Based on valuation alone, markets may be fully valued, but there are reasons to believe the stock market rally can continue

- While valuations may appear aggressive, they are actually just around average compared to historical valuations in similar inflation and tax environments

- Additionally, after making UAFRS adjustments, markets are not as expensive as as-reported metrics suggest

- Moreover, there are reasons to believe this rally can continue, even though the market is not deeply undervalued

The S&P is not as expensive as it initially appears, when compared against similar tax and inflation environments

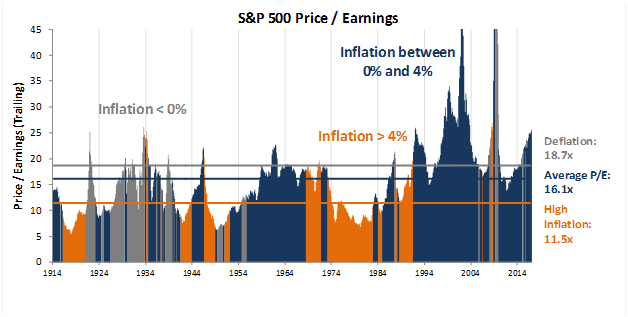

Although the S&P 500’s average trailing price-to-earnings multiple has steadily risen to recent highs of 25.5x, when compared against similar economic environments, this is likely warranted. Historically, the market tends to support different P/E multiples under different inflation and capital gains tax environments. The chart below highlights historical average P/E under different levels of inflation:

The U.S. is currently in a low (but rising) inflation environment, coupled with low dividends and capital gains tax rates relative to historical rates that are likely to persist during this election cycle. Although valuations may look expensive on a nominal basis, the current average trailing earnings multiple of 25.5x is in the middle of market valuations since the 1990s, assuming low inflation and low tax rates (the blue shaded area). Valuations are trading above 12x-15x lows seen following the tech and housing bubbles, but far below 30x+ levels seen during most of the late ‘90s and prior to the Great Recession, implying that while not cheap, markets are likely not overly expensive considering the economic environment.

After making appropriate UAFRS adjustments, it is apparent markets are not overly bullish

UAFRS adjusted ROA and Asset Growth Analysis also indicates that market expectations are justified, with a Forward V/E’ (Adjusted P/E) of 20.2x, a four-year low, and in line with averages under the current inflation and tax environment. At historically average levels, markets are fully valued at worst, with opportunities for further upside.

At current valuations, markets are pricing in expectations for Adjusted ROA (ROA’) to rise to 12% going forward, with expectations for Adjusted Asset growth reaching 6% levels. This is likely warranted considering U.S. corporate profitability had been improving on a cyclical basis over the past 20 years, rising from peaks of 8% to 9% to 10%-11% in 2011-2014. Also, although aggregate ROA’ declined recently due to headwinds in energy, analysts expect profitability to re-engage in 2017, returning to 2011-2014 levels.

Meanwhile, Asset’ growth has been subdued for the past three years, well below historical averages, but is similarly projected by analysts to improve to levels in-line with market expectations, which are for growth still below historical averages.

Considering ROA’ and growth expectations, U.S. markets appear fully valued at worst. Should corporate profitability trends sustain, and should growth accelerate back to levels seen pre-2012, there is further upside potential.

Traditional calculations, using UAFRS metrics, hold similar implications

Robert Shiller’s Cyclically Adjusted Price/Earnings (CAPE) multiple shares similar sentiment to traditional market metrics. S&P 500’s CAPE recently reached 29.3x, surpassing peak 27.6x levels last seen in 2007, before the Great Recession. Shiller himself is quoted as saying “the market is way overpriced” as recently as March 14th.

However, when replacing traditional earnings in the CAPE calculation with UAFRS earnings, markets appear fairly valued. In 2007, UAFRS CAPE reached a high of 35.4x, materially higher than CAPE using as-reported metrics, and after collapsing in 2008, have only returned to cyclically average levels since. This reinforces a more bullish outlook for the markets, suggesting current market expectations are warranted, rather than overly aggressive.

There are reasons to believe that even at current valuations, there could be considerable further upside

At current valuations, not only are markets fully-valued at worst, compared to traditional analysis suggesting overvaluation, but there are also reasons to believe aggregate prices can continue to run to the upside.

Specifically, at current valuations, upside would be warranted if management teams were to ramp investment going forward. Moreover, there are reasons to believe this may be the case, including tailwinds related to improving management confidence, catalysts for increased spending and continued looseness in lending standards.

Although the current “fully-valued” market offers the potential for short-lived dips, considering economic tailwinds to ROA’ and Asset’ growth, longer-term upside continues to be warranted.

This article highlights several segments of Valens Research’s Market Phase Cycle Newsletter. To read further please click here (login required.)

Our Chief Investment Strategist, Joel Litman, chairs the Valens Equities and Credit Research Committees, which are responsible for this article. Professor Litman is a recognized global expert in advanced financial statement analysis, corporate performance, and valuation.