How a grandfather running $500 million taught his grandson now running $100 billion

On a warm summer day in New York City, a teenager and his grandfather are walking down the street…

They pass by a hot dog stand and the young teenager, who had forgotten his wallet, asks his grandfather if he could borrow $1 to buy one.

The older man famously replies: “Do you realize that if you invest that dollar wisely it will double every 5 years? By the time you reach my age, in 50 years, your dollar will be worth $1,024. Are you so hungry you need to eat a $1,000 hot dog?”

The grandfather’s name was Shelby Cullom Davis, one of the greatest investors the world has ever known.

The grandson, who surely took his grandfather's wisdom to heart, was Christopher Davis, who now manages tens of billions of outside client money.

Annual return higher than Buffett - 23% over 47 years

Born in Peoria, Illinois in 1909, Shelby Davis began his investing career in 1947.

Interestingly, the graduate of Princeton and Columbia never received any sort of formal investment training, yet he established his own firm, Shelby Cullom Davis & Company, by borrowing money equivalent to today’s $100,000 from his wife.

In addition to serving as the American Ambassador to Switzerland under Presidents Richard Nixon and Gerald Ford, Shelby Davis managed to turn this initial $100,000 into a $1.6 billion fortune, a feat that put him on the Forbes 400 wealthiest individuals list.

At the time of his death in 1994, he had achieved a staggering annual return of 23% over 47 years, making him one of the most successful investors of his time.

How did he achieve such incredible success over the market you might ask?

There are a number of important lessons modern investors can take away from the life of Shelby Davis:

-

The Power of Compound Interest

First is his insistence on utilizing what Albert Einstein deemed the “eighth wonder of the world,” compound interest. As the $1,000 hot dog story illustrates, Shelby understood better than most the power of investing over long periods of time and allowing returns to compound.

While most people don’t consider the opportunity cost of their everyday purchase decisions, Mr. Davis truly did. He knew that a dollar today is worth more than a dollar tomorrow, and made sure he focused his attention on putting money to work rather than spending on unnecessary -

The superiority of the Stock Market

Secondly, Shelby Davis believed that as an asset class, stocks are always the best long-term investment, despite the wild euphoria and pessimism of Wall Street. He viewed bear markets as opportunities to get bargains on great companies and took advantage of others’ fears.

-

It’s Never too Late to Start Investing

Shelby Davis, as successful as he was, did not start investing until he was 38 years old. He believed in a three-step process for investing - Learn, Earn, and Return, and bought companies that were well managed and poised for growth. He also only invested in businesses he understood and believed the key to success was holding for the long term.

-

Look for Opportunities Everywhere

In Davis’ eyes, the world was full of investment opportunities. He was one of the first American investors who looked to Japanese stocks and other foreign ventures, believing that investors should not constrain themselves, or their portfolios, to a single country.

Photo from Our American Network

Photo from Our American Network

Photo from

Photo from While all of these lessons are incredibly useful, there is one more Mr. Davis passed along that was by far the biggest and most important: the need for investors to restate as-reported financial statements.

As they followed Ben Graham’s footsteps, you can follow theirs...

While it may be a well-kept secret by the Davis family, Shelby was the man who actually coined the term “Uniform Accounting”. This incredible investor understood that generally accepted accounting standards are merely arbitrary rules which leave much to the discretion of bookkeepers.

Like many other great investors, he knew inconsistencies made comparing as-reported data futile and that by adjusting to a Uniform standard, a more consistent picture of the company in question could be obtained.

By using Uniform Accounting, Shelby Davis was able to see what others could not… a major reason for his success.

He also passed along these lessons to his children and grandchildren, who now manage tens of billions of dollars using the same techniques.

However, if one thing is certain it is that the Davis family is not going to share the secret to their investment machine. After all, they have kept Uniform Accounting under wraps for decades.

Since Shelby Davis senior’s passing, no single person has mentioned the words of Uniform Accounting, except for one...

Professor Joel Litman has been talking about Uniform Accounting for decades.

As Chief Investment Strategist and Managing Director here at Valens Research, he advises institutional investors in fundamental analysis of equities, corporate credit, and macroeconomic strategy.

He’s been on CNBC, quoted in Barron’s and Institutional Investor, and interviewed in Forbes.com. He has also published work on Uniform Accounting in Harvard Business Review and taught at some of the world’s most prestigious businesses schools.

By breaking down as-reported financials and discovering the true earnings power of companies across sectors, industries, and countries, Professor Litman’s work offers investors the potential to generate Shelby Davis-style returns.

We are now offering clients access to a portfolio modeled on Uniform Accounting data, one that will enable you to pick stocks Davis and many other investment greats would have bought and are still buying today...

Shouldn’t your clients benefit from this opportunity?

The way to do so is QGV50….

The Simple Framework that Unlocks Massive Returns

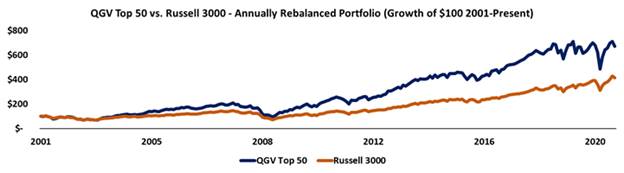

Valens Research’s powerful factor-based stock-picking model has proven to outperform the market significantly. The Russell 3000 has impressively gained a 400% return over the last 20 years. The QGV50 stocks have nearly DOUBLED that.

These factors that can help investors generate massive returns are just like the factors identified by

leaders such as Eugene Fama and Kenneth French thirty years ago. High quality, cheap stocks.

But with better data.

Generating alpha with these factors is no longer possible using traditional accounting data. GAAP and

IFRS mask the real quality, and the real value of the stocks investors are looking at.

Using Uniform Adjusted Financial Reporting Standards (UAFRS), we can get back to the roots of quality

investing.

The below chart tracks the performance of the UAFRS-driven Quality, Growth, and Valuation portfolio.

As you can see, this portfolio has generated sizable alpha. Investors won’t see returns near these levels

just by investing in the S&P 500 or Dow Jones.

For years, the investing greats have been competing with one another to drive outperformance. One

winning strategy many funds employ is factor investing. This methodology has grown in popularity as

quant funds have become more successful in the past few years.

Fama and French are credited with bringing factor investing to the common lexicon, starting with factors

such as size and valuation to model performance, eventually moving to quality, investment, and other

drivers. Today, investors around the world are using thousands of factors in the search for alpha.

But thanks to the numerous distortions inherent in GAAP and IFRS metrics, even the strongest factors

might miss the mark, due to the garbage-in, garbage-out nature of as-reported analysis.

At Valens, we know how little asset managers take stock in GAAP metrics. This is because nine out of the

top ten money managers in the world use Uniform data to drive their analysis.

Once the veil of as-reported accounting is lifted, the application of three intuitive factors leads to market

outperformance. When UAFRS is applied, even the simplest factors can drive alpha.

Combining UAFRS-based Quality, Growth, and Valuation factors, factors that have been around for

years, can create outperformance.

Quality is measured by UAFRS-based Return on Assets (ROA). Firms with a higher ROA are able to drive

better margins, asset turns, or a combination of the two, outperforming competitors.

Growth is measured by UAFRS-based asset growth. Businesses reinvesting in themselves.

And finally, Value is measured by simply looking for companies with low Uniform price to earnings (P/E)

ratios.

Firms who score well in all of these categories are strong, growing names the market has overlooked,

making them ripe for future outperformance.

And this outperformance is measurable. Over the past twenty years, investing purely with these UAFRS

factors has generated an 11.7% annual return, compared to the Russell 3000’s return of only 8.2%.

Now, Valens is selling the top fifty quality, growth, and valuation names in one report, for the low price

of $50 a year. Follow in the footsteps of Blackrock, Vanguard, Fidelity, and more by investing today.

This means each month, readers get fifty names just like Premier, Inc. (PINC)…

Premier operates in the health services industry, focusing on the integration of data and analytics, as well as supply chain and other consulting services.

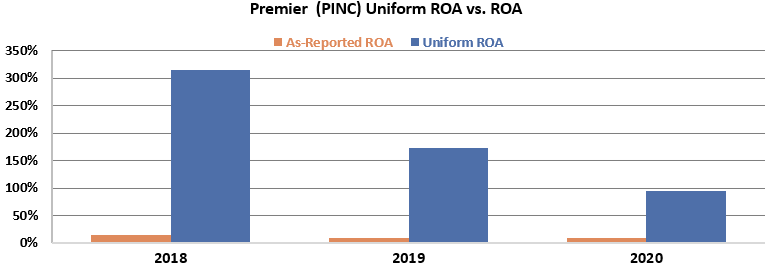

If investors viewed Premier through the lens of as-reported accounting, they would write off the firm’s performance.

Specifically, the firm’s as-reported return on asset (ROA) levels have fluttered around corporate averages, teetering around 10% to 14% levels over the past three years.

In reality, as you can in the below chart, Premier has been able to generate robust ROA at least ten times greater than GAAP returns.

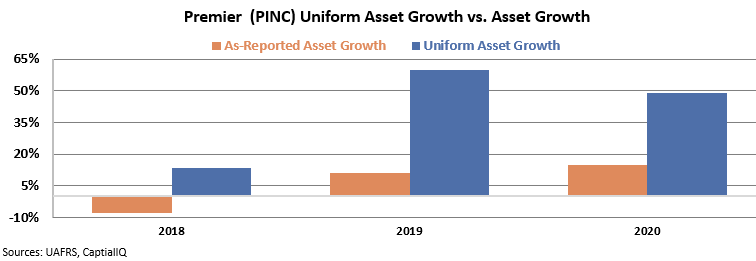

After determining the outstanding quality of the firm, we can then turn to its growth. The reason ROA levels have dropped off significantly is because Premier is investing heavily into its business.

And yet, GAAP accounting has failed to capture this. As-reported asset growth figures were negative in 2017, before expanding slightly into the 11% to 15% range since 2019. However, Uniform asset growth has been consistently strong. Specifically, Uniform asset growth has increased from 14% levels in 2018 to 49% levels in 2020.

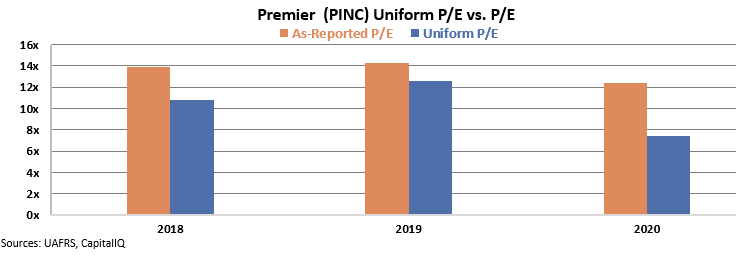

Finally, now that we can see Premier’s hidden strength, let us unpack valuations.

The market is pricing in Premier as a reasonable discount, with an as-reported P/E ranging from 12x to 14x over the past three years. However, on a Uniform basis, the company is even cheaper than it appears. Specifically, Uniform P/E levels have faded from 11x in 2018 to 8x in 2020.

This means investors are getting an incredibly high quality, high growth, CHEAP company, that would never have been found by looking at the as-reported metrics.

And again, this is just one example.

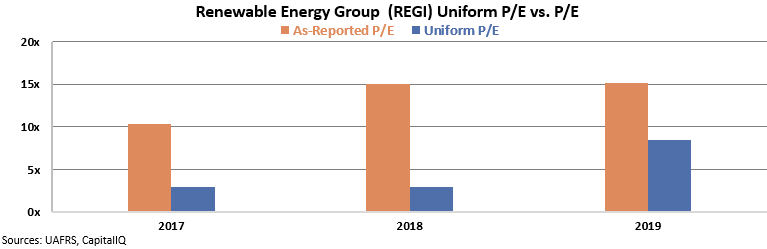

Another would be Renewable Energy Group (REGI). Renewable Energy Group engages in the production and trade of biofuel and renewable chemicals.

Despite having muted ROA levels in 2017, serious distortions become apparent in 2018 and beyond. Specifically, as-reported ROA levels have ranged from 18% to 19% levels since 2018. While these figures are robust, it does not do its justice on the true quality of Renewable Energy Group.

Uniform ROA levels were actually 29% in 2018 and 31% in 2019. This is more than 1.5x the as-reported metrics in their respective year.

See for yourself below.

Moving into the asset growth of the firm, there are slight differences amongst as-reported and Uniform accounting metrics. While as-reported metrics are slightly higher than the Uniform metrics, they are roughly in line with each other. Additionally, despite the wider gap in 2019, Uniform asset growth still shows a robust 33% rate.

Finally, the valuation of the company. Of the three factors, the valuation component may be the most compelling for this name.

Over the past three years, the market has been pricing in Renewable Energy Group at 10x to 15x multiples relative to earnings.

However, the Uniform P/E ratio highlights a different story; the firm is trading well below what as-reported metrics show. Before expanding to 9x in 2019, Uniform P/E was trading at 3x levels from 2017 to 2018.

By viewing Renewable Energy Group through a Uniform Accounting lens, investors are better able to recognize the high quality, high growth, and inexpensive company. This would never have been found by looking at the as-reported metrics.

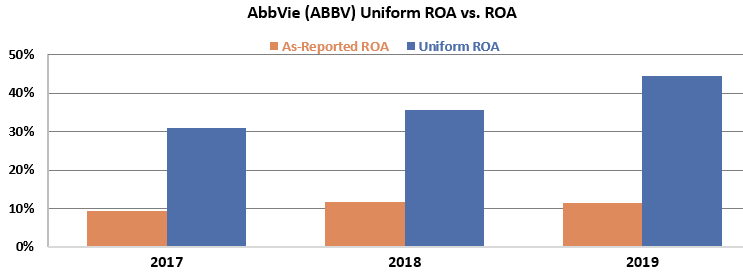

Our final example of a stellar QGV 50 name is AbbVie (ABBV). AbbVie is a research-based biopharmaceutical firm that develops drugs focused on treating blood cancers and autoimmune diseases.

If investors viewed this firm based on its as-reported metrics, they would never understand it would make a top 50 portfolio.

For example, as-reported ROA levels have ranged from 9% to 12% over the past three years, indicating the firm is generating returns near or below the corporate average. This makes it seem like AbbVie is a stereotypical firm.

In reality, AbbVie is generating robust returns. The company has been able to improve returns well above corporate averages. Over the past three years, Uniform ROA has grown from 30% to 45%.

Over the past three years, as-reported asset growth has vacillated between growing at 45% and shrinking by almost 20%. However, Uniform asset growth shows consistent growth, a good signal for a large pharmaceutical firm.

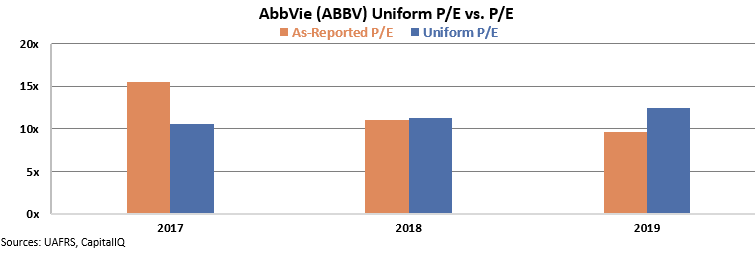

Diving deeper into the valuation of AbbVie, investors can see the firm trades at cheap valuations for such robust returns.

The Uniform P/E ratio shows despite slightly climbing valuations, AbbVie is still cheap 12x, well below corporate averages of 20x. While As-reported P/E shows a company only getting cheaper, Uniform Accounting shows investors are slowly coming around to the strength of the name.

Investors are blinded to AbbVie’s high quality, growth, and cheap valuation solely because they are viewing the wrong data. Instead of trusting the as-reported metrics of this company, investors should be asking to see the Uniform Accounting data.

These are just three examples of the fifty high quality and inexpensive names on the QGV 50.

With the portfolio updated every quarter, you can subscribe today to receive the 50 names identified by our Uniform powered factors today.