Hiding In Plain Sight

Companies that change their name generally want to walk away from their past. To start over.

Valeant rebranding as Bausch Health after their accounting and specialty pharmacy crisis. Andersen Consulting changed their name to Accenture to shake off Arthur Anderson’s Enron driven collapse. Philip Morris changed their name to Altria to distance themselves from their prior smoking settlements.

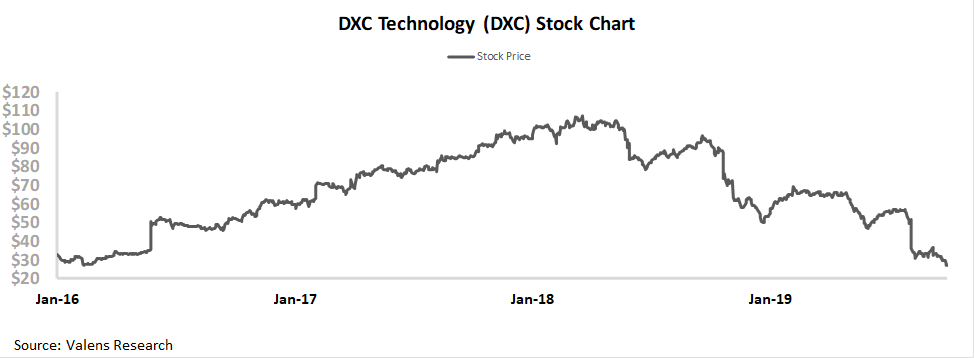

Computer Sciences Corporation didn’t do anything wrong to change their name. But they had been viewed for years as a has-been and an afterthought in the consulting world. Their acquisition of HP’s Enterprise Services business was meant to be a transformative event.

After the acquisition the stock rocketed from $33 before the acquisition was announced in early 2016 to over $100 by early 2018.

The stock has done nothing but fall since, round tripping all the way to $27 as of yesterday’s close.

At current valuations, the market is expecting returns to collapse. But we’re seeing interesting signs that market expectations may have become too pessimistic.

Welcome To Our First Edition

Welcome to our first Valens Research Institutional Daily.

We look forward to you receiving some of our most interesting insights each day from the content we’re generating across our 8,000 Uniform Accounting database.

Each day we’ll highlight one of our embedded expectations analysis that we’re sending to clients that day, sometimes replacing that with other insights from our credit, macro and other research.

With each piece, we’ll include a little bit of extra context on what make that piece so interesting.

Lastly, we’ll be sharing one of our Valens Research equity Tearsheets with you each day. All of our dailies will be available after we email them. Our Tearsheet will only be available the day we publish it, so be sure to check in each day to see which Tearsheet we’re hosting.

Hope you enjoy our daily, and find it insightful.

Now onto the content!

DXC Technology Company – Market expectations are for a material decline in Uniform ROA, but management is confident about their pipeline, cloud business, and free cash flow

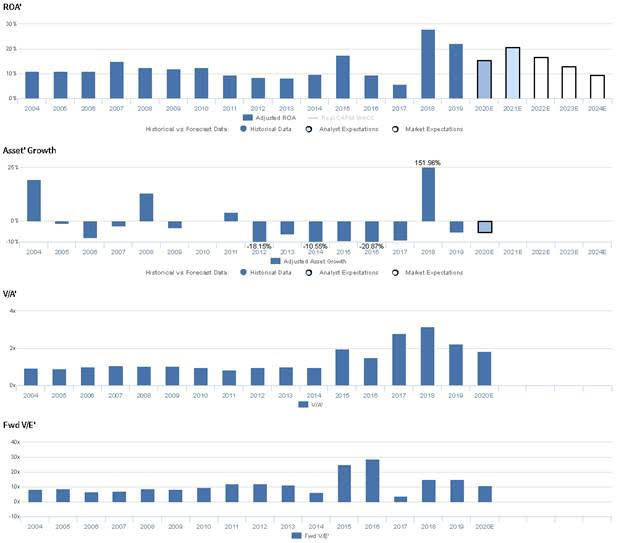

DXC currently trades below historical averages relative to UAFRS-based (Uniform) Earnings, with an 11.0x Uniform P/E. At these levels, the market is pricing in expectations for Uniform ROA to decline from 22% in 2019 to 10% in 2024, accompanied by immaterial Uniform Asset growth going forward.

However, analysts have less bearish expectations, projecting Uniform ROA to only decline to 21% by 2021, accompanied by 5% Uniform Asset shrinkage.

Historically, DXC has seen cyclical profitability. After improving from 11% in 2004 to 15% in 2007, Uniform ROA fell back to 8% in 2013. Thereafter, Uniform ROA rose to 17% in 2015, before sliding to 6% in 2017. Since then, Uniform ROA has soared to 28% in 2018, before contracting to 22% in 2019. Meanwhile, Uniform Asset growth has been volatile, positive in four of the past sixteen years, while ranging from -21% to 152%.

Performance Drivers – Sales, Margins and Turns

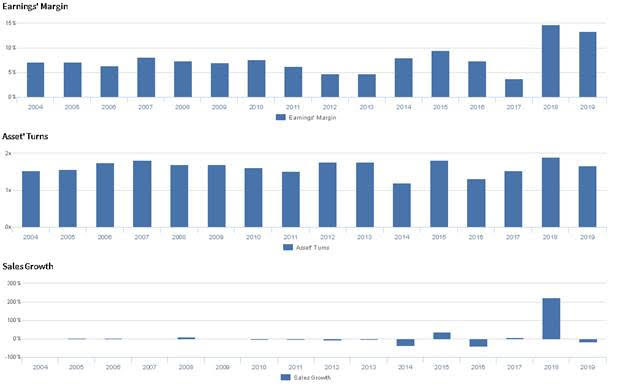

Trends in Uniform ROA have been driven by trends in both Uniform Earnings Margin and Uniform Asset Turns. After improving from 7% in 2004 to 8% in 2007, Uniform Margins fell to 5% levels from 2012-2013, before reaching 10% in 2015. Then, Uniform Margins slid to 4% in 2017, climbed to 15% in 2018, and eroded to 13% in 2019. Meanwhile, Uniform Turns expanded from 1.5x in 2004 to 1.8x in 2007, before fading to 1.2x in 2014. Thereafter, Uniform Turns jumped to a peak of 1.9x in 2018, and have subsequently compressed to 1.7x in 2019. At current valuations, markets are pricing in expectations for material declines in both Uniform Margins and Uniform Turns.

Earnings Call Forensics

Valens’ qualitative analysis of the firm’s Q1 2020 earnings call highlights that management generated an excitement marker when saying they have repurchased $400 million of shares. Furthermore, they are confident their cloud infrastructure business is growing faster than they expected and that their digital pipeline is strong. Moreover, they are confident in their ability to integrate their products into their customers’ existing IT infrastructure and that their adjusted free cash flow was $72 million.

However, management may lack confidence in their ability to sustain recent adjusted EBIT margin improvements, and they may be concerned about further headwinds in their legacy application services. Furthermore, they may be concerned about the sustainability of increased enterprise spend in digital investment and the strength of their relationship with Microsoft. Additionally, management may be concerned about the strength of their traditional business pipeline.

UAFRS VS As-Reported

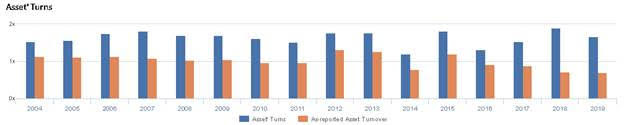

Uniform Accounting metrics also highlight a significantly different fundamental picture for DXC than as-reported metrics reflect. As-reported metrics can lead investors to view a company to be dramatically stronger or weaker than real operating fundamentals highlight. Understanding where these distortions occur can help explain why market expectations for the company may be divergent.

As-reported metrics significantly understate DXC’s asset efficiency, a key driver of profitability. For example, as-reported asset turnover for DXC was 0.7x in 2019, materially lower than Uniform Asset Turns of 1.7x that year, making DXC appear to be a much weaker business than real economic metrics highlight. Moreover, since 2016 as-reported asset turnover has decreased from 0.9x to 0.6x while Uniform Asset Turns have increased from 1.3x to 1.7x over the same time period, directionally distorting the market’s perception of the firm’s historical asset efficiency.

Today’s Tearsheet

Today’s tearsheet is for Microsoft. Microsoft’s UAFRS earnings growth is above average, that is above what the market is expecting for them going forward.

View All