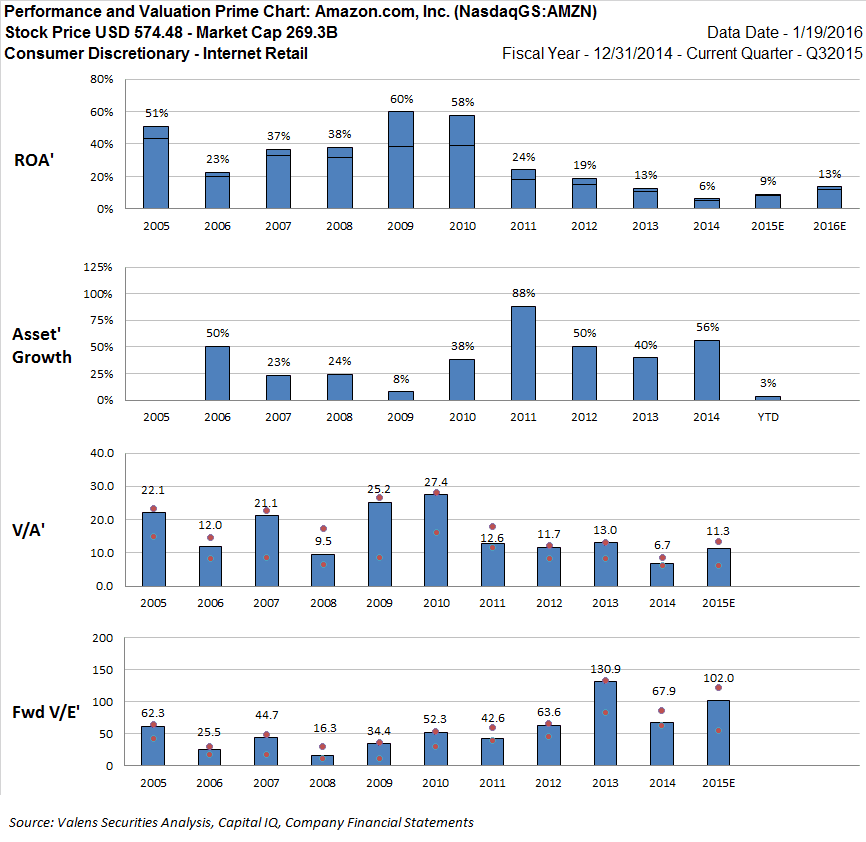

Amazon’s Traditional ROA Severely Miscommunicates Economic Reality

Summary

- After adjusting for distortions in GAAP earnings and assets, AMZN shows an adjusted P/B of 6.7x, significantly lower than the traditional P/B of 25.5x.

- Using adjusted earnings, AMZN’s adjusted ROA is projected to rise from 6% to 9% in 2015 – significantly higher than the traditional 2% ROA reported by most financial databases.

- Due to distortions caused by GAAP, AMZN’s as-reported cash flow from operations is $5.71bn in 2014 when, in economic reality, AMZN’s adjusted operating cash flow was actually at $7.38bn.

For Amazon, there are many failures of GAAP that lead to a low-quality earnings number and an unreliable balance sheet. One major issue is the failure to consistently require capitalization of research and development expenses as well as operating lease expenses. The natural “lumpiness” of the roughly $559mn expenditure in R&D and the $961mn in operating lease expenses results in earnings, margins, cash flow from operations and return on assets that can fluctuate up and down materially from year to year, unlike economic reality.

GAAP requires R&D costs to be either expensed or capitalized from acquisitions as in-process, or written off later. The goodwill and intangibles from acquisitions compound these inconsistencies and distortions when research and development expenditures are involved. For Amazon, goodwill in the $2bn to $3bn range also creates material inconsistencies.

Click here to read the article in its entirety at Seeking Alpha.