Valens Credit Weekly Insights for September 26, 2018

Credit and Market Mispricings

Most Compelling Credit v Equity Market Mispricings

AVP, CYH, MNI, NAV, UIS

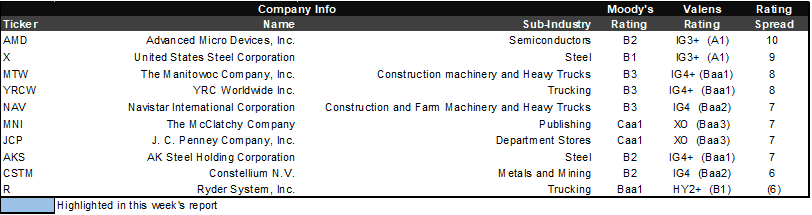

Most Compelling Credit Rating Dislocations

AKS, AMD, CSTM, JCP, MNI, MTW, NAV, R, X, YRCW

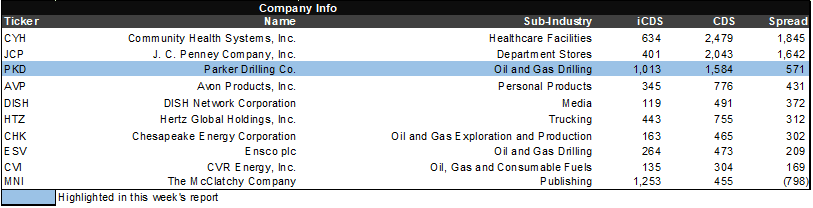

Most Compelling CDS Market Mispricings

AVP, CHK, CVI, CYH, DISH, ESV, HTZ, JCP, MNI, PKD

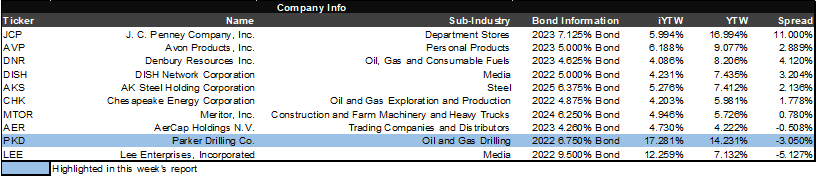

Most Compelling Bond Market Mispricings

AKS, AER, AVP, CHK, DISH, DNR, JCP, LEE, MTOR, PKD

Highlighted Top Ideas

GM – General Motors Company

MEG:CAN – MEG Energy Corp.

TMUS – T-Mobile US, Inc.

Other Recent Analyses

Consumer Discretionary

EXPE – Expedia Group, Inc.

Energy

PKD – Parker Drilling Company

Quantitative Credit Outlier Report Review

CYH tops our quantitative outlier report this week.

Aggregate Credit Market and Credit Fundamental Review

IG markets are currently fairly valued. HY markets have also moved to fairly valued levels, with iCDS converging towards CDS levels. However, the XO market appears mispriced. XO CDS appears to be overstating credit risk, with CDS levels not confirmed by iCDS. Overall, cost of borrowing have been rising thanks to improving economic activity and the rising risk free rate