What sharks and Russians have in common

A scary report emerged from Washington DC in 2018. It shed light on a concern that many in the national security apparatus have been aware of for decades.

The Russian state is actively trying to spy, potentially sabotage, and in general get close to the underwater cables that connect the US to the rest of the world.

Using mini submarines, the Russian Navy’s Directorate of Deep Sea Research (GUGI) is reported to potentially be tapping the cables to get a window into the information being transmitted. They even may be planning on cutting cables to disrupt communication.

Thousands of terabits of data flow each second through underwater cables each second under the Atlantic, Pacific, Indian ocean, and every other major body of water in the world on a daily basis.

This includes top secret government data, and data for the world’s militaries, financial transaction information, adorable cat memes, and any other traffic you could think of.

While many people talk about the potential for a modern military like the US to be disrupted by satellite attacks that would knock out communication, in reality, knocking out these high volume cables would be a far faster way to create chaos in a conflict.

While the cables in the Atlantic connecting the US to Europe number in the hundreds, one event in 2013 in Egypt shows the potential impact of sabotage of these cables.

In 2013, several men were apprehended in the Mediterranean after they had intentionally cut one of the fiber optic cables that transmitted data from Europe into Egypt and onto the Middle East and Asia. This one attack reduced internet speeds in Egypt by 60%.

Governments and internet providers are aware of these issues and are actively protecting and repairing cables. However they may not be able to defend us against an even bigger threat to the internet and undersea cables.

Sharks.

Literally, sharks are attacking fiber optic cables.

They are attacking our communication infrastructure globally. There have been attacks reported in the Atlantic, for the cables connecting the US to Europe. Attacks off the coast of Japan. Multiple attacks in Southeast Asia have dramatically impacted internet access at times for the ASEAN region.

Unlike the Russians, the sharks do not appear to have ill intentions (that we know of). They may just mistake the electromagnetic waves from the cables for the same bioelectric fields that some can detect to identify where there are schools of fish. But even so, they may be doing even more to negatively impact global communications.

Any company that can handle the breakdowns that can occur when these attacks happen is essential to global communication, and is likely to earn premium returns.

GTT is one of those companies. Through both organic growth and acquisitions they have grown into one of the most respected Tier 1 IP providers globally. This means they are one of the most trusted providers of the backbone of the internet, sometimes called backhaul services.

When a person on the AT&T network in the US has data that they need to send to someone on the Vodafone network in the UK, a company needs to provide the connection between those two networks. This type of solution is over a third of what GTT does, along with providing other solutions such as wide area network solutions.

When a person on the AT&T network in the US has data that they need to send to someone on the Vodafone network in the UK, a company needs to provide the connection between those two networks. This type of solution is over a third of what GTT does, along with providing other solutions such as wide area network solutions.

We’re Relaunching Our Portfolio Audit Review Offering – And Making A Special Offer

For our institutional clients, we don’t just provide access to our Valens Research app. We also do bespoke research. We produce one-off deep-dive company analyses using all our tools, including Uniform Accounting, credit work, and our management compensation and earnings call analysis. We monitor their portfolios for potential Uniform Accounting signals to alert them. We provide custom datasets for quantitative analysis, and provide aggregate analytics. We also help them create unique idea generation screens that are customized to their approach, using Uniform Accounting and our other analytics.

But for most of our institutional clients, the analysis that they find most useful, and almost universally ask for, is a quarterly portfolio audit and call with our analysts.

Our institutional clients pay a significant premium for all our bespoke research. Some of our institutional clients have paid well over $100,000 a year for our uniquely tailored Uniform Accounting research, because of the value it adds to their process.

Until Thanksgiving, we’re making a special offer.

For any investor that buys access to the Valens Research app ($10,000/year subscription), we will include an Institutional-level portfolio audit and call with our analyst team with no extra charge.

Also, for those people who sign up to the offer before end of day on November 15th, we’ll include one year of access to all of our newsletters, including our Market Phase Cycle™ and Conviction Long Idea List (a $6,000 value), for no extra charge.

We want to help show you how powerful Uniform Accounting research can be for your investment strategy.

If you want to hear more about this offer, or are interested in subscribing, feel free to reply to this email. I’ll forward your note to our head of client servicing. Or, feel free to reach out to Doug Haddad, the head of our client relations team, at doug.haddad@valens-securities.com or at 630-841-0683.

To read more about the offer and sign up, you can also click here.

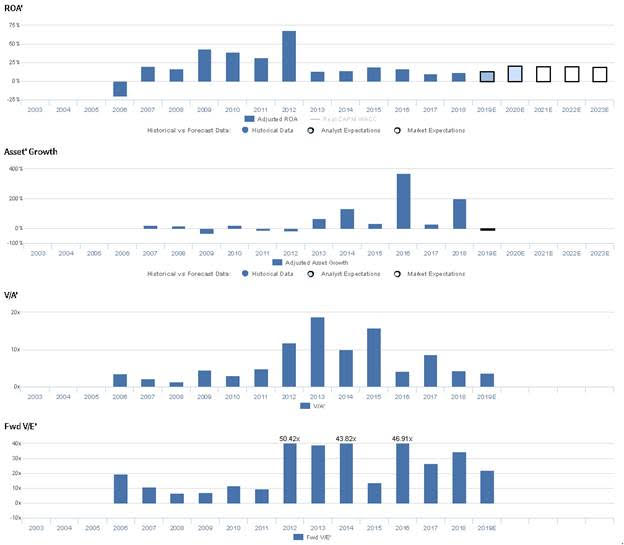

Markets are pricing in expectations for Uniform ROA to expand, and management is confident about their growth and margins

GTT currently trades above corporate averages relative to UAFRS-based (Uniform) Earnings, with a 22.2x Uniform P/E. At these valuations, the market is pricing in expectations for Uniform ROA to rise from 12% in 2018 to 20% by 2023, accompanied by immaterial Uniform Asset growth going forward.

However, analysts have even more bullish expectations, projecting Uniform ROA to rise to 21% by 2020, accompanied by 6% Uniform Asset shrinkage.

GTT has historically seen cyclical profitability, with Uniform ROA improving from -20% in 2006 to 68% in 2012, before falling to 10%-19% levels from 2013 to 2018. Meanwhile, Uniform Asset growth has been volatile, ranging from -34% to 369% since 2007, driven by the firm’s acquisition of a number of competitors in the space.

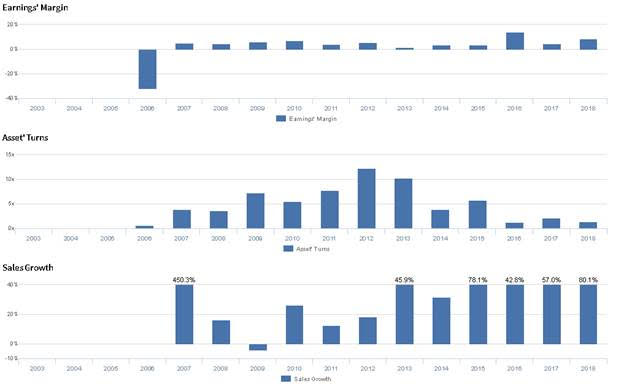

Performance Drivers – Sales, Margins, and Turns

Cyclicality in Uniform ROA have been driven by cyclicality in Uniform Asset Turns, and to a lesser extent, trends in Uniform Earnings Margin. Uniform Asset Turns improved from 0.6x in 2006 to 12.2x in 2012, before falling to 1.4x in 2018. Meanwhile, Uniform Margins improved from -32% in 2006 to 1%-7% levels from 2007 to 2015. Then, Uniform Earnings Margin improved to 14% in 2016, before falling to 5% in 2017 and reversing to 8% in 2018. At current valuations, markets are pricing in expectations for improvement in both Uniform Margins and Uniform Turns.

Earnings Call Forensics

Valens’ qualitative analysis of the firm’s Q2 2019 earnings call highlights that management is confident that their focus is on accelerating organic rep-driven growth, and they are confident in their ability to return to organic growth in the future. Furthermore, they are confident in their ability to drive additional growth and margin expansion. However, they may lack confidence in their ability to sustain year-over-year EBITDA growth and larger sales volumes. Furthermore, they may be concerned about continued weakness in their churn rate, and they may lack confidence in their ability to forecast capex. Finally, they may be concerned about the value of their goodwill and free cash flow.

UAFRS VS As-Reported

Uniform Accounting metrics also highlight a significantly different fundamental picture for GTT than as-reported metrics reflect. As-reported metrics can lead investors to view a company to be dramatically stronger or weaker than real operating fundamentals highlight. Understanding where these distortions occur can help explain why market expectations for the company may be divergent.

As-reported metrics significantly understate GTT’s profitability. For example, as-reported ROA for GTT was near 2% levels in 2018, materially lower than Uniform ROA of 12%, making GTT appear to be a much weaker business than real economic metrics highlight. Moreover, as-reported ROA has sustained 2%-4% levels from 2009 to 2018, while Uniform ROA has fallen from 43% to 12% during this time, directionally distorting the markets perception of the firm’s profitability since the Great Recession.

Today’s Tearsheet

Today’s tearsheet is for Comcast. Comcast trades in line with market averages. However, at current valuations, the market is pricing in no material Uniform EPS going forward. The company has historically has robust Uniform EPS growth, though it is forecast to be more intermittent going forward. The company’s earnings growth and valuations are around peer averages. While the company has healthy profitability, they will need to manage obligations to avoid any issues with their maintaining their dividend.

Regards,

Joel Litman

Chief Investment Strategist