Aggregate valuations are back above pre-pandemic highs—that may be as far as they go

With the stock market rebounding to almost pre-pandemic highs, and with massive amounts of new debt in Q1, corporate enterprise values have reached even higher levels than in 2019 or in February before the market dropped.

That may seem like an encouraging signal, but these valuation levels come with fairly bullish market expectations.

Today, we’ll look at the market’s embedded expectations and consider how much room it has left to run.

Investor Essentials Daily:

The Monday Macro Report

Powered by Valens Research

You’ll never find an investing great making blind assumptions.

Famous investors always work backwards, starting by assuming the market is right.

Bill Miller of Legg Mason has a great quote on the matter:

The first duty of the investor… is to figure out what is embedded in the price.

It’s a powerful quote coming from an investor who clearly understood what the market was thinking. During Miller’s time with Legg Mason, he beat the S&P in 15 consecutive years.

His point is simple—a good investor starts by understanding what the market thinks about a company, and only then decides if they have a divergent opinion.

Seth Klarman makes a similar point when describing how his hedge fund, Baupost, has succeeded, saying “If only one word is to be used to describe what Baupost does, that word should be ‘mispricing’.”

One of the best ways to test if a stock is mispriced is by building a discounted cash flow (“DCF”) model.

The point is to forecast the future cash flows of a business using what you know now plus your assumptions about the future, understanding that the current value of the business should be based on those future cash flows.

When you look at valuation metrics like P/E and EV/EBITDA, you’re essentially distilling the outcome of a DCF into a simple ratio.

If you expect a company’s P/E to rise, you’re simply saying you expect its future cash flows to rise.

Unfortunately, most people miss the most important step when building a DCF.

They fail to use that DCF to consider what the market is pricing in before building in their own assumptions and guesses.

That essentially defeats the purpose of a DCF.

There’s another metric we can use to understand what the market expects from a company, which is to compare the company’s value to its asset base.

When companies have excess returns and consistent growth, the market is willing to value them at a premium to the book value of their assets.

While this is typically called a price-to-book (“P/B”) ratio, Valens’ adjusted version of the metric is an adjusted value-to-asset (“V/A’”) which considers the company’s entire enterprise value.

Just as we can value any company using V/A’ we can also value the entire market by aggregating V/A’, and that metric is currently giving us pause.

Aggregate V/A’ is currently at all-time highs, even surpassing levels from late 2019.

Not only have stocks rebounded nearly to pre-pandemic levels, but corporations took on significant debt in the first quarter of 2020.

Tying this into the concept of embedded expectations that both Miller and Klarman consider crucial, we can see that investors have fairly bullish expectations for corporate America.

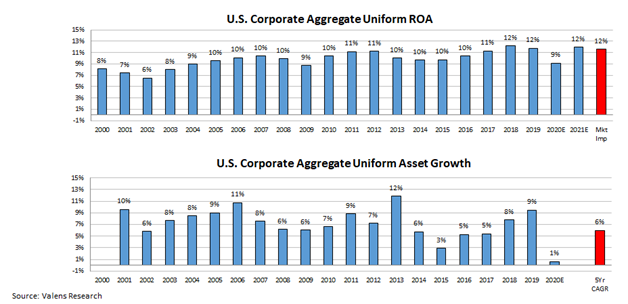

The chart below highlights the expectations for Uniform ROA and asset growth at current V/A’ levels.

Current valuations mean the market expects Uniform ROA to rebound back to all-time highs with asset growth maintaining the same rate from the last five years.

While these are clearly attainable results based on prior performance, they’re still on the bullish side. With that in mind, the market already appears to be pricing in a full recovery, limiting future upside.

Meanwhile, any unforeseen headwinds in the coming months could lead to much more significant downside, implying a potentially unattractive risk/reward profile in the near-term.

Best regards,

Joel Litman & Rob Spivey

Chief Investment Strategist &

Director of Research

at Valens Research