This automaker is not a fan of the At-Home Revolution, and yet its credit is so bulletproof it’s still a sound investment in the pandemic

The current economic crisis is fundamentally different from the 2008 financial collapse. The U.S. government has launched landmark programs to spur demand, the recession was not caused by credit problems, and it created no bifurcations in sector analysis that haven’t previously existed.

This leads to strange dislocations, simply due to the unique nature of today’s credit environment.

Today’s company has market interest rates that would be far too low in a normal recession, and yet it has even less credit risk than markets account for, unlike its precarious position during the 2008 recession.

Below, we show how Uniform Accounting restates financials for a clear credit profile. We also provide the equity tearsheet showing Uniform Accounting-based Performance and Valuation analysis of the company.

Investor Essentials Daily:

Wednesday Credit Insights

Powered by Valens Research

Economists have needed to throw out the standard playbook during this year’s coronavirus-induced downturn.

Maxims such as “homebuilders get crushed in a recession” or “auto companies struggle during downturns”, have not applied. In the past, recessions have always been driven by a credit crisis, which has not been the catalyst for this recession.

Companies typically struggle during downturns with an inability to pay down debt, causing bankruptcies. This is especially true for consumer-focused companies that see their customers pull back.

However, the pandemic’s unique nature and forced lockdowns have turned conventional wisdom on its head.

One thing this recession hasn’t changed though is that an automaker rarely is going to be immune to a recession. As such, some might look at General Motors (GM) bonds and be perplexed as to why they are trading at low yields of 2.8%.

During the last recession, General Motors posted a staggering $31 billion loss in 2008. It was forced into bankruptcy just one year later, becoming the fourth largest Chapter 11 filing in history.

General Motors sold off a variety of assets and had to receive bailout money from the U.S. government. It emerged from bankruptcy with far less debt on the books and a leaner, more focused operation.

Since then, General Motors has taken a variety of steps to improve its credit structure and build cash liquidity for issues like today. It shed large amounts of debt, discontinued less profitable models and reduced expenses for retired workers and families. Management remembers 2009 all too well and has built the company to survive this.

General Motors is now a more profitable company with a stronger balance sheet. During the coronavirus, even as the company has seen revenues collapse, it has drawn on its credit facility, while refinancing debt in this ultra-low interest rate environment to maintain its liquidity.

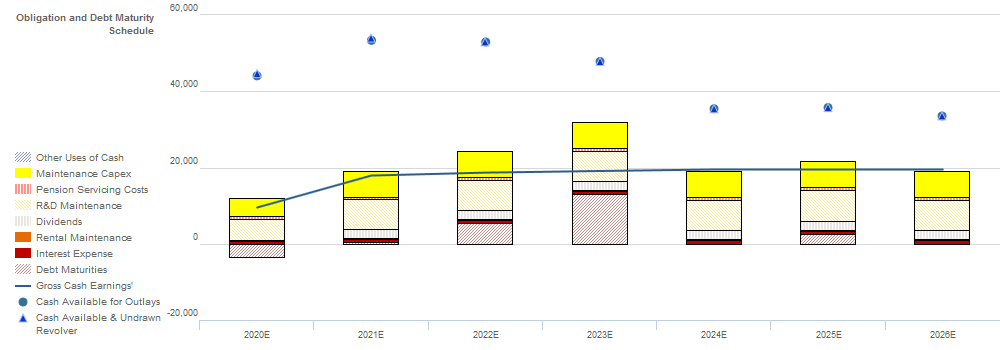

By looking at the Credit Cash Flow Prime (CCFP), we can compare the company’s cash flows to its outstanding obligations, and measure the real risk of default. Thanks to General Motors’ large cash balance and strong cash flow generation, the firm is at little risk of bankruptcy even with the current demand strike.

General Motors’ cash flows and cash on hand is well in excess of all obligations through 2026, including a large $13 billion debt maturity headwall in 2023.

As demonstrated earlier in the crisis, General Motors’ huge market capitalization gives it access to the credit markets to refinance if needed.

Despite the economic issues stemming from coronavirus, General Motors only has a yield of 2.8%. The market is pricing in General Motors for little credit risk, defying typical stereotypes about recessionary impacts on automakers.

However, after looking at the company’s CCFP, it is clear General Motors is even less of a credit risk than the market gives it credit for. Robust cash flows and a sizable cash build indicate the company’s Intrinsic YTW is 1.4%, nearly half of outstanding yields.

Despite its past history of credit troubles during recessions, General Motors has little to no credit risk with a strong balance sheet. Prudent management decisions, as well as a unique recession environment, have left General Motors in a strong position.

Only when looking at the Uniform numbers, can we understand just how good this position is.

Tightening of Credit Spreads Likely as GM’s Strong Cash Flows Continue to be Overlooked

CDS markets are slightly overstating GM’s credit risk with a CDS of 161bps relative to an Intrinsic CDS of 109bps, while cash bond markets are overstating credit risk with a YTW of 2.878% relative to an Intrinsic YTW of 1.428%. Meanwhile, Moody’s is accurately stating GM’s fundamental credit risk, with its Baa3 credit rating one notch below Valens’ IG4 (Baa2) rating.

Fundamental analysis highlights that GM’s cash flows should roughly match operating obligations in each year going forward. Moreover, the combination of the firm’s cash flows and ample cash on hand should be sufficient to cover all obligations including debt maturities through 2026. Furthermore, GM’s large market capitalization should allow access to credit markets to refinance if necessary, despite its lackluster 30% recovery rate.

Incentives Dictate Behavior™ analysis highlights positive signals for investors. GM’s compensation framework focuses management on improving all three value drivers, with a specific focus on margin expansion and asset utilization, which should lead to Uniform ROA expansion and increased cash flows available for servicing obligations.

Moreover, CEO Barra is a material holder of GM’s equity relative to his average annual compensation, indicating she may align other NEOs with shareholders for long-term value creation. Additionally, management members have low change-in-control compensation indicating they are not incentivized to pursue a buyout, and GM’s large market capitalization limits event risk related to a sale of the company.

Earnings Call Forensics™ of the firm’s Q1 2020 earnings call (5/6) highlights that management is confident they had to suspend operations in March and that they expect an annualized loss of 2%-2.5%. Moreover, they may lack confidence in their ability to deliver a profitable electric vehicle business by increasing scale and capacity utilization, meet GM Financial leverage targets, and prevent community spread in their facilities.

In addition, management may be concerned about year-over-year volume and equity income declines in China, the impact of production stoppages, and the pace of China’s economic recovery. They may also be exaggerating their focus on trucks and full-size SUVs, the resiliency of full-size pickup demand, and the potential of their Baojun and Wuling brand partnerships.

Furthermore, management may lack confidence in their ability to ensure a strong supply base and add Shop-Click-Drive features and capabilities. Finally, they may be concerned about pickup segment penetration, dealer inventory levels, and contactless home deliveries.

GM’s strong cash flows, ample cash on hand, and sizable market capitalization indicate credit markets are overstating the firm’s fundamental credit risk. As a result, a tightening of credit spreads is likely going forward.

SUMMARY and General Motors Company Tearsheet

As the Uniform Accounting tearsheet for General Motors Company (GM:USA) highlights, the company trades at a 92.7x Uniform P/E, which is well above global corporate average valuation levels and historical average valuations.

High P/Es require high EPS growth to sustain them. That said, in the case of General Motors, the company has recently shown a 9% Uniform EPS contraction.

Wall Street analysts provide stock and valuation recommendations that in general provide very poor guidance or insight. However, Wall Street analysts’ near-term earnings forecasts tend to have relevant information.

We take Wall Street forecasts for GAAP earnings and convert them to Uniform earnings forecasts. When we do this, General Motors’ Wall Street analyst-driven forecast projects a 150% and 189% EPS contraction in 2020 and 2021, respectively.

Based on current stock market valuations, we can use earnings growth valuation metrics to back into the required growth rate to justify General Motors’ $30.02 stock price. These are often referred to as market embedded expectations.

The company can have Uniform earnings shrink by 8% each year over the next three years and still justify current prices. What Wall Street analysts expect for General Motors’ earnings growth is below what the current stock market valuation requires in 2020, but above in 2021.

Furthermore, total obligations—including debt maturities, maintenance capex, and dividends —are only 1.5x total cash flows, and intrinsic credit risk is 110bps above the risk-free rate, signaling average risk to its dividend and operations.

To conclude, General Motors’ Uniform earnings growth is well below peer averages but the company is trading well above average peer valuations.

Best regards,

Joel Litman & Rob Spivey

Chief Investment Strategist &

Director of Research

at Valens Research