One of our most powerful recession indicators is flashing a surprisingly bullish signal

Most economic models agree we’re in the midst of our first recession in more than a decade.

Compared to most other recessions, this may be one of the fastest we’ve experienced in modern history. That said, certain economic signals point to an equally fast recovery.

Today, we’ll investigate one of our most powerful recession indicators and discuss what the data says about our ability to recover.

Investor Essentials Daily:

The Monday Macro Report

Powered by Valens Research

U.S. GDP shrank by nearly 5% in Q1 2020, even though widespread shutdowns didn’t occur until the last few weeks of March.

That doesn’t bode well for Q2 data, though we won’t know for sure until July or August.

That said, we don’t need to wait that long to know the coronavirus pandemic has already pushed us into a recession.

If the weekly waves of unemployment claims weren’t enough evidence, the fact that entire industries, from travel to movies and restaurants, have effectively shut down across the whole country easily justifies the recession claims.

We don’t disagree, but we do recognize just how unprecedented this recession is.

One large theme in our Monday macroeconomic analysis is that recessions are almost always preceded by a credit crunch.

In the history of modern markets, this might be the first recession to have started without major disruption to lending markets.

At the beginning of March, one of our essays highlighted that corporate lending standards remain lenient, meaning they aren’t tightening. Normally, we see a spike in tightening credit lending standards leading to a recession.

One of the big concerns for this recession is some sections of the economy will have no revenue for several months, which could leave a lot of companies unable to pay their debts.

But so far, this has proved to be less of a concern than you may expect. Entering the pandemic, U.S. corporations had extremely healthy balance sheets.

If you’ve ever read our credit-focused Investor Essentials Daily essays that we post every Wednesday, you may be familiar with our Credit Cash Flow Prime analysis.

For example, on April 29th, we highlighted how as-reported financial metrics understate Iron Mountain’s (IRM) credit risk.

For a corporation, we just compare its Uniform Accounting based cash flows versus its annual obligations to understand its credit position.

We can do this in aggregate to understand how U.S. corporates as a whole are prepared to handle their obligations over the next five years.

Through a combination of historically high cash flows, substantial cash balances, and relatively low debt maturities in the next two years, our economy looks prepared to rebound quickly.

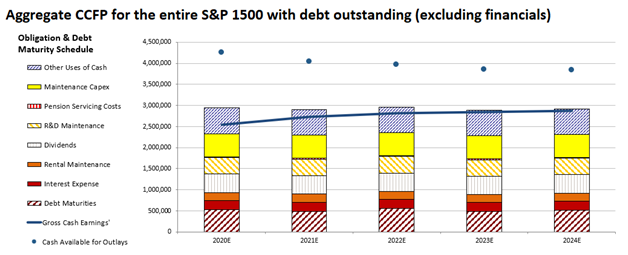

The chart below highlights the aggregate CCFP for the S&P 1500 (S&P 500 plus the S&P 1000) with debt outstanding.

Despite a fairly substantial dip in Uniform earnings in 2020, aggregate earnings are firmly above all obligations except for other uses of cash, which includes activities like share buybacks. Furthermore, these firms have nearly $2 trillion in cash on hand to service any short-term cash flow shortages.

That said, the S&P 1500 includes outliers at the top of the S&P 500 with significant cash stockpiles and limited debt.

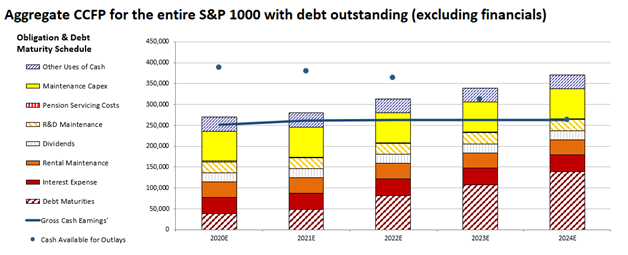

By removing the S&P 500, we can get a more accurate picture of what the average U.S. corporation looks like. Even still, we rarely see such strong forward years in the aggregate CCFP.

The S&P 1000 should have sufficient Uniform earnings to service all obligations except for share buybacks until 2022, at which point some corporations may struggle to fully fund their maintenance capex with just cash flows.

That said, these corporations still have more than $100 billion in cash on hand for any short-term headwinds.

Given the lack of need for liquidity, and the fact that banks still seem willing to lend, these companies will likely be able to service their obligations, even if current shutdowns last for several more weeks or months.

This is a good sign that credit issues shouldn’t lead to a coronavirus shutdown to become a debt driven deep recession. Once we’re able to turn the economy on fully, our rebound could be almost as rapid.

All the best, as always,

Joel Litman & Rob Spivey

Chief Investment Strategist &

Director of Research

at Valens Research