This company’s recurring LBOs have terrified Moody’s. Meanwhile, active CDS credit markets and Uniform analytics show why Moody’s is wrong

This company has repeatedly been taken private and then gone public. Risk averse credit rating agencies are focusing on that risk and refuse to rate the company as investment grade.

However, a look at the company’s TRUE uniform UAFRS-based cash flow analysis shows the company’s situation is not nearly as concerning as Moody’s is concerned about. Also, management isn’t compensated to push for an LBO, reducing that perceived risk.

Below, we show how Uniform Accounting restates financials for a clear credit profile.

We also provide the equity tearsheet showing Uniform Accounting-based Performance and Valuation analysis of the company…

Investor Essentials Daily:

Wednesday Credit Insights

Powered by Valens Research

Creditors and rating agencies are always slow to warm to companies that have previously been private equity owned, even if they’ve been back in the public markets for some time.

A cloud of suspicion tends to hover over the company’s credit situation, as though a mountain of debt is about to be dropped on everyone involved, only making equity holders happy.

It can lead to both the market, and in particular the rating agencies, to be too slow to react to the fundamental realities for a business.

So imagine how credit rating agencies would react to a company who has gone public 3 times, twice after a management led buyout (MBO) or traditional private equity leverage buyout (LBO), in the past 32 years.

HCA, the largest publicly listed hospital company in the US originally went public in 1969. However, the Frist family that founded the company has consistently been savvy about the company’s engagement with the pubic markets.

In 1988, not liking the current environment in the markets, management took the company private in a leveraged buyout before taking it public again in 1992. In less than 15 years, in 2006, the company was taken private again by KKR and Bain, only to be taken public again in 2010 in the midst of the push for the Affordable Care Act.

With that many round trips, Moody’s, spooked about the risk of another LBO, refuses to rate HCA as investment grade. The company’s Moody’s rating is Ba1, in crossover land, on the high yield side.

In reality though, Uniform Accounting highlights that HCA has robust cash flows. The company’s excellent operations and large scale has enabled it to generate best in class Uniform ROA, at 13% levels for 2018.

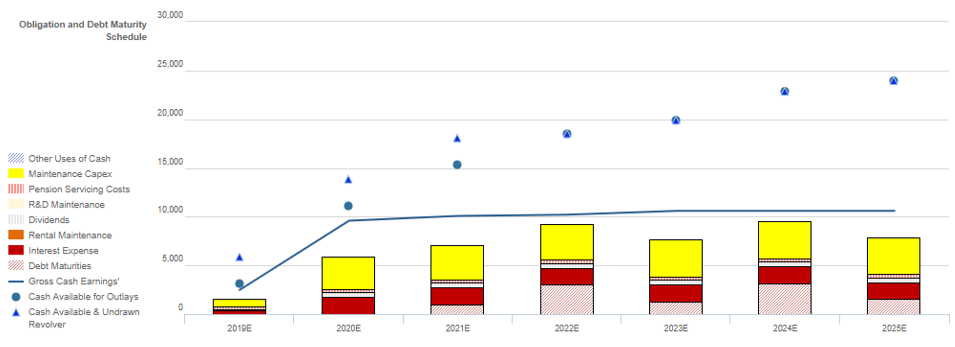

Using Uniform Accounting analytics, we can see the company’s cash flows consistently exceed operating obligations, providing almost a $4bn buffer between operating cash flows and operating obligations.

Even with regular debt maturities in 2021-2025, Uniform Accounting highlights no issues with the company handling its obligations.

Also, management does not appear to be incentivized to support an LBO based on their compensation in a change in control giving further reason to think Moody’s is over-reacting.

After the financials are cleaned up, and looking at the company through a proper fundamental lens as opposed to fear of history, it’s clear HCA should be an investment-grade company. That is why it is rated an IG4 Valens Credit Rating, equivalent to a Baa2 rating. If Moody’s also looked at the real cash flows they’d realize how safe the company is.

Robust cash flows, sizable expected cash build, and significant market capitalization indicate that ratings agencies and cash bond markets are overstating risk

CDS markets are accurately stating credit risk with a CDS of 75bps relative to an Intrinsic CDS of 83bps, while cash bond markets are slightly overstating credit risk with a cash bond YTW of 3.166% relative to an Intrinsic YTW of 2.466%. Meanwhile, Moody’s is overstating HCA’s fundamental credit risk with its Ba1 rating two notches lower than Valens’ IG4 (Baa2) rating.

Fundamental analysis highlights that HCA’s cash flows would exceed operating obligations in each year going forward. Moreover, the combination of the firm’s cash flows and expected cash build would be sufficient to service all obligations through 2025, including consistent annual debt maturities of $1bn+. In addition, if necessary, HCA’s substantial $41bn market capitalization should facilitate access to credit markets to refinance, even with a neutral 60% recovery rate on unsecured debt.

Incentives Dictate Behavior™ analysis highlights mostly positive signals for credit holders. HCA’s compensation framework should drive management to focus on top-line growth and margin expansion, but it does not punish management for overspending on assets or overleveraging the balance sheet to drive growth. However, management members are significant holders of HCA equity, indicating that they are likely well-aligned with shareholders for long-term value creation. In addition, they are not well-compensated in a change in control, suggesting they may not be incentivized to accept a takeover or pursue a buyout, limiting event risk.

Earnings Call Forensics™ of the firm’s Q3 2019 earnings call (10/29) highlights that management may lack confidence in their ability to sustain recent revenue improvements, and they may be concerned about upcoming healthcare legislation impacting profitability. Furthermore, they may lack confidence in their ability to meet their elective procedures guidance.

Robust cash flows, sizable expected cash build, and significant market capitalization indicate that cash bond markets and ratings agencies are overstating HCA’s fundamental credit risk. As such, a tightening of cash bond market spreads and a ratings improvement are likely going forward.

SUMMARY and HCA Healthcare, Inc. Tearsheet

As the Uniform Accounting tearsheet for HCA Healthcare (HCA) highlights, the HCA Uniform P/E trades at 16x, well below corporate average valuation levels and is in line with previous period valuations.

Low P/Es require low, and even negative, EPS growth to sustain them. In the case of HCA, the company has recently shown an 11% Uniform EPS growth.

Wall Street analysts provide stock and valuation recommendations that, in general, provide very poor guidance or insight. However, Wall Street analysts’ near-term earnings forecasts tend to have relevant information.

We take Wall Street forecasts for GAAP earnings and convert them to Uniform earnings forecasts. When we do this, HCA’s Wall Street analyst-driven forecast is a historically high growth of 35% into 2019. That drops to an 11% growth in earnings in the succeeding year.

Based on current stock market valuations, we can back into the required earnings growth rate that would justify $143 per share. These are often referred to as market embedded expectations. In order to meet the current market valuation levels of HCA, the company would have to have Uniform earnings shrink by 2% each year over the next three years.

What Wall Street analysts expect for HCA’s earnings growth falls far above what the current stock market valuation requires.

To conclude, HCA’s Uniform earnings growth is above peer averages in 2020. Also, the company is trading at well below average peer valuations.

The company has an average earning power, based on its Uniform return on assets calculation. Together, this signals moderate cash flow risk to the current dividend level in the future.

Best regards,

Joel Litman & Rob Spivey

Chief Investment Strategist &

Director of Research

at Valens Research