Creditors are treating this company as a one-hit wonder, but Uniform metrics show its success is sustainable, and markets will need to react

The equity markets rewarded this company after a risky bet paid off, sending the stock three times higher over the last three years.

However, even though a look at the company’s TRUE Uniform UAFRS-based analysis shows the company’s credit profile also benefited from its strategy, credit markets remain more pessimistic on its debt.

Below, we show how Uniform Accounting restates financials for a clear credit profile. We also provide the equity tearsheet showing Uniform Accounting-based Performance and Valuation analysis of the company…

Investor Essentials Daily:

Wednesday Credit Insights

Powered by Valens Research

When President Trump came into office in early 2017, many industries were holding their breath about how a new administration would impact the way they did business.

Certainly, many companies reliant on international trade maintained their focus, including the steel industry, the automotive industry, and even the wine and spirits industry.

Another closely monitored industry, oil refining, had its fair share of exposure to Trump’s potential policy decisions.

There’s a movement in the refining industry towards integrating more sustainable biofuels into the refining process. This movement dates back to 2005 when the EPA created the Renewable Fuel Standard (RFS) under the Energy Policy Act.

Under the original act, each ongoing year, the United States needs to replace a larger number of traditional petroleum-based fuel with more renewable and environmentally friendly versions, including biofuel and biomass diesel.

Much the same idea as an emissions tax, companies can produce biofuels to earn a “credit” – which in this case is called a Renewable Identification Number (RIN).

All refiners were required to finish the year with credits representing a percentage of their total output. The RIN quickly became an open marketplace.

Oil refiners who were able to blend more biofuels into their production than necessary were able to sell excess RINs, while companies who chose to underutilize biofuels had to go to the market and pay market price for the credits to fulfill their requirements.

After the 2016 election, there were many unknowns about the future of the EPA and its many programs. One company in particular, CVR Energy (CVI), owned by Carl Icahn, took the opportunity to make a significant bet.

Icahn postulated that under Trump’s administration, the RIN market would flip from a seller’s market to a buyer’s market. As a result, CVI delayed their RIN buying activity for as long as they could. In essence, Icahn was shorting the RIN market.

While the company was forced to buy some RINs towards the end of 2017, Icahn remained patient and bought only the minimum it was allowed to under the 1-year delay the program offers.

In the long run, the bet paid off. Trump’s administration lowered the price small refiners had to pay for RINs, from $0.92 in 2017 to a low of $0.33 in 2018. CVI’s RIN costs dropped from $249 million in 2017 to just $60 million in 2018.

This was huge for the company’s stock, which has tripled since the 2016 election.

While equity holders have celebrated the company’s strategy, creditors have been less quick to reward the company.

Creditors view CVI’s strategy as a short-term positive that may not be sustainable, and are waiting for CVI to get their comeuppance.

Because of that, even as the equity has rallied, the company’s bonds that are only 2 years from maturing still trade with an elevated 6% yield to worst.

But while the market is punishing the company for its savvy move, Uniform Accounting highlights a few reasons to think markets are being too pessimistic.

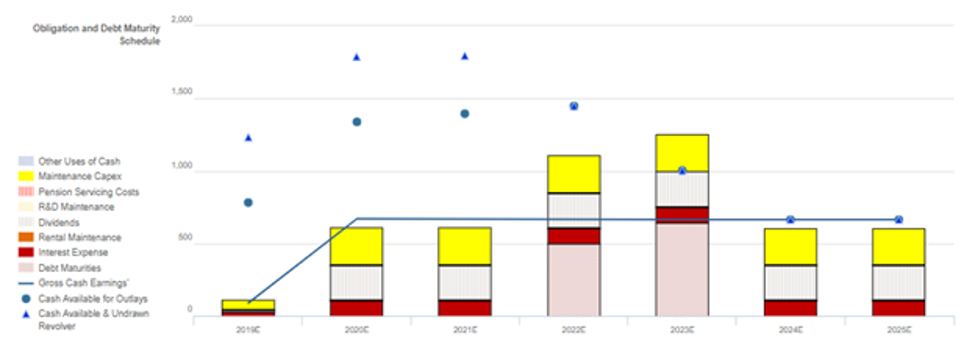

CVI is forecast to have Uniform cash flows exceed operating obligations each year going forward. Even when the company’s 2022 debt obligations referenced above come due, thanks to the company’s significant cash on hand balance, it should have no issues retiring this debt if it doesn’t choose to refinance it.

Also, while the company may have an issue paying down its 2023 debt maturity based on Uniform cash flow and cash on hand levels, the company also has significant asset backing for their debt.

This is likely to enable them to refinance that debt, especially since the 2022 and 2023 bonds are the only material debt the company has.

After the financials are cleaned up, and looking at the company through a proper fundamental lens as opposed to fear of history, it’s clear that CVI shouldn’t be viewed as a fly by night speculator.

The company’s cash flows, obligations, and asset backing mean it is a safer credit than the capital markets are giving it credit for.

Multi-year debt runway, capex flexibility, and a robust recovery rate indicate that cash bond markets are grossly overstating credit risk

Cash bond markets are grossly overstating credit risk with a cash bond YTW of 5.953% relative to an Intrinsic YTW of 3.083% and an Intrinsic CDS of 148bps.

Fundamental analysis highlights that CVI’s cash flows should exceed all operating obligations in each year after 2019.

However, the firm’s cash flows and cash on hand would fall short of servicing all obligations including debt maturities beginning in 2023, when the firm faces a material $645mn debt headwall.

That said, while they will likely need to refinance to avoid a liquidity crunch, the firm has several years to improve operations before this first debt headwall, and they have ample capex flexibility to temporarily cover cash shortfalls.

Furthermore, their robust 200% recovery rate and sizable market capitalization should facilitate access to credit markets to refinance, if necessary.

Incentives Dictate Behavior™ analysis highlights mostly negative signals for CVI’s credit holders.

While management’s compensation framework focuses them on improving all three value drivers, their compensation framework is heavily skewed towards growth, potentially incentivizing management to overleverage the balance sheet and overspend on assets.

Additionally, management members do not hold any CVI equity, indicating they may not be aligned with shareholders for long-term value creation.

Furthermore, CEO Lamp has high change-in-control compensation, indicating that he may influence other members of management to accept or pursue a sale of the company, increasing event risk for creditors.

Earnings Call Forensics™ of the firm’s Q3 2019 earnings call (10/24) highlights that management is confident their EBITDA for the quarter was $235mn.

However, they may lack confidence in their ability to sustain total barrel throughput, and they may be concerned about future hikes in RIN prices.

Furthermore, they may lack confidence in their ability to forecast their effective tax rate, and they may be concerned about the impact of oil pricing on profitability.

CVI’s multi-year debt runway, capex flexibility, and robust recovery rate indicate that cash bond markets are overstating credit risk. As such, a tightening of cash bond market spreads is likely going forward.

SUMMARY and CVR Energy, Inc. Tearsheet

As the Uniform Accounting tearsheet for CVR Energy (CVI) highlights, the company’s Uniform P/E trades at 9x, which is well below both corporate average valuation levels and previous period valuations.

Low P/Es require low, and even negative, EPS growth to sustain them. In the case of CVR Energy, the company has recently seen its Uniform EPS decline, which may be a signal that below-average valuations are justified.

Wall Street analysts provide stock and valuation recommendations that in general provide very poor guidance or insight. However, Wall Street analysts’ near-term earnings forecasts tend to have relevant information.

We take Wall Street forecasts for GAAP earnings and convert them to Uniform earnings forecasts. When we do this, CVR Energy’s Wall Street analyst-driven EPG growth forecast is 37% in 2019. That drops to a 12% growth in earnings in 2020.

Based on current stock market valuations, we can back into the required earnings growth rate that would justify $42 per share. These are often referred to as market embedded expectations. In order to meet the current market valuation levels for CVR Energy, the company would have to have Uniform earnings shrink by 10% each year over the next three years.

Despite a weak year this year, Wall Street analysts’ expectations for CVI’s earnings growth are far above what the current stock market valuation requires.

In addition to CVR Energy’s valuations being low, its Uniform P/E is well below peer averages, while its Uniform EPS growth is significantly higher than peer averages.

Meanwhile, the company’s earnings power is 2x higher than corporate averages, signaling very low risk to its dividend or operations.

To summarize, CVR Energy is a fairly high-profitability company with significant earnings growth potential and very bearish embedded expectations.

Best regards,

Joel Litman & Rob Spivey

Chief Investment Strategist &

Director of Research

at Valens Research