Back in 2017, two of the largest chemical companies, DuPont de Nemours (DD) and Dow (DOW), merged to form DowDuPont. Within 18 months, they then dissolved into 3 separate companies, each focused on a different market segment.

From a business perspective, it makes a ton of sense.

By doing this, they wouldn’t be competing in areas that overlapped, and the portions they combined would have scale to remove redundant costs and get more pricing power. It was also an important step in avoiding pressure from regulators regarding antitrust concerns.

Ultimately, the DuPont portion of the business focuses on end markets like solar cell and semiconductor fabrication materials, LCD screen chemicals, and other technology end markets as well as safety, construction, and transportation offerings.

In theory, DuPont’s big-end markets have strong tailwinds. But these end markets, especially solar cells and semiconductors, are also highly cyclical boom and bust businesses.

Yet DuPont’s BBB+ rating from S&P prices it as though this cyclicality isn’t an issue.

However, we see things a little differently.

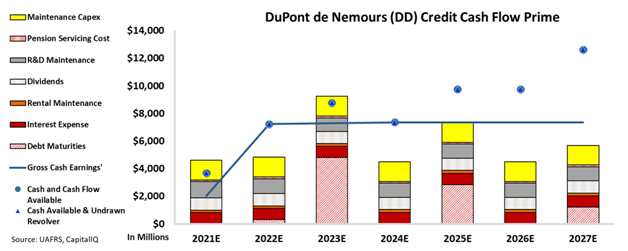

Using our Credit Cash Flow Prime (“CCFP”) framework, we can get to the heart of DuPont’s true fundamental credit risk.

In the chart below, the stacked bars represent the firm’s obligations each year for the next seven years. These obligations are then compared to the firm’s cash flow (blue line) as well as the cash on hand available at the beginning of each period (blue dots) and available cash and undrawn revolver (blue triangles).

As you can see, DuPont has multiple massive debt maturities within the next few years. This means it needs to make sure to refinance debt to be able to handle its obligations, especially with all the transactions it is exploring. While it has already begun this process, after a round of refinancing it’s still looking at a debt headwall of $4.8 billion by 2023.

Also worth noting is that the recovery rate has fallen below 100%, which is not a good sign for the business looking to refinance in a rising rate environment. Finally, when the bust cycle of semiconductors comes back after the recent boom, cash flows will be impacted.

Yet its BBB+ rating seems to miss all this risk.

That’s why we rate DuPont as having a much higher risk, with a high-yield rating of HY2. An HY2 rating translates to a default risk greater than 20% over the next five years, as DuPont struggles to refinance as rates continue to climb.

Using Uniform Accounting, we can see through the distortions of as-reported numbers to get to the true fundamental credit picture for companies in highly cyclical industries such as DuPont.

To see Credit Cash Flow Prime ratings for thousands of other companies we cover, click here to learn more about the various subscription options now available for the full Valens Database.

SUMMARY and DuPont de Nemours, Inc. Tearsheet

As the Uniform Accounting tearsheet for DuPont de Nemours, Inc. (DD:USA) highlights, the Uniform P/E trades at 14.8x, which is below the global corporate average of 24.0x and its historical P/E of 24.6x.

Low P/Es require Low EPS growth to sustain them. That said, in the case of DuPont, the company has recently shown 8% Uniform EPS shrinkage.

Wall Street analysts provide stock and valuation recommendations that in general provide very poor guidance or insight. However, Wall Street analysts’ near-term earnings forecasts tend to have relevant information.

We take Wall Street forecasts for GAAP earnings and convert them to Uniform earnings forecasts. When we do this, DuPont’s Wall Street analyst-driven forecast is for 78% and 13% EPS growth in 2021 and 2022, respectively.

Based on the current stock market valuations, we can use earnings growth valuation metrics to back into the required growth rate to justify DuPont’s $76 stock price. These are often referred to as market embedded expectations.

The company is currently being valued as if Uniform earnings were to grow by 4% over the next three years. What Wall Street analysts expect for Dupont’s earnings growth is above what the current stock market valuation requires in 2021 and 2022.

Meanwhile, the company’s earning power in 2020 is 2x the long-run corporate average. However, cash flows and cash on hand are below its total obligations. Additionally, intrinsic credit risk is 220bps above the risk-free rate. All in all, this signals a high credit and dividend risk.

Lastly, DuPont’s Uniform earnings growth is above peer averages and the company is trading below its peer average valuations.

Best regards,

Joel Litman & Rob Spivey

Chief Investment Strategist &

Director of Research

at Valens Research

This analysis of DuPont de Nemours, Inc.’s credit outlook is the same type of analysis that powers our macro research detailed in the FA Alpha Pulse.