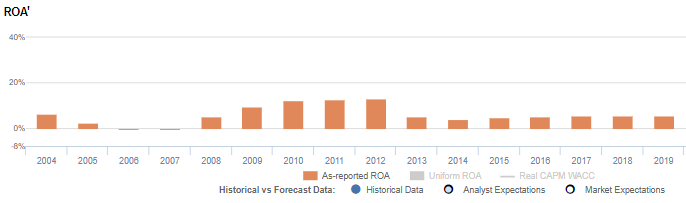

However, as-reported metrics show that the business is weak, indicating that having a master franchise for a whole country is not translating to strong returns. Currently, the company’s as-reported ROA is at 6%.

This is not an accurate picture of CP ALL’s profitability.

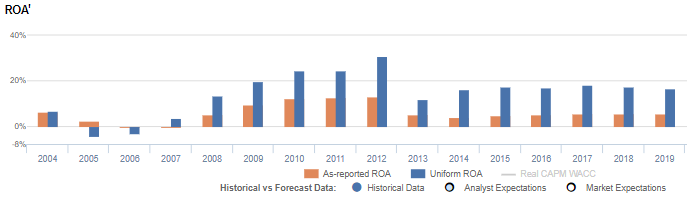

Uniform Accounting shows that the company actually has stronger returns, and that its strategic innovations and store expansions are working. Currently, its Uniform ROA is sitting at 17%.

One of the things that as-reported metrics failed to consider is the company’s goodwill and other intangible assets, which caused the distortions between Uniform and as-reported ROAs.

Goodwill and other intangibles are purely accounting-based and unrepresentative of the company’s actual operating performance. When as-reported accounting includes this in a company’s balance sheet, it creates an artificially inflated asset base.

As a result, as-reported ROAs are not showing the real strength of CP ALL’s earning power. After goodwill and other intangibles adjustments were made, we can see that the company does not really have lackluster performance. In fact, it is performing well with a Uniform ROA that is 3x more robust than as-reported.

CP ALL Public Company Limited’s profitability is more robust than you think

As-reported metrics are distorting the market’s perception of the firm’s profitability. If you were to just look at as-reported ROA, you would think that the company is a weaker business than real economic metrics show.

CP ALL’s Uniform ROA has been higher than its as-reported ROA in the past thirteen years. For example, Uniform ROA was 17% in 2019, while as-reported ROA was only 6%.

The company’s Uniform ROA for the past thirteen years has ranged from 4% to 31%, while as-reported ROA has ranged only from immaterial levels to 13% in the same timeframe.

From negative levels in 2005-2006, Uniform ROA rose to a peak of 31% in 2012 before falling to 12% in 2013. Uniform ROA then stabilized at 16%-18% levels through 2019.

CP ALL Public Company Limited’s Uniform earnings margins are weaker than you think, but its Uniform asset turns make up for it

Volatility in Uniform ROA has been driven by trends in Uniform earnings margins and Uniform asset turns, with peaks and troughs lining up historically with that of Uniform ROA.

From negative levels in 2005-2006, Uniform margins stabilized at 4%-6% levels through 2019. Meanwhile, Uniform turns dropped from 11.3x in 2004 to 3.6x in 2008, before gradually climbing to 8.2x in 2012. Since then, Uniform turns have faded to 3.2x-3.4x levels through 2019.

SUMMARY and CP ALL Public Company Limited Tearsheet

As the Uniform Accounting tearsheet for CP ALL Public Company Limited (CPALL:THA) highlights, its Uniform P/E trades at 29.1x, which is above the global corporate average of 25.2x but below its historical average of 31.5x.

High P/Es require high EPS growth to sustain them. In the case of CP ALL, the company has recently shown a 10% Uniform EPS growth.

Sell-side analysts provide stock and valuation recommendations that in general provide very poor guidance or insight. However, sell-side analysts’ near-term earnings forecasts tend to have relevant information.

We take sell-side forecasts for Thai Financial Reporting Standards (TFRS) earnings and convert them to Uniform earnings forecasts. When we do this, CP ALL’s sell-side analyst-driven forecast is a 23% earnings shrinkage in 2020, followed by an 18% earnings growth in 2021.

Based on the current stock market valuations, we can use earnings growth valuation metrics to back into the required growth rate to justify CP ALL’s THB 61.75 stock price. These are often referred to as market embedded expectations.

To justify current valuations, the company’s earnings need to grow by 6% per year over the next three years. What sell-side analysts expect for CP ALL’s earnings is below what the current stock market valuation requires in 2020, but above its requirement in 2021.

The company’s earning power is 3x the corporate average. That said, cash flows and cash on hand are below its total obligations. Together, this signals a moderate dividend and credit risk.

To conclude, CP ALL’s Uniform earnings growth is in line with its peer averages in 2020, and the company is trading well above its peer valuations.

About the Philippine Market Daily

“Wednesday Uniform Earnings Tearsheets – Asia-listed Focus”

Some of the world’s greatest investors learned from the Father of Value Investing or have learned to follow his investment philosophy very closely. That pioneer of value investing is Professor Benjamin Graham. His followers:

Warren Buffett and Charles Munger of Berkshire Hathaway; Shelby C. Davis of Davis Funds; Marty Whitman of Third Avenue Value Fund; Jean-Marie Eveillard of First Eagle; Mitch Julis of Canyon Capital; just to name a few.

Each of these great investors studied security analysis and valuation, applying this methodology to manage their multi-billion dollar portfolios. They did this without relying on as-reported numbers.

Uniform Adjusted Financial Reporting Standards (UAFRS or Uniform Accounting) is an answer to the many inconsistencies present in GAAP and IFRS, as well as in PFRS.

Under UAFRS, each company’s financial statements are rebuilt under a consistent set of rules, resulting in an apples-to-apples comparison. Resulting UAFRS-based earnings, assets, debts, cash flows from operations, investing, and financing, and other key elements become the basis for more reliable financial statement analysis.

Every Wednesday, we focus on one company listed in Asia that’s relevant to the Philippines and that’s particularly interesting from a UAFRS vs as-reported standpoint. We highlight one adjustment that illustrates why the as-reported numbers are unreliable.

This way, we gain a better understanding of the factors driving a particular stock’s returns, and whether or not the firm’s true profitability is reflected in its current valuations.

Hope you’ve found this week’s Uniform Earning Tearsheet on an Asian company interesting and insightful.

Stay tuned for next week’s Asia company highlight!

Regards,

Angelica Lim

Research Director

Philippine Markets Daily

Powered by Valens Research

www.valens-research.com