GameStop Levels Up To Investment Grade, While Equity Markets Expect an ROA’ Compression

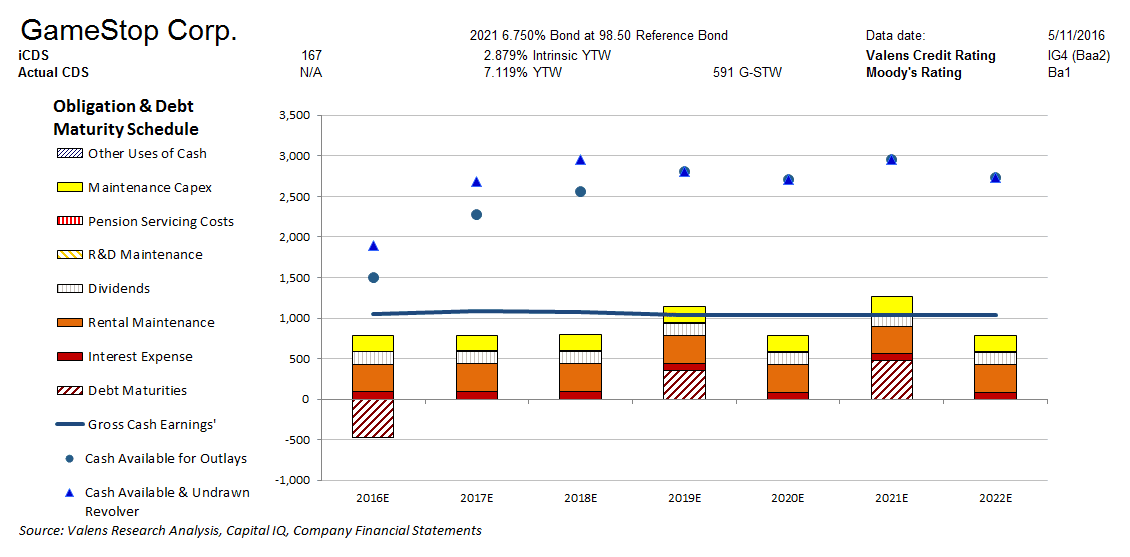

Moody’s is overstating the credit risk of GameStop Corp. (NYSE:GME) with its Ba1 rating. Our fundamental analysis highlights a much safer credit profile for GME, whose strong cash flows cover all operating obligations each year. Moreover, their sizable expected cash build would grant them the ability to meet all obligations including debt maturities through 2022. We therefore rate GME two notches higher at an IG4 credit rating, or a Baa2 equivalent using Moody’s ratings scale.

Moreover, cash bond markets are grossly overstating GME’s fundamental credit risk with a cash bond YTW of 7.119%, relative to an Intrinsic YTW of 2.879% with an Intrinsic CDS of 167bps.

GME is trading at a 12.1x V/E’, which is moderate relative to historical valuations. Equity markets expect an ROA’ compression from last year’s 14% to 10%, with no Asset’ growth going forward. Fundamental headwinds, combined with lagging Asset’ Turns and ever increasing competition, indicate that market expectations appear warranted and that equity is likely fairly valued. However, with Asset’-based valuations near historical lows, equity downside is likely limited as well.

Click here to read the article in its entirety at Seeking Alpha.