Atwood Oceanics Digs Deep With A Crossover Credit Rating, With Equity Markets Having a Similarly Bearish Outlook

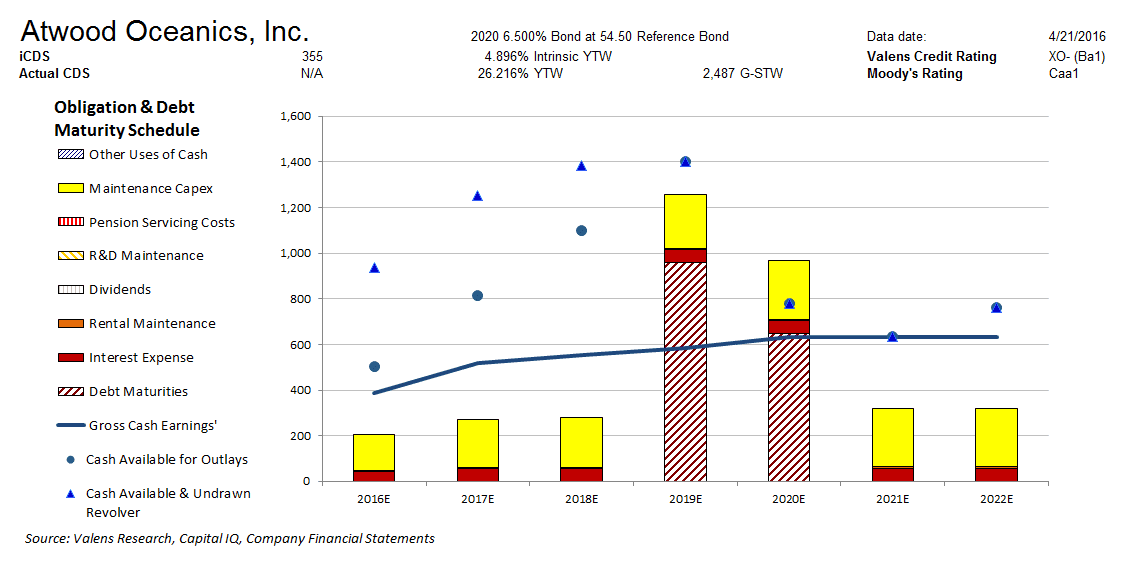

Moody’s is materially overstating the credit risk of Atwood Oceanics, Inc. (NYSE:ATW) with its Caa1 rating. Our fundamental analysis highlights a much safer credit profile for ATW, whose strong cash flows cover all operating obligations going forward. Moreover, their sizable expected cash build would allow them to service their 2019 debt maturity before cash flows and cash on hand fall short of their 2020 debt maturity. We therefore rate ATW six notches higher at an XO- credit rating, or a Ba1 equivalent using Moody’s ratings scale.

Meanwhile, cash bond markets are grossly overstating the firm’s credit risk with a cash bond YTW of 26.216%, relative to an Intrinsic YTW of 4.896% with an Intrinsic CDS of 126bps.

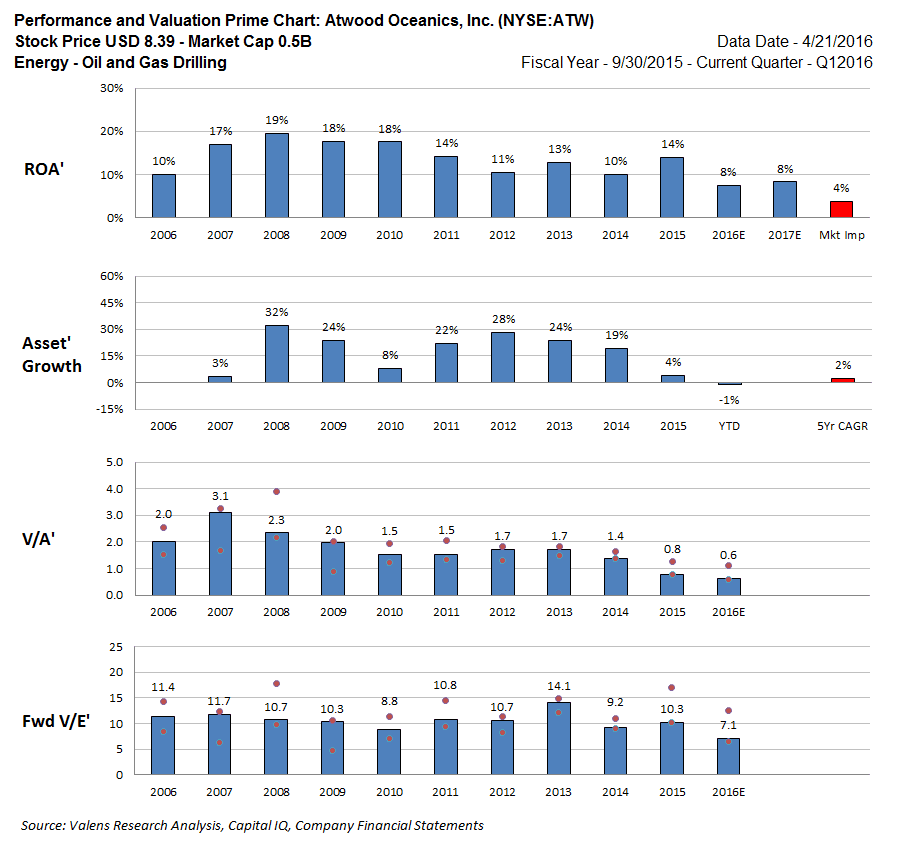

ATW is trading at a 0.6x V/A’ and a 7.1x V/E’, which are historically low valuations. With a similarly bearish outlook, equity markets expect a material ROA’ compression to 4% from 14% levels in 2015, with moderate 2% Asset’ growth going forward. At these levels, asset values begin to offer a floor to valuations, so equity downside is likely limited. Furthermore, a ratings upgrade or a tightening of yield spreads could spur equity upside going forward, with the low market expectations driven by concerns about the firm’s credit.

Click here to read the article in its entirety at Seeking Alpha.