Spin-offs don’t just benefit shareholders, this firm’s spin-off also improved perception of its credit risk helping it navigate the pandemic

Investors often talk about the value of a spin-off for shareholders, yet spin-offs can be just as valuable for bondholders.

Asset-intensive businesses can greatly complicate understanding the borrowing capacity and credit profiles of other asset-light businesses in the same firm. As such, when complex firms execute spin-offs, the true cash flows and creditworthiness of the underlying businesses can be revealed.

This firm shows how its recent spin-off has allowed its asset-light legacy business to benefit during the uncertainties of the coronavirus pandemic, particularly in the eyes of the credit market.

Below, we show how Uniform Accounting restates financials for a clear credit profile.

Investor Essentials Daily:

Wednesday Credit Insights

Powered by Valens Research

Investors often talk about the benefits of a spin-off, especially for conglomerates or large companies with multiple different business lines.

Not only can the smaller, independent companies focus more on their specialized products and services, investors can also value each independently. This often leads to higher individual valuations, as each segment is no longer being held back by the valuation of others, or by the conglomerate discount as some investors just avoid dealing with the complexities of the combined company financials.

For instance, in early April, following its merger with Raytheon, industrial conglomerate United Technologies completed a three-piece spin-off. It retained its aerospace business under the new name Raytheon Technologies, while separating its Carrier HVAC business and Otis elevator business.

United Technologies investors generally saw this move as a positive for each company, as they could better focus on their wildly different businesses and optimize their cost structures and growth strategies.

So far, since the spin-off was finalized in the midst of the coronavirus pandemic, both the aerospace and HVAC businesses have outperformed the industrials sector and the broader market.

The value of spin-offs is frequently discussed in equity circles, but it could often be just as valuable for credit investors.

For instance, when a firm has both an asset-light business and an asset-intensive, potentially highly levered, business combined into one, the borrowing ability of the asset-light business can be restricted more than usual. This structure distorts the underlying firms’ credit profiles.

A classic example of this structure is soft drink giant Coca-Cola.

Its credit profile looks drastically different with and without its bottling businesses, which it has divested, re-consolidated, and re-divested over the past few decades. When included, the bottling businesses’ asset-intensive, low profitability operations can greatly diminish the firm’s credit attractiveness.

Another example of this phenomenon is Wyndham Hotels and Resorts (WH). For a long time, this hotel chain had one of the largest timeshare businesses in the industry attached to it.

Timeshares are asset-intensive businesses with lots of leverage. They need to build out the timeshares themselves before beginning to monetize them.

Due to this, Wyndham’s cost to borrow was always driven by that side of the business, as opposed to its portfolio of hotel and resort brands.

Debt investors would often overlook the borrowing capacity of its incredibly lucrative and scalable franchising model, for timeshares posed a much more glaring risk.

This focus on the riskier, asset-intensive business becomes even more pronounced in the midst of a recession.

Fortunately, Wyndham spun off its two businesses in 2018, and now, the hotel brands survive on their own.

As the coronavirus pandemic greatly threatened the cash flows of the travel industry, Wyndham’s timeshare business, Wyndham Destinations (WYND) saw its credit risk skyrocket, with yield to worst on its bonds increasing from about 3.4% in late February to well over 10% in late March, during the height of the pandemic.

Meanwhile, as markets could focus on the asset-light, high cash flow nature of the hotels and resorts business, the hotel business saw a more moderate increase in its perceived credit risk, with yield to worst rising from similar mid-3% levels to just 8% over the same timeframe.

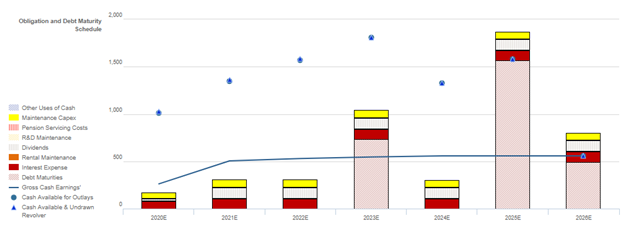

As the Credit Cash Flow Prime for the hotel business shows, it’s no wonder the market was less concerned about this asset-light business. It has significant cash buffers and really no obligations with its limited capex or debt maturities until 2023 or even 2025.

It is clear that the hotel business benefited from separating its asset-intensive business from its remaining hotels and resorts business. As such, it is important to remember that credit investors, and not just equity holders, can benefit from the clarity and options created by a spin-off.

Tightening of Credit Spreads Likely as WH’s Strong Liquidity and Sizable Debt Runway are Overlooked

Credit markets are grossly overstating credit risk with a cash bond YTW of 6.727% relative to an Intrinsic YTW of 4.057% and an Intrinsic CDS of 371bps. Meanwhile, Moody’s is accurately stating WH’s fundamental credit risk, with its speculative Ba1 rating in line with Valens’ XO- (Ba1) rating.

Fundamental analysis highlights that WH’s cash flows should comfortably exceed operating obligations in each year going forward. Additionally, the combination of the firm’s cash flows and substantial cash on hand should be sufficient to service all obligations until 2025, when the firm faces a material $1.6bn debt headwall. As a result, the firm has a sizeable debt runway to improve cash flows to service this shortfall, which is critical, as the firm’s nonexistent recovery rate and moderate market capitalization may make it difficult for it to access credit markets to refinance at favorable rates.

Incentives Dictate Behavior™ analysis highlights mixed signals for credit holders. WH’s compensation framework should drive management to focus on margin expansion and top-line growth, which should lead to Uniform ROA improvement.

In addition, management is not well-compensated in a change-in-control, indicating they may not be incentivized to seek a sale of the company or accept a buyout, reducing event risk.

Additionally, although management members other than CEO Ballotti do not hold material amounts of equity relative to their annual compensation, his sizeable ownership may lead him to influence management to align with shareholder interests for long-term value creation.

That said, management is not penalized for overleveraging the balance sheet or overspending on assets to drive growth, which may reduce cash flows available for servicing obligations.

Earnings Call Forensics™ of the firm’s Q1 2020 earnings call (5/5) highlights that management is confident their asset-light select service franchise business model is primed for long-term growth, that they are looking to increase their pipeline growth to 3%-5% annually, and that they expect license fee revenue from Wyndham Destinations of at least $65mn.

Moreover, they are confident they successfully completed an amendment to their credit agreement and that some emergency travel remained throughout the pandemic.

However, they are also confident every point of RevPAR decline could lead to a $1.5mn decline in EBITDA in this environment, and they may be concerned about hotel closures in China and ongoing weakness in their US hotel operations.

Furthermore, management may lack confidence in their ability to sustain room count growth, increase occupancy rates, and solicit government relief. In addition, they may be concerned about slower new construction growth, the suspension of certain fees, and the sustainability of emergency crew demand. Finally, they may be exaggerating the rate of leisure travel recovery in China.

Operating sustainability, strong liquidity, and a sizeable debt runway indicate credit markets are overstating fundamental credit risk. As such, a tightening of credit spreads is likely going forward.

SUMMARY and Wyndham Hotels & Resorts, Inc. Tearsheet

As the Uniform Accounting tearsheet for Wyndham Hotels & Resorts, Inc. (WH:USA) highlights, the company trades at a 24.2x Uniform P/E, which is above both global corporate average valuation levels and historical average valuations.

High P/Es require high EPS growth to sustain them. That said, in the case of Wyndham, the company has recently shown only 4% Uniform EPS growth.

Wall Street analysts provide stock and valuation recommendations that in general provide very poor guidance or insight. However, Wall Street analysts’ near-term earnings forecasts tend to have relevant information.

We take Wall Street forecasts for GAAP earnings and convert them to Uniform earnings forecasts. When we do this, Wyndham’s Wall Street analyst-driven forecast projects a 49% decline in earnings in 2020, followed by 121% growth in 2021.

Based on current stock market valuations, we can back into the required earnings growth rate that would justify $46 per share. These are often referred to as market embedded expectations.

The company can have Uniform earnings shrink by 3% each year over the next three years and still justify current prices. Wall Street analyst expectations for Wyndham’s earnings growth are below what the current stock market valuation requires in 2020, but above that requirement in 2021.

Meanwhile, the company’s earnings power is 11x corporate averages. Furthermore, total obligations—including debt maturities, maintenance capex, and dividends—are above total cash flows and cash on hand, signaling a low risk to its dividend and its operations.

To summarize, despite trading at high valuations, market expectations for Wyndham are fairly low, suggesting only modest performance is needed to justify current valuations. Even so, the firm has recently struggled to greatly exceed these expectations.

Best regards,

Joel Litman & Rob Spivey

Chief Investment Strategist &

Director of Research

at Valens Research