Deluxe Crosses Over To Investment Grade, While Equity Markets Have Bearish Expectations

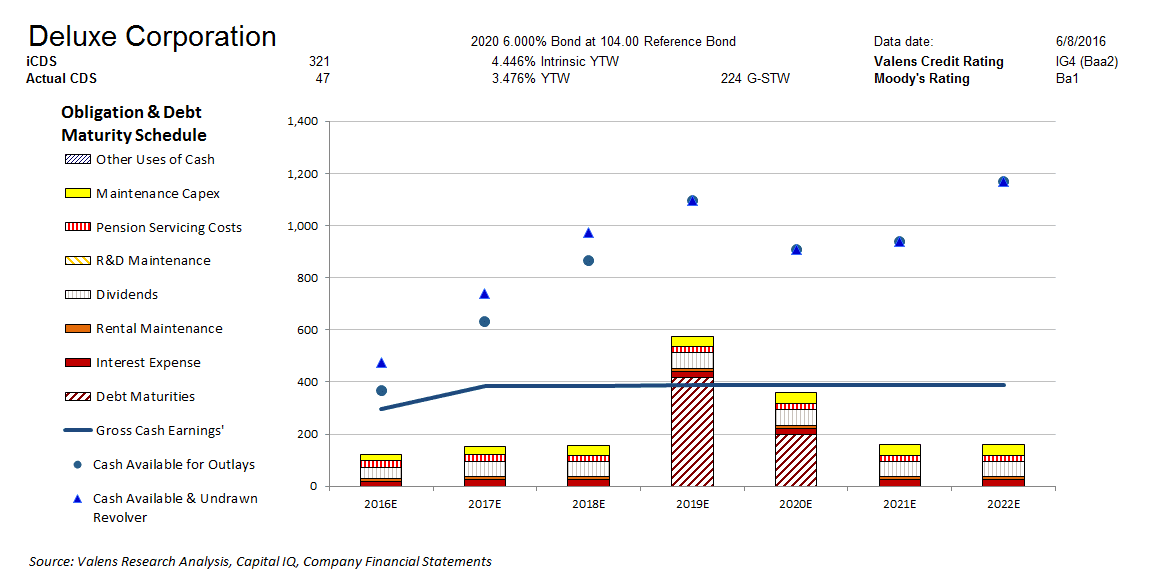

Moody’s is overstating the credit risk of Deluxe Corporation (NYSE:DLX) with its Ba1 rating. Our fundamental analysis highlights a safer credit profile for DLX, whose strong cash flows cover all operating obligations going forward. Moreover, their healthy liquidity profile would allow them to service all obligations including debt maturities through 2022. We therefore rate DLX two notches higher at an IG4 credit rating, or a Baa2 equivalent using Moody’s ratings scale.

Meanwhile, CDS markets are grossly understating credit risk with a CDS of 47bps relative to an Intrinsic CDS of 321bps, while cash bond markets are understating credit risk with a cash bond YTW of 3.476% relative to an Intrinsic YTW of 4.446%. This is justified by their negative net working capital levels and limited asset backing, which drive a nonexistent recovery rate on unsecured debt.

DLX is trading at the high end of historical valuations with a V/E’ of 13.0x. The market is expecting modest Asset’ growth of 3% going forward, with ROA’ materially falling to historically low levels from 45% in 2015 to 33%. Considering consensus estimates for ROA’ to slightly fade, market expectations appear too bearish. As a result, even if the firm experiences fading ROA’ levels, equity downside is limited. That said, there is a possibility for modest equity upside if the company is able to maintain their recent plateau shift to +40% ROA’, or see only modest declines as analysts project.

Click here to read the article in its entirety at Seeking Alpha.