This Taiwanese company is setting healthier eating standards. Earning power is almost 2x as-reported returns!

Healthy eating has been gaining a lot of traction in the Philippines, as millennials are becoming the “wellness generation.” According to a survey conducted by Herbalife Nutrition in 2016, seven out of 10 Filipino millennials strive to live healthy.

One go-to breakfast for a healthy diet is oatmeal because of its high fiber content, which is good for the heart, stomach, and bowels. Moreover, oats are nutritious and contain antioxidants, and they can improve cholesterol levels and blood sugar control.

Quaker Oats has been a staple name for instant oatmeal in the Philippines, Taiwan, and around the world.

This company is committed to promoting healthy foods, and they produce, distribute, and market Quaker products in Taiwan.

Also below, Uniform Accounting Embedded Expectations Analysis and the Uniform Accounting Performance and Valuation Tearsheet for the company.

Philippine Markets Daily:

Wednesday Uniform Earnings Tearsheets – Asia-listed Focus

Powered by Valens Research

Health and wellness is an important factor considered by global consumers nowadays. Given the health issues in our environment today, consumers are starting to invest in their health.

According to Nielsen Global Survey, 72% of global consumers responded that they would buy foods that include “superfoods.”

Superfoods is a term used for food that has a lot of health benefits because of their nutrient density.

One company in Asia that benefits from the shift in the trend towards superfoods is Standard Foods Corporation.

Standard Foods is a company that has the rights to Quaker Oats products in Taiwan. They also sell powdered milk, baby food, drinking water, and herbal drinks.

Quaker Oats, a brand that is internationally famous for their oatmeals, started promoting their products in Taiwan as part of their global expansion in 1978. They invested $4 million for a food factory, Quaker Products Taiwan Ltd.

In 1986, Standard Foods Taiwan Ltd. was established after purchasing the Taiwan-based subsidiary of Quaker Oats. It also acquired the rights to produce, distribute, and market Quaker products in the country.

In 2002, they changed their name to Standard Foods Corporation.

Standard Foods has been committed to producing healthy products with the highest quality since day one. Their dedication to providing healthy options in the market paved the way for their portfolio expansion.

Mentos candies and Great Day cooking products were included in the company’s portfolio in 1988.

In the same year, Standard Foods launched Great Day Sunflower Oil, giving the consumers a healthier cooking option. For over two decades, it has been the top-selling edible oil in Taiwan.

In 1994, the company launched the first calcium-enriched non-fat milk powder in Taiwan. With the help of this product, Quaker brand rose to the top of the low-fat and non-fat milk powder industry.

Standard Foods also started offering herbal tonic drinks with Chinese herbal medicines to the market in 1997.

Aside from oatmeals, edible oil, and tonic drink, the company also offers baby foods, ranging from non-staple food, baby’s milk, nutritional supplements, and tonic drinks for children.

The company’s offerings reflect their focus on their number one goal: to create products of superior quality that improve consumers’ lives. This is evident in the offerings that they have in the market.

One of the company’s key cornerstones to growth is innovation, and given the track record of their offerings, they have succeeded innovating their products every time.

While as-reported metrics do not exactly reflect the strength of Standard Foods’ offerings and innovation, Uniform metrics do.

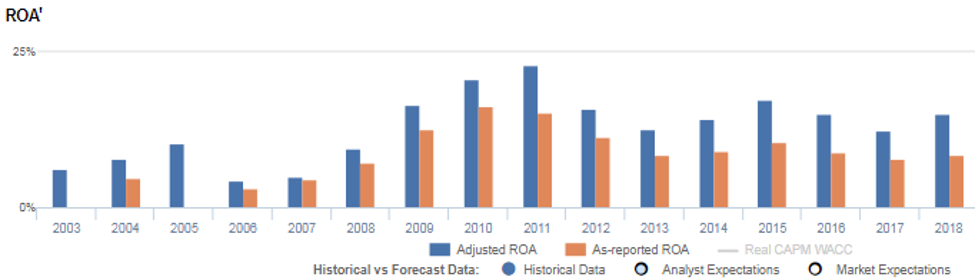

From 2010 to 2018, as-reported ROA ranged from 8% to 16%, materially lower than the Uniform ROA range of 12% to 23%. This indicates that Standard Foods is delivering a better performance than what the market perceives.

The increasing demand for healthier foods from the evolving consumer behavior may not be priced in by the market, distorting Standard Foods’ TRUE profitability.

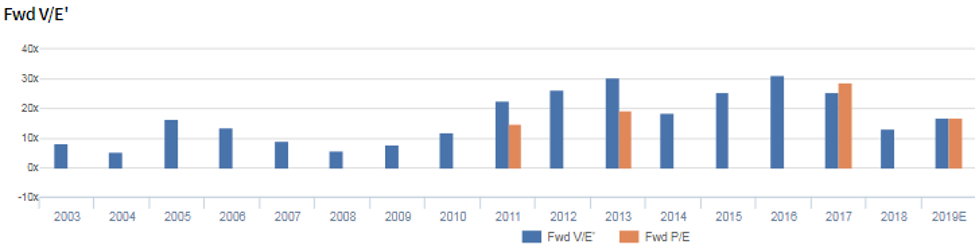

Standard Foods’ Uniform valuation is in line with the market

Standard Foods Corporation (1227:TAI) currently trades below corporate and historical averages with a 17.0x Uniform P/E (blue bars), but in line with the as-reported P/E of 17.1x (orange bars).

At these levels, the market is pricing in expectations for Uniform ROA to remain at 15% levels in 2023, accompanied by a 4% Uniform asset growth going forward.

However, analysts project Uniform ROA to rise to 18% in 2019, accompanied by a 3% Uniform asset growth.

Standard Foods’ profitability is actually better than you think it is

Standard Foods’ profitability has been cyclical, with Uniform ROA ranging from 4% to 23% over the past 16 years.

After rising from 6% in 2003 to 10% in 2005, Uniform ROA fell to a low of 4% in 2006, before slowly rising to historical highs of 23% in 2011. Uniform ROA then fell to 13% in 2013, before increasing to 17% in 2015. After decreasing to 12% in 2017, Uniform ROA rebounded to 15% in 2018.

Meanwhile, Uniform asset growth has been positive for the past 16 years, while ranging from 0% to 31%.

As-reported metrics are understating Standard Foods’ profitability.

For example, as-reported ROA was 8% in 2018, materially lower than Uniform ROA of 15%, making the company look like a weaker business than real economic metrics highlight.

Moreover, Uniform ROA has been higher than as-reported ROA for the past 16 years, significantly distorting the market’s perception of the firm’s historical profitability trends.

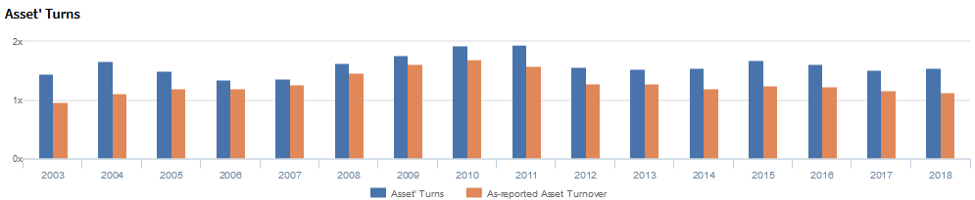

Standard Foods’ asset turns are stronger than you think

Cyclicality in Uniform ROA has been driven primarily by trends in Uniform asset turns, with peaks and troughs lining up historically with that of Uniform ROA.

Uniform asset turns increased from 1.4x in 2003 to 1.7x in 2004 before falling to 1.4x in 2007. Thereafter, Uniform asset turns rose to a historical high of 2.0x in 2011, before dropping to 1.6x in 2012. Uniform asset turns stabilized at 1.5x to 1.7x from 2013 to 2018, with the company having a 1.6x Uniform asset turns in 2018.

Summary and Standard Foods Tearsheet

As the Uniform Accounting tearsheet for Standard Foods highlights, they are trading at 17.0x Uniform P/E, which is below market average valuations and historical average levels.

Low P/Es require low EPS growth to sustain them. In the case of Standard Foods, the company has recently shown a 26% Uniform EPS growth.

Sell-side analysts provide stock and valuation recommendations that in general provide very poor guidance or insight. However, sell-side analysts’ near-term earnings forecasts tend to have relevant information.

We take sell-side forecasts for Taiwan Financial Supervisory Commission: International Financial Reporting Standards (TIFRS) earnings and convert them to Uniform earnings forecasts. When we do this, Standard Foods’ sell-side analyst-driven forecast is for Uniform earnings to grow by 28% in 2019 and 9% in 2020.

Based on current stock market valuations, we can back into the required earnings growth rate that would justify TWD 67.90 per share. These are often referred to as market embedded expectations.

In order to meet the current market valuation levels of Standard Foods, the company would have to have Uniform earnings grow by 1% each year over the next three years. What sell-side analysts expect for Standard Foods earnings growth is well above what the current stock market valuation requires.

To conclude, Standard Foods’ Uniform earnings growth is above peer averages in 2019. Moreover, the company is trading below peer average valuations.

The company’s earning power, based on its Uniform return on assets calculation, is at least 2x corporate average returns. Furthermore, with cash flows and cash on hand consistently exceeding obligations, Standard Foods has low credit and dividend risk.

About the Philippine Market Daily

“Wednesday Uniform Earnings Tearsheets – Asia-listed Focus”

Some of the world’s greatest investors learned from the Father of Value Investing or have learned to follow his investment philosophy very closely. That pioneer of value investing is Professor Benjamin Graham. His followers:

Warren Buffett and Charles Munger of Berkshire Hathaway; Shelby C. Davis of Davis Funds; Marty Whitman of Third Avenue Value Fund; Jean-Marie Eveillard of First Eagle; Mitch Julis of Canyon Capital; just to name a few.

Each of these great investors studied security analysis and valuation, applying this methodology to manage their multi-billion dollar portfolios. They did this without relying on as-reported numbers.

Uniform Adjusted Financial Reporting Standards (UAFRS or Uniform Accounting) is an answer to the many inconsistencies present in GAAP and IFRS, as well as in PFRS.

Under UAFRS, each company’s financial statements are rebuilt under a consistent set of rules, resulting in an apples-to-apples comparison. Resulting UAFRS-based earnings, assets, debts, cash flows from operations, investing, and financing, and other key elements become the basis for more reliable financial statement analysis.

Every Wednesday, we focus on one company listed in Asia that’s relevant to the Philippines and that’s particularly interesting from a UAFRS vs as-reported standpoint. We highlight one adjustment that illustrates why the as-reported numbers are unreliable.

This way, we gain a better understanding of the factors driving a particular stock’s returns, and whether or not the firm’s true profitability is reflected in its current valuations.

Hope you’ve found this week’s Uniform Earning Tearsheet on an Asian company interesting and insightful.

Stay tuned for next week’s Asia company highlight!

Regards,

Angelica Lim & Joel Litman

Research Director & Chief Investment Strategist

Philippine Markets Daily

Powered by Valens Research

www.valens-research.com