CVS’s Health Has Been Misdiagnosed, While Equity Markets Expect Stable ROA’

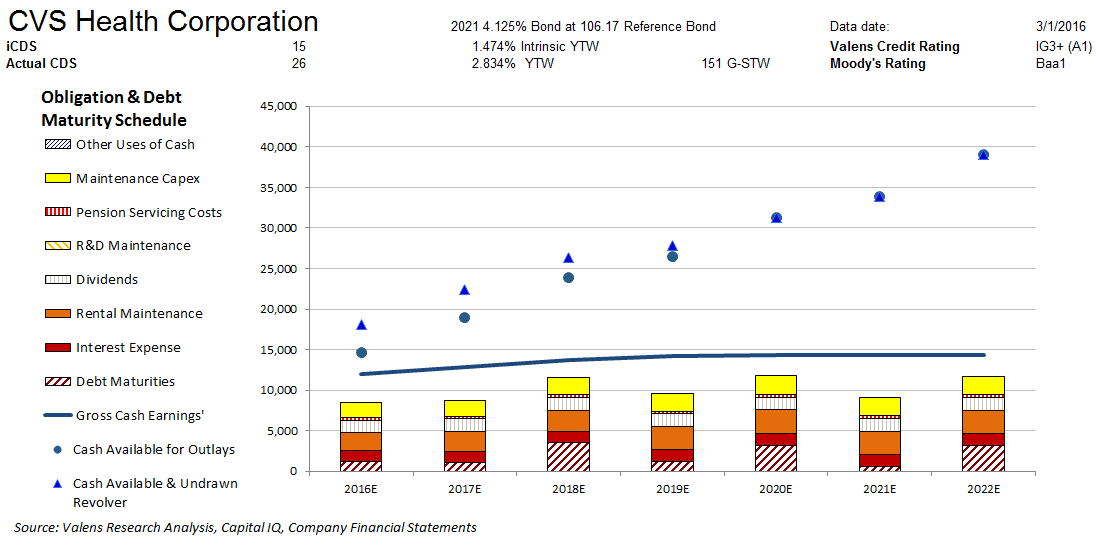

Moody’s is overstating the credit risk of CVS Health Corporation (NYSE:CVS) with its Baa1 rating. However, Valens’ fundamental analysis highlights a much safer credit profile for CVS. The company’s cash flows easily cover all their obligations including debt maturities. Moreover, their sizable cash build should allow them to service all obligations including debt maturities if their cash flows ever fall short. Valens therefore rates CVS three notches higher at an IG3+ credit rating, or an A1 rating using Moody’s ratings scale.

In addition, cash bond markets are overstating CVS’ credit risk, with a cash bond YTW of 2.834% relative to an Intrinsic YTW of only 1.474%. Meanwhile, CDS markets are accurately stating credit risk, with a CDS of 26bps relative to an Intrinsic CDS of 15bps.

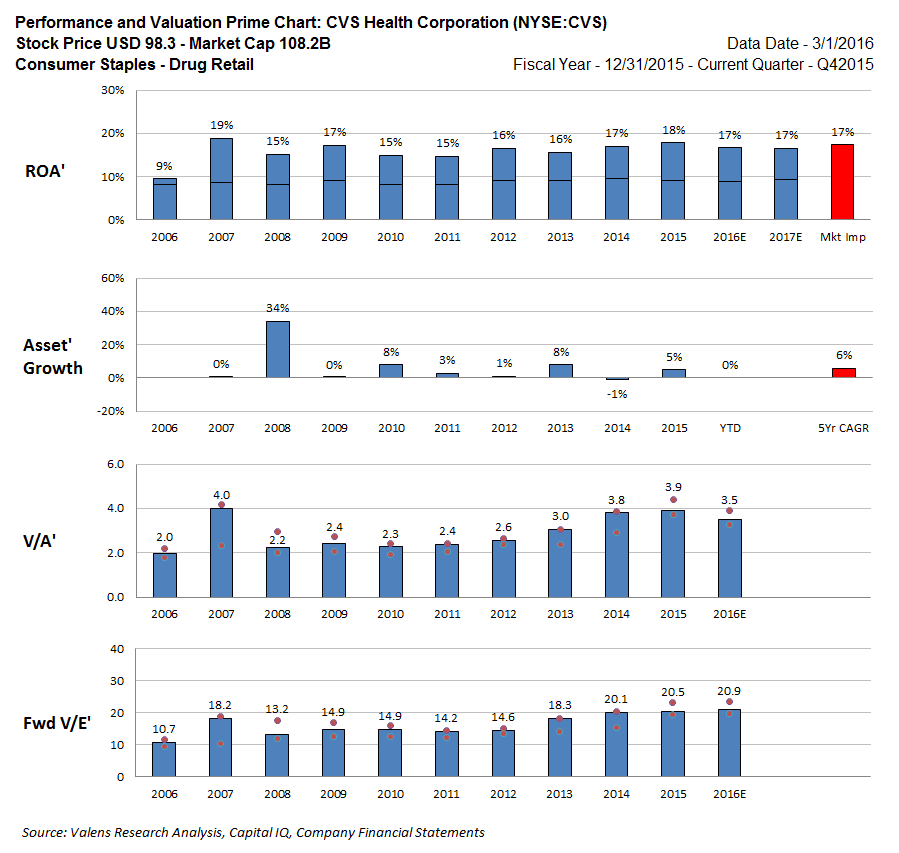

On the other hand, equity markets foresee little change. CVS is trading at high levels relative to history with a 20.9x V/E’ and a 3.5x V/A’. The market expects ROA’ to stay stable at the 16%-18% levels seen during the past few years, with 6% Asset’ growth going forward. Given that the market is pricing in a stable ROA’, the firm is likely fairly valued. However, there could be equity downside if performance begins to fade.

Click here to read the article in its entirety at Seeking Alpha.