Achieve ‘PEEK’ Returns With Victrex

Summary:

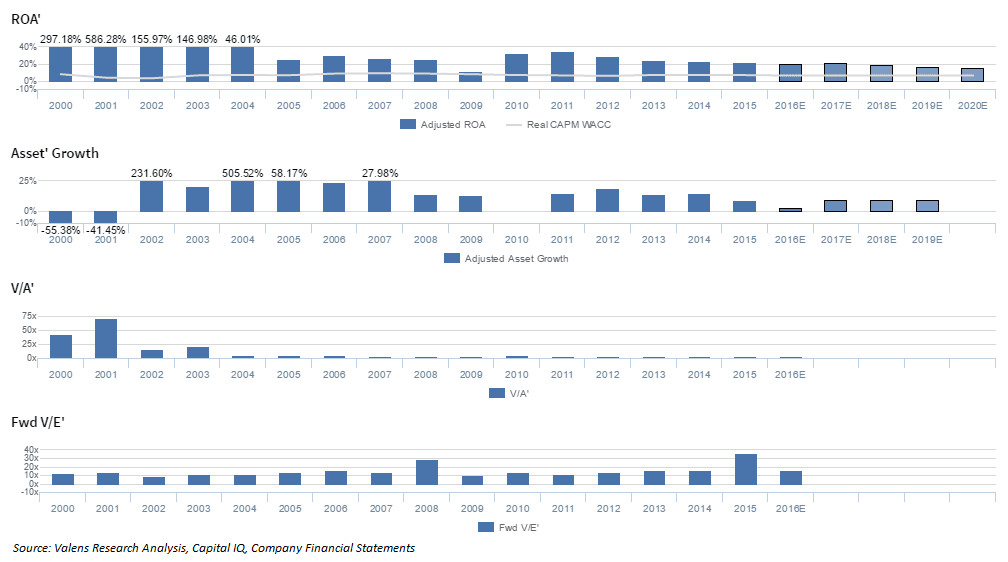

- At £15.51 per share, VCT’s Adjusted ROA of 21% and Adjusted P/B of 3.2x drive an Adjusted P/E of 15.8x, making it an interesting long value idea given its fundamentals.

- Since the expiration of the firm’s manufacturing patent for their key compound PEEK™, the market has significantly undervalued VCT.

- This is due to concerns that the firm’s loss of exclusive manufacturing rights will destroy its competitive advantage and lead to Adjusted ROA compression.

- While, VCT used to be a mere chemical manufacturing company years ago, it has transformed into a solutions provider, manufacturing full products in partnerships with clients.

- This unique focus requires extensive experience and a unique technical skillset, which provides the firm with a distinct competitive advantage and should allow them to drive Adjusted ROA expansion.

At $15.51 per share, Victrex plc has embedded expectations of future performance that are low

Based on a stock price of £15.51, market valuations are pricing in VCT to see Adjusted ROA decline to 15% over the next five years, with a 5-year CAGR (compound annual growth rate) of 9%. To see this in more detail, and have the flexibility to perform your own scenario analysis, click here.

What the market is thinking and why

The market thinks of Victrex only as a PEEK™ manufacturer and distributor, based on their prior performance and business model. While the firm was able to generate substantial returns in the early 2000s, as they benefitted from the exclusive right to manufacture PEEK™, their returns have compressed since losing that right, and the market has begun to have a negative view of the firm’s future. Investors believe that without the exclusive manufacturing right, Victrex will face increasing competition and pricing pressures as other companies enter into the market for PEEK™.

To find out why the market is wrong, and how high LSE:VCT equity can climb, click here to read the article in its entirety at Seeking Alpha.