Despite the cord-cutting phenomenon, this broadcasting company is a much safer credit risk than what credit agencies think

Broadcast TV and cable companies have struggled to hold onto customers in recent years as consumers have cut the cord. This has led to declining cash flows and growing concerns about their ability to pay off heavy debt loads.

Today’s company is a broadcast television company seen as a high credit risk by the rating agencies.

Below, we show how Uniform Accounting restates financials for a clear credit profile. We also provide the equity tearsheet showing Uniform Accounting-based Performance and Valuation analysis of the company.

Investor Essentials Daily:

Wednesday Credit Insights

Powered by Valens Research

Cord-cutting has been a steadily building wave in recent years, with over 39 million people ditching cable in 2019 alone. Cable TV appears to be heading down the same declining route as newspapers over the past decade.

Newspapers were once the dominant form of news, before being overtaken by television. Now, these same consumers are moving to digital sources, including online websites or social media platforms like Twitter (TWTR). They are cutting the cord and getting both entertainment and news from specific platforms and custom apps.

One company that is being directly impacted by the trend is Tegna Inc. (TGNA). Tegna was created in 2015 when the Gannett Company (GCI) split up into two publicly traded companies.

At the time, it looked like a smart move to isolate the quality TV broadcasting assets from the company’s declining newspaper assets. Now five years later, it appears the firm was just separating a fast-melting ice cube from a slow melting one. The TV broadcasting assets now appear to be in a secular decline, much like the newspaper division earlier in the decade.

From 2018 to 2019, Tegna’s as-reported cash flow from operations fell from $530 million to $300 million. This certainly appears to be a sign of a company in distress, especially considering the $4 billion of debt on the company’s balance sheet.

Credit rating agencies appear to have taken note, with a BB- high yield credit rating signaling a high risk of default. And yet, the bond markets do not appear as spooked, with the company having just a 3.2% yield on its debt and a 160bps CDS. This begs the question, what are the bond markets seeing in this declining company?

It appears the bond markets are seeing through the recent declines, and viewing Tegna under a similar framework to what Uniform Accounting shows. According to Uniform Accounting, while the company’s operating cash flow did decline slightly last year, it was only from $700 million to $600 million. Tegna’s cash flow is also forecast to bounce back this year, and is much healthier than what credit rating agencies are realizing.

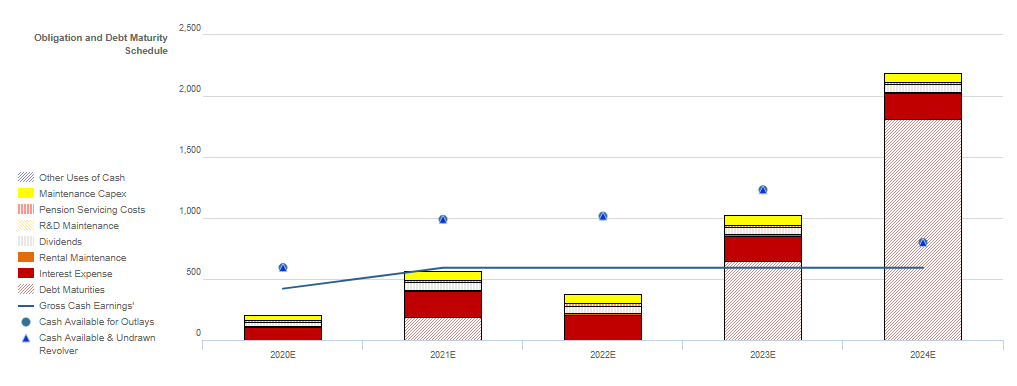

Additionally, most of Tegna’s debt maturities will not yet come due for several years. Cash on hand along with cash flow should be sufficient to meet all obligations until 2024, where the firm will run into a material debt maturity headwall. This gives the company multiple years to improve operations and possibly refinance debt before this occurs.

Ultimately, Uniform Accounting helps investors see through the flawed ratings and paints a more accurate picture of Tegna. After looking at the company’s credit cash flow prime (“CCFP”), it is clear Tegna is much less of a credit risk than rating agencies believe.

The company has better cash flows than as-reported metrics suggest and has a multi-year runway before significant debt maturities become due. While the industry appears to be in decline, it does not spell immediate doom for the firm, as evidenced by Tegna’s significant runway.

Only when looking at the Uniform numbers can we understand the real strength of Tegna’s credit profile.

SUMMARY and Tegna Inc. Tearsheet

As the Uniform Accounting tearsheet for Tegna Inc. (TGNA:USA) highlights, the company trades at a 12.1x Uniform P/E, which is below global corporate average valuation levels, but around its own historical average valuations.

Low P/Es require low EPS growth to sustain them. That said, in the case of Tegna, the company has recently shown an 18% Uniform EPS decline.

Wall Street analysts provide stock and valuation recommendations that in general provide very poor guidance or insight. However, Wall Street analysts’ near-term earnings forecasts tend to have relevant information.

We take Wall Street forecasts for GAAP earnings and convert them to Uniform earnings forecasts. When we do this, Tegna’s Wall Street analyst-driven forecast projects a 28% EPS growth in 2020, before a 15% decline in 2021.

Based on current stock market valuations, we can use earnings growth valuation metrics to back into the required growth rate to justify Tegna’s $12 stock price. These are often referred to as market embedded expectations.

The company can have its Uniform earnings shrink by 7% each year over the next three years and still justify current prices. What Wall Street analysts expect for Tegna’s earnings growth is above what the current stock market valuation requires in 2020, but below its requirement in 2021.

Furthermore, cash flows are below total obligations—including debt maturities, capex maintenance, and dividends. In addition, intrinsic credit risk is 350bps above the risk-free rate, signaling high dividend risk.

To conclude, Tegna’s Uniform earnings growth is above peer averages, and the company is trading in line with average peer valuations.

Best regards,

Joel Litman & Rob Spivey

Chief Investment Strategist &

Director of Research

at Valens Research