With Uniform ROAs of over 15%, this online review platform is definitely deserving of a 5-star review

Nowadays, it’s rare for people to go out and try something new without checking reviews online first.

Thankfully, this online review platform makes it easier to do just that with its library of over 200 million crowd-sourced reviews on traditional brick-and-mortar businesses and local service providers.

However, looking at as-reported metrics, it seems that the company has little to no success from bringing in-person recommendations to the web. In reality, Uniform Accounting reveals the opposite, with returns that have been above cost-of-capital levels.

Also below, Uniform Accounting Embedded Expectations Analysis and the Uniform Accounting Performance and Valuation Tearsheet for the company.

Philippine Markets Daily:

Thursday Uniform Earnings Tearsheets – Global Focus

Powered by Valens Research

In this digital age, information is always just a quick internet search away—it’s what makes it easier for us to make decisions.

Before the internet, the only way to find out whether a movie was good or a restaurant was worth going to was through word of mouth. Now, we have Yelp (YELP:USA).

Yelp (a combination of the words “help” and “yellow pages”) was developed in 2004 when Jeremy Stoppelman, one of the company’s co-founders, had the flu and found it incredibly difficult to find an online recommendation for a doctor in his local area.

The initial business idea was for the company to be an email-based referral network. So, after getting the go signal and receiving a $1 million investment from their former boss at Paypal, Jeremy Stoppelhan, together with Russel Simmons, worked together to bring the concept of “word of mouth” online.

With Yelp, users can email each other to ask for recommendations on specific places. However, the business didn’t turn out to be as revolutionary as they had hoped. It appeared no one was willing to freely hand out their personal email addresses–the company’s user base didn’t go beyond the founders’ friends and family.

Venture capital investors were starting to lose interest in the company’s business, so the two founders re-evaluated Yelp and looked for features they could improve. As it turned out, according to their user data, Yelp’s unsolicited reviews feature had more submissions than their email-requested reviews.

Switching the company’s focus to “real reviews” turned out to be a smart decision, with the company growing from a couple thousand users in 2005 to over 140 million in 2021, and accumulating over 220 million reviews.

…a reach that massively displays just how powerful Yelp’s network effects are.

As a refresher, having network effects means that a platform becomes more valuable the more people use it. This is common for social media apps or crowdsourcing platforms like Google or TripAdvisor where the user base is a critical component of the business.

While Yelp is competing against behemoths like Google, its network effect is how it maintains a dominant position. Simply put, people go to Yelp versus Google or elsewhere for reviews because Yelp has more review data.

Additionally, Yelp has consistently found ways to add new features to make it even harder to switch platforms. It acquired companies such as SeatMe, an online restaurant reservation platform, and Eat24, a food delivery company, to offer services beyond just reviews.

Yelp has become a significant tool in the everyday lives of individuals as it connects people with almost every type of local business, from restaurants, boutiques and salons to dentists, mechanics, plumbers, and more.

These reviews are written by people using Yelp to share their everyday local business experiences, giving voice to consumers and bringing “word of mouth” online.

That being said, analysts who take a look at Yelp’s as-reported financials would think the company’s network effects aren’t as powerful as expected.

In reality, the company has actually been consistently generating positive Uniform ROAs since 2013, save for 2020 when the company was impacted significantly by country-wide lockdowns.

This shows how Yelp’s continued focus to grow their network and enhance their services has created robust returns for their business.

The distortion comes from as-reported metrics incorrectly treating R&D as an expense. In recent years, Yelp’s R&D expense stood at around $230 million, about 25% of its total operating expenses.

In reality, R&D is an investment in the long-term cash flow generation of the company. Recording R&D as an expense violates one of the core principles of accounting, which is that expenses should be recognized in the period when the related revenue is reported.

Since as-reported accounting records R&D on the income statement, as opposed to as an investment on the balance sheet, net income can become materially understated.

As in the case of Yelp, as-reported ROAs are not capturing the true strength of the company’s earning power. Adjusting for R&D, you get returns that are greater than what is actually shown. Without this adjustment, it would appear that Yelp had been less successful with its R&D investments than it really is, leading to poorer valuations.

Yelp is actually more profitable than you think it is

As-reported metrics distort the market’s perception of the firm’s recent profitability. If you were to just look at as-reported ROA, you would think the company is a much weaker business than real economic metrics highlight.

Yelp’s Uniform ROA has actually been higher than its as-reported ROA in the past twelve years. For example, Uniform ROA was at 0% in 2020, while as-reported ROA was at -2%.

Specifically, Yelp’s Uniform ROA has ranged from -8% to 25% in the past twelve years while as-reported ROA has ranged from only -17% to 2% levels in the same timeframe.

Uniform ROA declined from 7% in 2009 to -8% in 2010, before inflecting positively and expanding to a peak of 25% in 2014. Since then, however, Uniform ROA has collapsed back to negative levels in 2020, amidst pandemic-related headwinds.

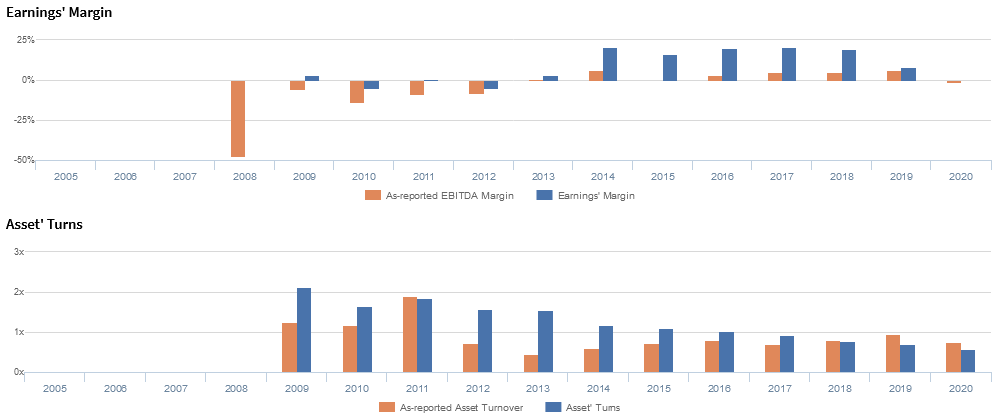

Yelp’s Uniform earnings margins and Uniform asset turns are much stronger than you think

Trends in Uniform ROA have been driven largely by trends in Uniform earnings margins, accompanied by declining Uniform asset turns.

After falling from 3% in 2009 to negative levels in 2010 and 2012, Uniform margins improved to a peak of 21% in 2014. Then, Uniform margins faded to 16% in 2015, before recovering to 21% in 2017 and subsequently falling to negative levels in 2020.

Meanwhile, since 2009, Uniform turns have steadily compressed from 2.1x to 0.6x in 2020.

At current valuations, markets are pricing in expectations for Uniform margins to rebound towards recent averages and for Uniform turns to stabilize near historical lows.

SUMMARY and Yelp Inc. Tearsheet

As our Uniform Accounting tearsheet for Yelp Inc. (YELP:USA) highlights, the Uniform P/E trades at 78.2x, which is above the global corporate average of 23.7x and its historical median Uniform P/E of 34.6x.

High P/Es require high EPS growth to sustain them. In the case of Yelp, the company has recently shown a 101% Uniform EPS decline.

Wall Street analysts provide stock and valuation recommendations that provide very poor guidance or insight in general. However, Wall Street analysts’ near-term earnings forecasts tend to have relevant information.

We take Wall Street forecasts for GAAP earnings and convert them to Uniform earnings forecasts. When we do this, Yelp’s Wall Street analyst-driven forecast is a 3,450% and a 207% EPS growth in 2021 and 2022, respectively.

Furthermore, the company’s earning power is below the long-run corporate average. However, cash flows and cash on hand are around 3x its total obligations—including debt maturities and capex maintenance. Together, this signals a moderate credit risk.

To conclude, Yelp’s Uniform earnings growth is above its peer averages. Therefore, as is warranted, the company is also trading above average peer valuations.

About the Philippine Markets Daily

“Thursday Uniform Earnings Tearsheets – Global Focus”

Some of the world’s greatest investors learned from the Father of Value Investing or have learned to follow his investment philosophy very closely. That pioneer of value investing is Professor Benjamin Graham. His followers:

Warren Buffett and Charles Munger of Berkshire Hathaway; Shelby C. Davis of Davis Funds; Marty Whitman of Third Avenue Value Fund; Jean-Marie Eveillard of First Eagle; Mitch Julis of Canyon Capital; just to name a few.

Each of these great investors studied security analysis and valuation, applying this methodology to manage their multi-billion dollar portfolios. They did this without relying on as-reported numbers.

Uniform Adjusted Financial Reporting Standards (UAFRS or Uniform Accounting) is an answer to the many inconsistencies present in GAAP and IFRS, as well as in PFRS.

Under UAFRS, each company’s financial statements are rebuilt under a consistent set of rules, resulting in an apples-to-apples comparison. Resulting UAFRS-based earnings, assets, debts, cash flows from operations, investing, and financing, and other key elements become the basis for more reliable financial statement analysis.

Every Thursday, we focus on one multinational company that’s particularly interesting from a UAFRS vs as-reported standpoint. We highlight one adjustment that illustrates why the as-reported numbers are unreliable.

This way, we gain a better understanding of the factors driving a particular stock’s returns, and whether or not the firm’s true profitability is reflected in its current valuations.

Hope you’ve found this week’s Uniform earnings tearsheet on a multinational company interesting and insightful.

Stay tuned for next week’s multinational company highlight!

Regards,

Angelica Lim

Research Director

Philippine Markets Daily

Powered by Valens Research

www.valens-research.com