Moody’s Fails To Recognize United Rentals’ Investment Grade Profile, While Equity Markets Have Low Expectations

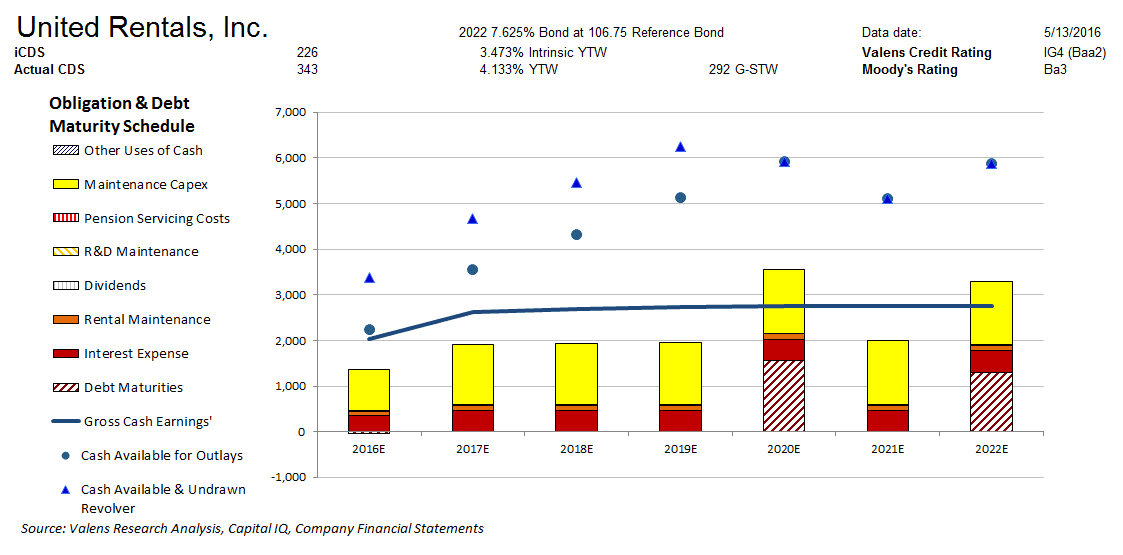

Moody’s is still overstating the credit risk of United Rentals, Inc. (NYSE:URI) with its Ba3 rating. Our fundamental analysis highlights a much safer credit profile for URI, whose strong cash flows cover all operating obligations going forward. Moreover, their projected cash build and cash flows would be sufficient to service all obligations including debt maturities each year even with debt maturities coming due in 2020 and 2022. We therefore rate URI four notches higher at an IG4 credit rating, or a Baa2 equivalent using Moody’s ratings scale.

Moreover, CDS markets are overstating URI’s credit risk with a CDS of 343bps relative to an Intrinsic CDS of 226bps, while cash bond markets are slightly overstating credit risk with a cash bond YTW of 4.133% relative to an Intrinsic YTW of 3.473%.

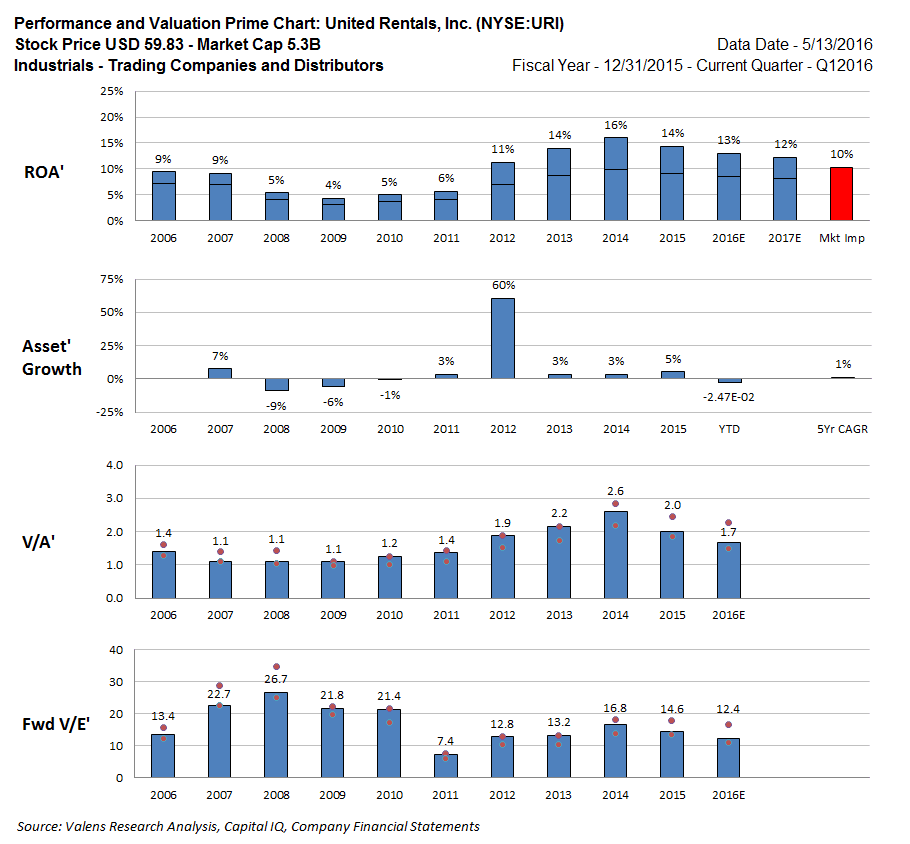

Like credit markets, equity markets are bearish on the name with URI trading at a 1.7x V/A’ and a 12.4x V/E’, both at the lower end of valuations since 2012 (when the firm acquired RSC Holdings and saw ROA’ shift higher). Current market expectations are low, as the market is expecting ROA’ to decrease to 10% from last year’s 14% levels, with modest 1% Asset’ growth going forward. Muted expectations imply that there may be equity upside if the company can sustain ROA’ levels seen since the RSC Holdings acquisition.

Click here to read the article in its entirety at Seeking Alpha.