Do AI bots even sleep, let alone dream of electronic sheep?

When Philip K. Dick wrote Do Androids Dream of Electronic Sheep his vision of a post-apocalyptic machine-driven world was vastly different from the technology-driven world we see today.

The idea that machine intelligence would come in the form of androids and human-like robots, who rest and move around like humans has proven to be antiquated in a world of machine learning, quantum computing, neural networks, and artificial intelligence driven solutions for problems as simple as getting from one side of a city to the other, to as complex as modelling out game theory in complex online marketplaces.

Instead, it is companies that can deploy solutions that make customers feel like they are interacting with a human that are winning. Solutions that can drive customer engagement, customer endorsement of the offerings, and that can identify new parts of the market for companies the penetrate.

Along with many consulting company brands that are well known, like BCG, Bain, McKinsey, Accenture, and Cognizant, to name a few, one company has been a leader in this space.

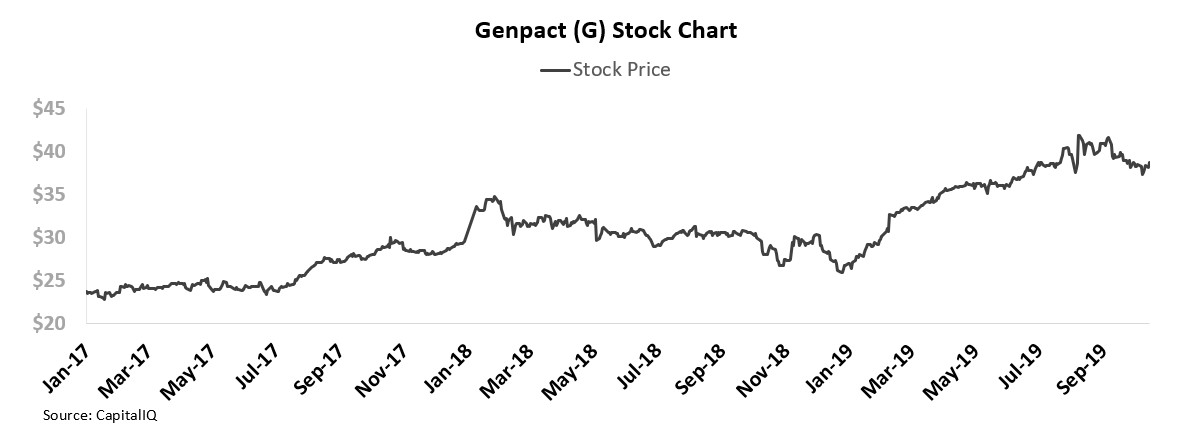

Genpact stock is up 60% since the beginning of 2017 because they are a leader in this space, and this is unlikely to change.

While the stock has already moved significantly, our Uniform Accounting analysis shows market expectations are still not excessive, and there may be more fundamental room for the stock to run. Not only are the fundamentals strong, management is showing confidence about fundamental drivers that may enable them to continue to exceed market expectations.

I’m in Chicago this Friday – Limited Availability Left!

This Friday, I’m presenting at the Driehaus College of Business at DePaul in Chicago. The free event is at 9am, at the campus in the Loop.

I’ll be presenting my popular presentation “Give My Regrets To Wall Street” at 9am.

I’ll be highlighting my thoughts on why Wall Street’s fixation on as-reported earnings and forecast of earnings has led to the dark side of financial statements analysis.

If you are interested in joining us on 10/18, from 9am-10:30am CT, please RSVP.

Seating is filling up rapidly, so let us know if you’re interested, and we’ll be sure to save you a seat. You can reply to this email, or email Andy Aronson (andrew.aronson@valens-research.com).

I look forward to seeing you there.

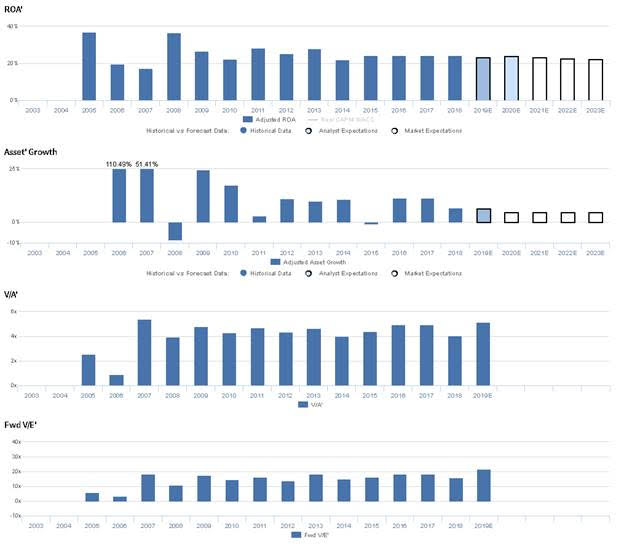

Market expectations are for slight compression in Uniform ROA, but management is confident about margins, revenues, and their market size

G currently trades near corporate averages relative to Uniform Earnings, with a 21.5x Uniform P/E. At these levels, the market is pricing in expectations for Uniform ROA to decline from 24% in 2018 to 22% in 2023, accompanied by 5% Uniform Asset growth going forward.

Meanwhile, analysts have less bearish expectations, projecting Uniform ROA to sustain 24% levels through 2020, accompanied by 6% Uniform Asset growth.

Historically, G has seen robust profitability which has stabilized over time. After falling from 37% in 2005 to 17% in 2007, Uniform ROA returned to 37% in 2008 before stabilizing in the 22%-28% range from 2008-2014. Thereafter, Uniform ROA stabilized further, maintaining 24% levels from 2015-2018. Meanwhile, Uniform Asset growth has been consistent, positive in 11 of the last 13 years, while ranging from -9% to 110%.

Performance Drivers – Sales, Margins, and Turns

Trends in Uniform ROA have been driven by trends in both Uniform Earnings Margin and Uniform Asset Turns. After improving from 13% in 2005 to 18% in 2008, Uniform Margins compressed to 12% in 2014, before improving to and stabilizing at 13% from 2015-2018. Meanwhile, Uniform Turns fell from 2.7x in 2005 to 1.3x in 2007, before rising to 2.1x in 2008 and falling again to 1.5x in 2010. Thereafter, Uniform Turns stabilized at 1.8x-2.0x levels from 2011 to 2018. At current valuations, the market is pricing in expectations for a slight decline in Uniform Turns along with continued stability in Uniform Earnings Margin.

Earnings Call Forensics

Valens’ qualitative analysis of the firm’s Q2 2019 earnings call highlights that management is confident their operating income margin is up 40 basis points year-over-year, and they are confident their business process outsourcing revenues increased 23% year-over-year. Furthermore, they are confident their total addressable market has grown.

However, they are confident they have difficult year-over-year growth comparisons in H2, and they may lack confidence in their ability to deliver attractive profitable growth over the long term. Furthermore, they may lack confidence in their ability to meet the changing needs of their clients, and they may be concerned about the sustainability of earnings improvements across their brands. Moreover, they may be concerned about the growth trajectory of their Global Client BPO, and they may be concerned about the level of competition in the marketplace. Finally, management be concerned about the margin impact of their large deals and about the sustainability of recent cash levels.

UAFRS VS As-Reported.

Uniform Accounting metrics also highlight a significantly different fundamental picture for G than as-reported metrics reflect. As-reported metrics can lead investors to view a company to be dramatically stronger or weaker than real operating fundamentals highlight. Understanding where these distortions occur can help explain why market expectations for the company may be divergent.

As-reported metrics significantly understate G’s profitability. For example, as-reported ROA for G was near 6% levels in 2018, materially lower than Uniform ROA of 24%, making G appear to be a much weaker business than real economic metrics highlight. Moreover, Uniform ROA has consistently been 4x-5x higher than as-reported ROA, distorting investors’ perception of the firm’s profitability ceiling.

Today’s Tearsheet

Today’s tearsheet is for Johnson & Johnson. Johnson & Johnson trades at a discount to market average valuations. At current valuations, the market is pricing in EPS growth significantly below what Johnson & Johnson has been able to deliver historically, or is forecast to deliver going forward.

Regards,

Joel Litman

Chief Investment Strategist