Investors are constantly looking for macro and microeconomic trends that could disrupt their investments.

For the majority of the first month of the year, much of the conversation has centered around inflation and the coronavirus.

However, the other big focus for investors should be the geopolitical concerns stemming particularly from bubbling tension in Russia and Ukraine.

These concerns provide an ample opportunity to focus on the proverbial Teddy Roosevelt reminder to “speak softly and carry a big stick.” In other words, to ensure there is civil dialogue for peace while ensuring if things escalate a country’s word can be backed up with force.

While the world has become a more peaceful and cooperative place since Teddy Roosevelt’s time, human nature remains unchanged. In this case, the United States is speaking softly, while NATO carries the “big stick” against Russia.

In the past few years, the United States and NATO have been forced to move from soft words to stronger deterrents.

Since the breakup of the USSR, Russia has been looking to force Ukraine into its political alignment and away from NATO by seizing Crimea and moving troops into the east of the country. Meanwhile, the U.S. and allies after having sanctioned Russia are now bringing anti-tank weaponry into the country to act as a deterrent.

The largest supplier of these weapons is Lockheed Martin (LMT), the largest defense contractor in the world.

As a government supplier, many may think that their profits and margin aren’t that high.

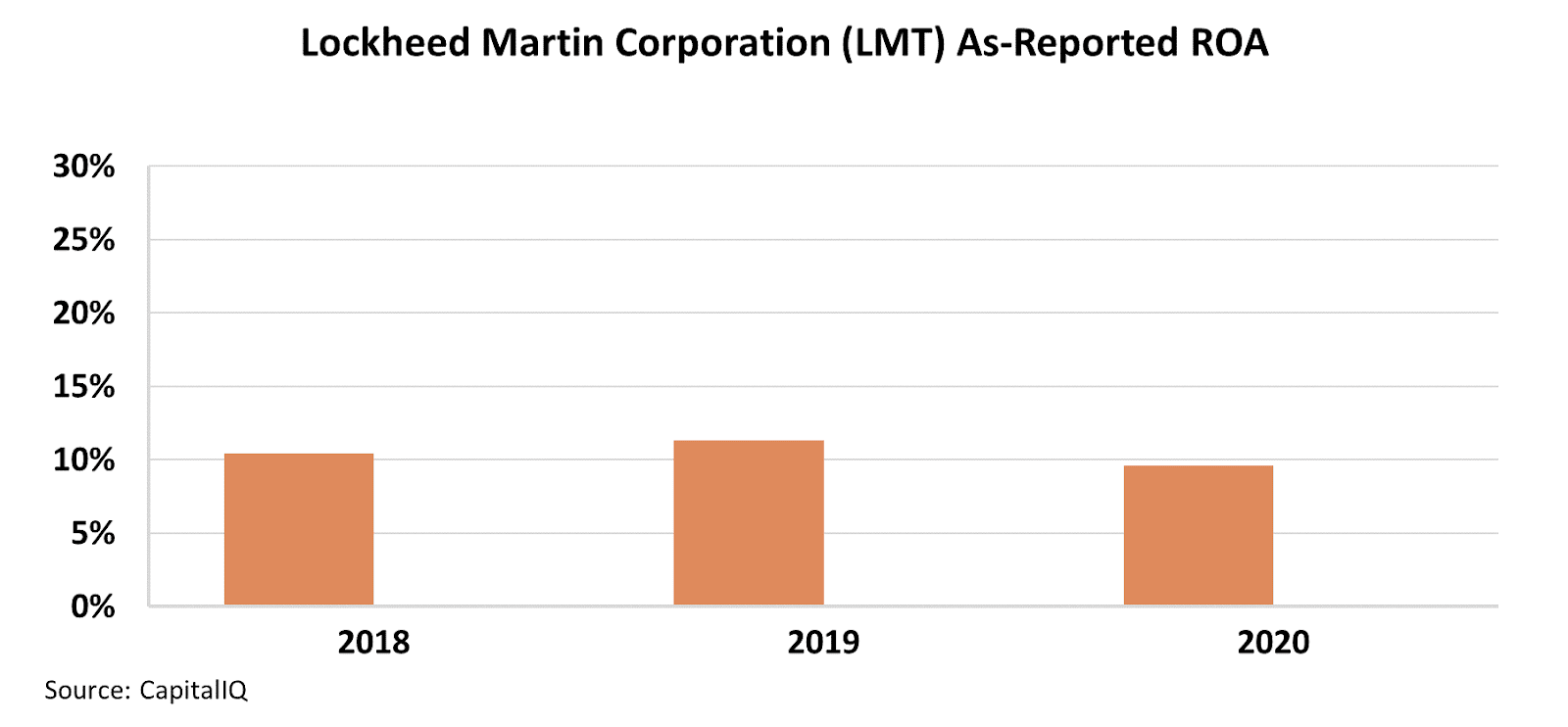

Looking at the as-reported metrics, it would appear that Lockheed Martin has been able to convert a big stick to big returns. Over the past three years, returns have hovered around corporate averages of 10%.

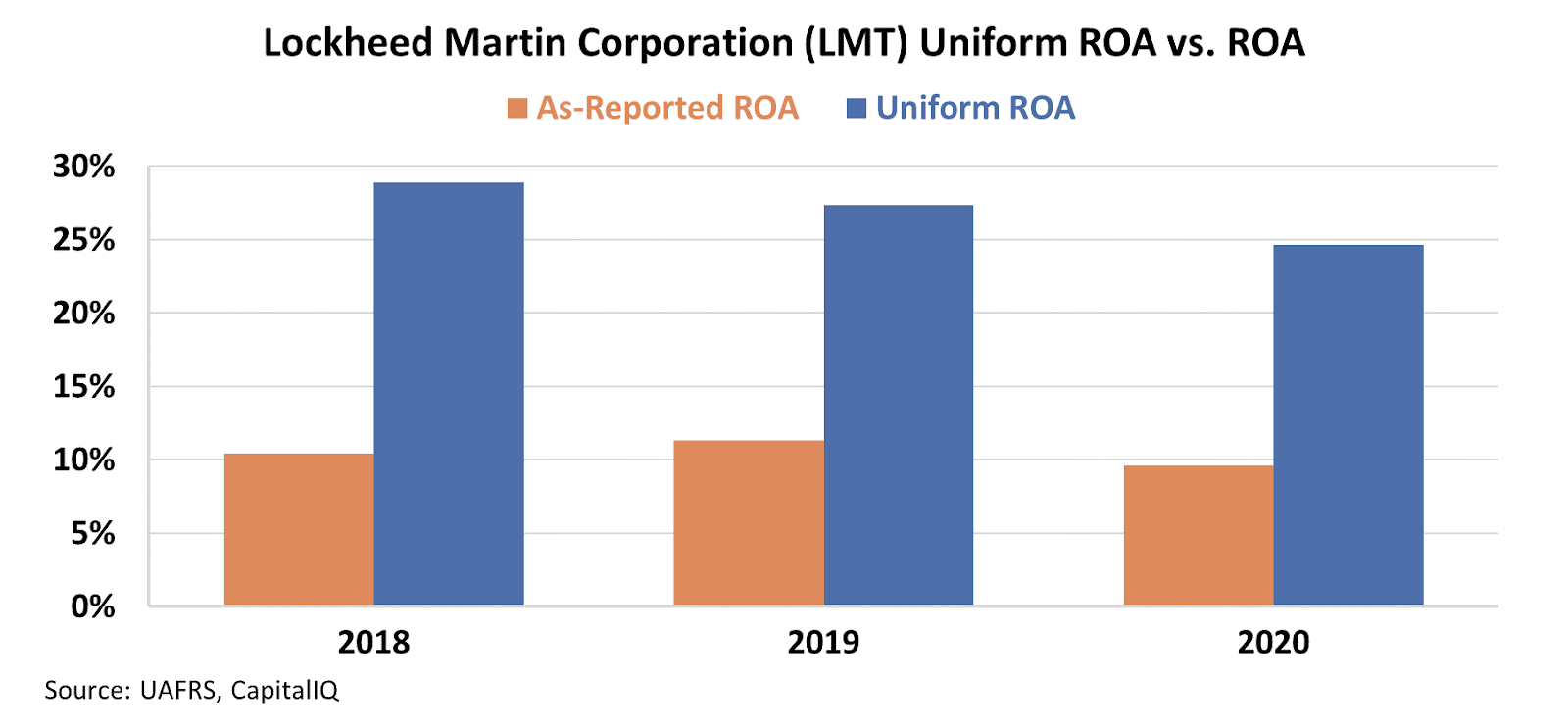

However, a closer look at the business’s real performance tells a much different story. Using Uniform Accounting adjusts for distortions such as goodwill and excess cash which are artificially inflating the assets on the balance sheet.

After resolving these discrepancies, we can see that returns have a very different reality.

Uniform Accounting shows us that LMT does quite well by supplying the defense industry with a ROA two times higher than the as-reported values. Returns have been well above averages, between 25% and 29% the past three years.

As long as conflicts between large entities remain, investments in the companies that build the tools that allow the US to carry a big stick will remain a great investment. Names like Lockheed Martin are well poised to continue to reap high returns in 2022 and beyond as tensions continue to escalate.

In our Conviction Long List, we highlight a plethora of names that are poised to benefit from this macroeconomic trend that the wider investment community hasn’t yet caught onto. If you are interested in reading more, you can click here to subscribe.

SUMMARY and Lockheed Martin Corporation Tearsheet

As the Uniform Accounting tearsheet for Lockheed Martin Corporation (LMT:USA) highlights, the Uniform P/E trades at 16.8x, which is below the global corporate average of 24.0x, but around its own historical P/E of 16.4x.

Low P/Es require low EPS growth to sustain them. In the case of Lockheed Martin, the company has recently shown a 1% Uniform EPS shrinkage.

Wall Street analysts provide stock and valuation recommendations that in general provide very poor guidance or insight. However, Wall Street analysts’ near-term earnings forecasts tend to have relevant information.

We take Wall Street forecasts for GAAP earnings and convert them to Uniform earnings forecasts. When we do this, Lockheed Martin’s Wall Street analyst-driven forecast is a 4% EPS decline in 2021 and 11% EPS growth in 2022.

Based on the current stock market valuations, we can use earnings growth valuation metrics to back into the required growth rate to justify Lockheed Martin’s $373 stock price. These are often referred to as market embedded expectations.

The company is currently being valued as if Uniform earnings were to shrink 2% annually over the next three years. What Wall Street analysts expect for Lockheed Martin’s earnings growth is in line with what the current stock market valuation requires in 2022, but above this requirement in 2023.

Furthermore, the company’s earning power in 2020 is 4x the long-run corporate average. Moreover, cash flows and cash on hand are almost 2x its total obligations, and intrinsic credit risk is 60bps above risk-free rate, signaling low dividend risk.

Lastly, Lockheed Martin’s Uniform earnings growth is below its peer averages. However, the company is trading well below its average peer valuations.

Best regards,

Joel Litman & Rob Spivey

Chief Investment Strategist &

Director of Research

at Valens Research

The Uniform Accounting insights in today’s issue are the same ones that power some of our best stock picks and macro research, which can be found in our FA Alpha Daily newsletters.