This key sentiment indicator flashed negative in the first quarter, pointing to a key investment trend for Q2 and beyond

Management confidence peaked right when the economy did in February. March and April brought higher levels of uncertainty from management teams.

That said, this isn’t necessarily a signal that the worst is yet to come. It’ll be important to monitor management confidence over the next several months to understand when corporate investments and earnings are likely to pick back up.

Today, we’ll take a look at why management confidence plummeted over the last two months, and what that might mean for Q2 earnings.

Investor Essentials Daily:

The Monday Macro Report

Powered by Valens Research

In our April 27th Investor Essentials Daily, we already began the conversation around management confidence and the ongoing pandemic.

Coronavirus disrupted the longest tenured bull market in our lifetime and officially sent us into a recession as of February according to the National Bureau of Economic Research.

Unfortunately, coronavirus cut the bull market off just as it was poised to keep accelerating.

You’ve likely heard the expression “bull markets don’t die of old age.” This one was no different.

After a historic year of profitability and growth in 2018, U.S. corporations followed up with a comparable performance in 2019.

With two years of strong momentum pushing their sails, management teams were carrying great momentum into 2020.

As our April essay highlighted, our Earnings Call Forensics analysis highlights that management sentiment was improving through the end of 2019 and through the first two months of 2020.

This was a signal to us that, without coronavirus, management teams would have been investing heavily in growth through Q1 and Q2, setting up and extending our bull market.

Even after we saw a rapid decline in confidence in March, management’s pre-pandemic confidence signaled that companies would likely start investing as conditions improved.

Since then, we’ve seen management teams continue expressing more uncertainty and less confidence.

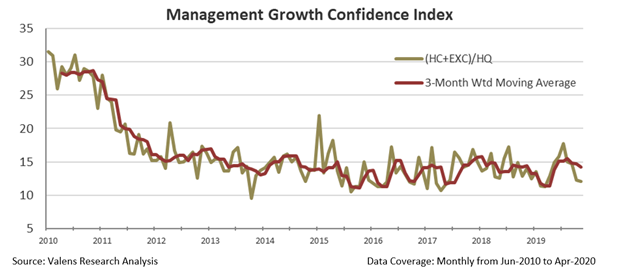

The chart below highlights that management’s confidence ticked even lower in April, which could raise longer-term concerns for the economy.

That said, despite sustained management uncertainty, we expect that in the current environment, this signal on management confidence may be less of a leading indicator than a concurrent indicator.

Management teams are showing concerns because there is rampant uncertainty right now. No one actually knows what will happen in a month.

In March, the first cities began announcing their shutdowns. Confirmed cases kept accelerating through April while there were no clear timetables for a return to normalcy.

We saw this sentiment reflected in management earnings calls in real-time. March and April management growth confidence levels indicated higher uncertainty.

If that’s when most management teams were uncertain, then it makes sense that we’d see lower levels of investment and weaker earnings over the next quarter.

As we wrote in a Forbes article late last month, Q2 earnings are likely going to be worse than most analysts expect.

That does not mean we’re heading for long-term economic issues.

Rather, while management teams are reporting their Q2 earnings, it will be more important than ever to pay attention to our Earnings Call Forensics to understand how management actually feels about the future.

If we start seeing management confidence rise over the next few months, that’s a good sign that the overall impact of the pandemic will be transitory. If the opposite happens, we may need to push off when we expect things to start improving.

We will continue monitoring our Management Growth Confidence Index for telling signals of what’s to come.

Best regards,

Joel Litman & Rob Spivey

Chief Investment Strategist &

Director of Research

at Valens Research