Discovering Your Newest Position: DISCA

- DISCA is trading well below corporate averages relative to Forward Adjusted Earnings

- At these levels, markets are already pricing in a near-worst-case for the name

- However, DISCA has fundamentally transformed their business in the last decade

- The company continues to build an economic moat through their low-cost, niche programming and their recent acquisition of Scripps

When there is negative sentiment surrounding an industry, it can be difficult to look through the noise and focus on individual company performance. Within the Communication Services industry, concerns surrounding the cord-cutting movement have clouded investors’ judgment when thinking of individual companies.

While a rising tide indeed lifts all boats, should the inverse be true? While some companies have floundered in the wake of rising costs and lower demand driven by increased streaming competition, others have quietly built a vault of high-quality assets and streamlined operations. DISCA is one of these companies.

Discovery, Inc. (DISCA) is an example of the market failing to recognize operational differences between companies that will lead to vastly different performances facing cord-cutting headwinds. Additionally, the market is pricing in expectations for DISCA to see profitability fall to levels last seen prior to their spin-off of Ascent Media and transition towards pure-play content. As such, should DISCA maintain even the low end of their profitability over the last decade, there is room for material upside. Uniform Accounting helps us see this.

Valuations & Market Expectations

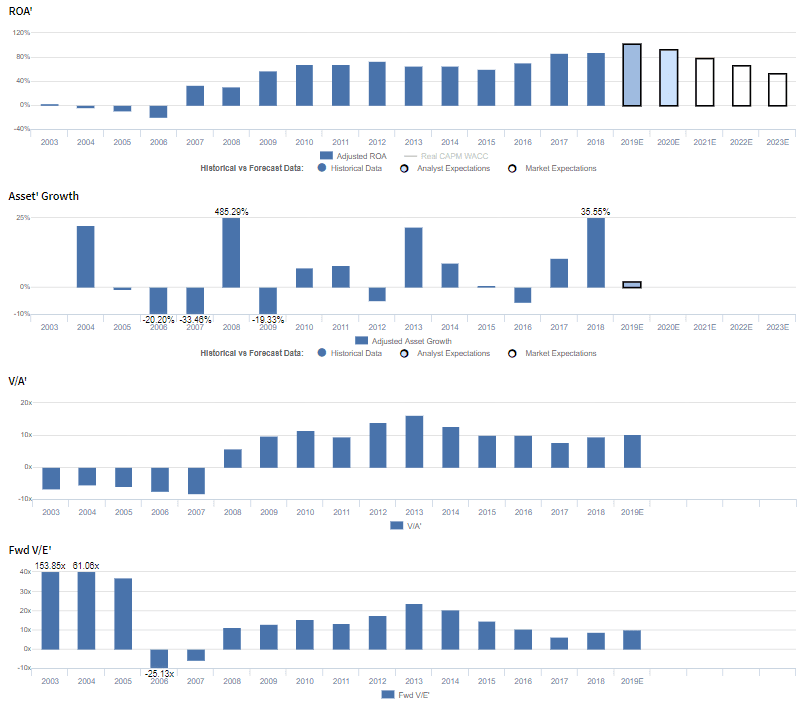

The PVP chart below reflects the real economic performance and valuation measures of Discovery, Inc. (DISCA) after making many major adjustments to the as-reported financials. The rationale behind Uniform Adjusted Financial Reporting Standards (UAFRS) or “Uniform Accounting”, and theory supporting this model can be found here.

The four panels explain the company’s historical corporate performance and valuation levels plus consensus estimates for forecast years as well as what the market is currently pricing in, in terms of expectations for profitability and growth.

The apostrophe after ROA’, Asset’, V/A’, and V/E’ is the symbol for “prime” which means “adjusted” under Uniform Accounting, and these metrics will be referred to as “Uniform” throughout this report. These calculations have been modified with comprehensive adjustments to remove as-reported earnings, asset, liability, and cash flow statement inconsistencies and distortions. To better understand the PVP chart and the following discussion, please refer to our guide here.

DISCA is trading at a 10.2x Uniform P/E (Fwd V/E’), at the low end of historical and peer valuations. DISCA and its peers like Viacom (VIAB) (13.1x Uniform P/E), CBS (CBS) (11.2x), AMC Networks (AMCX) (11.1x), and Tribune (TRCO) (14.2x), have all been punished related to cord cutting concerns. Specifically, as consumers continue to switch from cable subscriptions to online streaming subscriptions, traditional network companies are likely to see reduced demand.

At these levels the market is pricing in expectations for DISCA to have no real organic Uniform Asset (Asset’) growth going forward, toward the lower end of historical Uniform Asset growth levels, with Uniform ROA falling from current 88% levels to just 54% over the next several years.

Just looking at DISCA’s historical trend in Uniform ROA, the company has seen profitability above 50% in each of the last 10 years following their acquisition of assets from Advanced/Newhouse Communications, indicating a fundamental transformation in their business. Moreover, DISCA has seen profitability expand over the last four years, with Uniform ROA rising from 60% in 2015 to peak 88% levels in 2018 due in part to the strengthening of their content portfolio related to their acquisition of Scripps. At current valuations, the market expects the company to see profitability fall to levels associated with a fundamentally different business.

Specifically, DISCA had a transformational change in 2007 when they spun off the legacy Ascent Media portion of their business and began efforts to become a pure-play content provider, a far more profitable and asset efficient business.

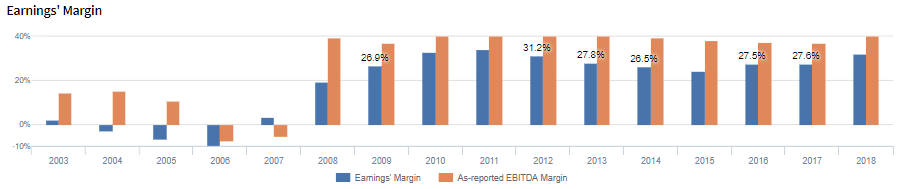

If you look at DISCA’s margins, it is clear their transition away from Ascent Media fundamentally changed their operations. Prior to 2008, Uniform Earnings Margin was volatile, often negative, and never above cost-of-capital levels. However, since shifting their focus entirely to content production and network ownership, Uniform Margins inflected positively and have ranged between 19% and 34% since 2008. Even using as-reported EBITDA margin, this shift is evident.

That said, using as-reported metrics only tell half of the story. Not only has DISCA experience a substantial margin improvement, but they have also seen a huge improvement in asset efficiency. Prior to the Ascent Media spin-off, Uniform Asset Turns were fairly weak, ranging between 0.2x-1.3x. However, over the last 11 years, Uniform Turns have consistently improved to current 2.7x levels, as the firm has focused on streamlining their existing content while integrating new channels like the Scripps portfolio. Using as-reported asset turns, DISCA incorrectly appears to be an inefficient business, with turns never reaching higher than 0.4x over the last 16 years.

At current valuations, markets are pricing in expectations for a reversal in recent trends to both Uniform Earnings Margin and Asset Turns, which appears far too pessimistic when considering the fundamental improvements the business has incorporated into their operations.

Peer Analysis – Valuations Relative to Profitability

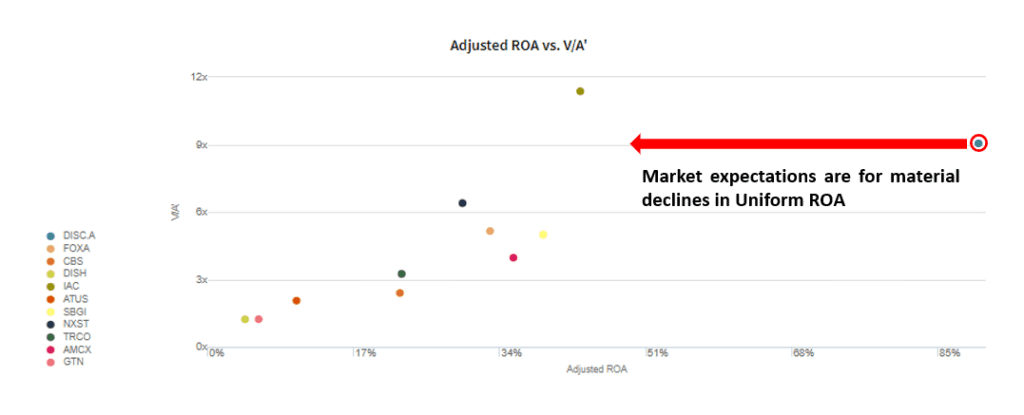

A major benefit of adjusting as-reported financial statements is to clear away accounting distortions to allow for more accurate peer-to-peer comparisons. To this end, we have included a scatter chart below that plots DISCA against its peers based on their Uniform Value-to-Assets (P/B) and Uniform ROA.

Looking across industries, markets, and time, there has been a strong relationship between a company’s Uniform ROA relative to the corporate average (~5%) Uniform ROA, and the multiple the market will pay above the value of the company’s Uniform Asset base, in terms of a Uniform V/A (P/B) multiple. A company that generates a 5% Uniform ROA will tend to trade at a 1.0x Uniform P/B, and a company that generates an 15% Uniform ROA will trade for a 3.0x Uniform P/B, etc.

Relative to its peers, DISCA appears undervalued with its 9.1x Uniform P/B and 88% Uniform ROA. Most of DISCA’s peers, including CBS, AMCX, and TRCO, trade along the expected Uniform ROA and P/B relationship. However, DISCA trades between 1.5x-3.0x higher valuations compared to these names while having 3x-5x higher profitability. The market is pricing in expectations for the company to see profitability decline to levels not seen since their fundamental transformation, which appears unwarranted given the firm’s stable profitability over the last 10 years.

Conclusion

Considering DISCA has fundamentally improved their business since 2008, the market should not be pricing in expectations for profitability to return to pre-2008 levels. Even with cord-cutting an ongoing concern, DISCA has built a portfolio of content designed for sustainable margins and ongoing improvements to efficiency.

In a scenario where DISCA can sustain 50%+ Uniform ROA, and just keep from shrinking their asset base, the firm is likely worth north of $40 per share, 25%+ higher than current prices, and if they are able to continue growing the business, the firm could be worth north of $60 per share, or 2x current prices.