Good Years Ahead With Goodyear’s Strong Cash Profile, While Equity Markets Expect ROA’ Improvement

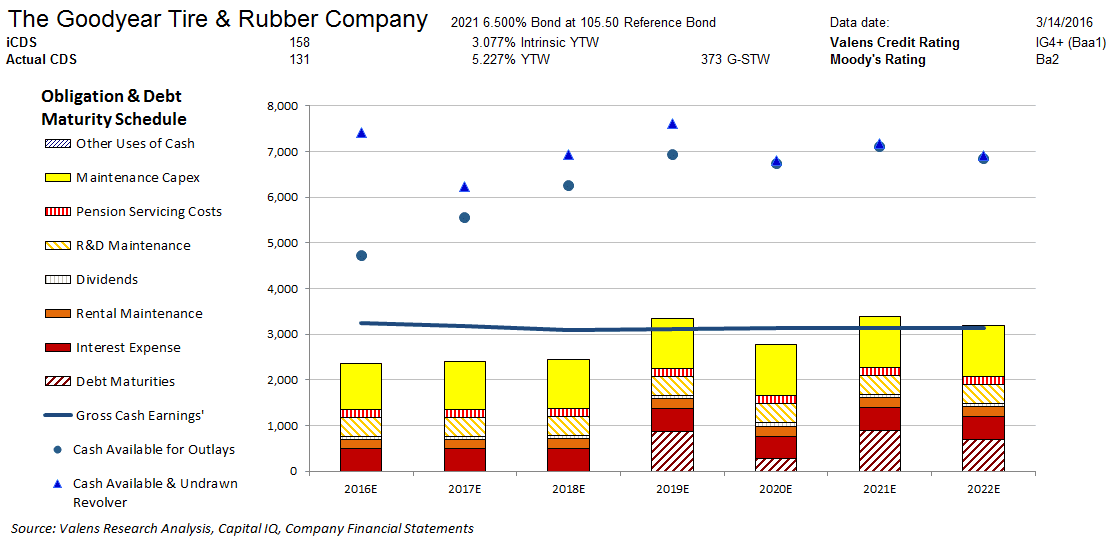

Moody’s is overstating the credit risk of The Goodyear Tire & Rubber Company (NASDAQ:GT) with its Ba2 rating. However, Valens’ fundamental analysis highlights a much safer credit profile for GT. The company’s stable cash flows easily cover all their operating obligations. Moreover, their sizable cash build should allow them to service all obligations including debt maturities in years when their cash flows fall short. Valens therefore rates GT four notches higher at an IG4+ credit rating, or a Baa1 equivalent using Moody’s ratings scale.

Moreover, cash bond markets are materially overstating GT’s credit risk, with a cash bond YTW of 5.227% relative to an Intrinsic YTW of 3.077%.

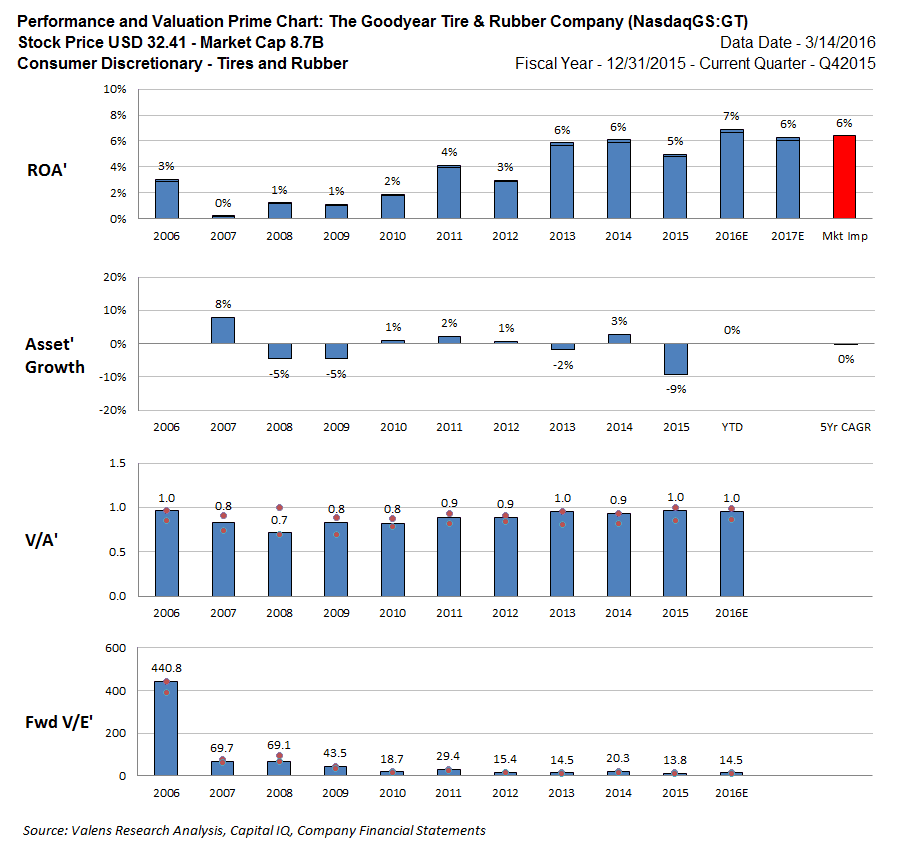

Contrary to credit markets, equity markets are optimistic with GT, trading at modest asset-based valuations with a 1.0x V/A’. Equity markets are expecting ROA’ to improve to 6% levels, which would be a historically high profitability level, with no Asset’ growth going forward. Considering that GT has been able to expand ROA’ to 5% from near-0% levels over the last several years, market expectations appear warranted, though equity upside may be limited. However, equity downside may also be limited absent a material collapse in ROA’, given the reasonable valuations relative to asset levels.

Click here to read the article in its entirety at Seeking Alpha.