The mistake Alexander Fleming and rating agencies both made

Some of the greatest innovations in the past have occurred by accident. It may be a good thing this type of success is much harder to repeat in today’s environment, though.

Today’s firm is a niche player providing lab instruments to prevent accidental discoveries in the medical field.

The rating agencies are showing a lack of understanding for this firm’s credit risk, barely rating it as Investment Grade.

Also below, the company’s Uniform Accounting Performance and Valuation Tearsheet.

Investor Essentials Daily:

Wednesday Credit Insights

Powered by Valens Research

One of the greatest innovations in the healthcare industry was the confirmation of the antibiotic properties of penicillin. This innovation can be attributed to the work of Alexander Fleming in 1928, when a mold accidentally grew on a culture of staph bacteria. The mold ended up killing the bacteria.

The revolution of antibiotics changed the quality of life dramatically for the human race. Nowadays, this type of lucky breakthrough is unlikely to happen thanks to the higher standard for safety and cleanliness in research.

Stringent measures have been brought into effect across the healthcare industry and other life sciences work such as food and agriculture. All said, this raised standard is a net positive.

Higher safety standards are vital for development, production, and testing. If these precautions are not followed, any data gathered cannot be trusted and will put the public’s safety and wellbeing at risk.

Agilent Technologies (A) is one company central to providing the technology to safely study and control this type of research. Since Agilent lives at the heart of the booming medical research industry, the firm has been an impressively profitable company.

The types of accidental discoveries Fleming and other scientists of old made may be a thing of the past. Today’s research industry is highly regulated, and Agilent acts as a supplier to keep all research within bounds.

However, the company is barely rated as an investment grade by Moody’s, with a Baa2 rating.

This does not appear to reflect the firm’s economic reality and how its core position has allowed the company to generate resilient cash flows.

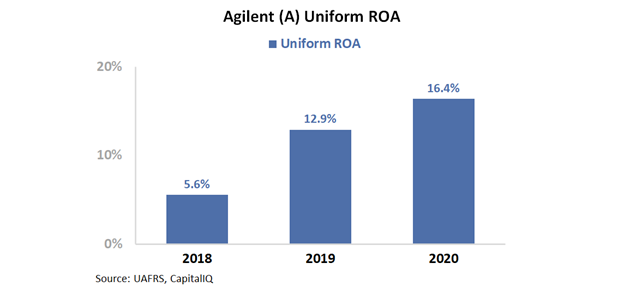

Agilent generated $1.3 billion in earnings, which translates to a robust 16% Uniform return on assets (ROA) last year.

With how essential Agilent is to its industry, it is capable of surviving mostly on its cash flows alone, with only $1 billion of debt coming due within the next five years.

Our Credit Cash Flow Prime (CCFP) analysis is able to show the minimal credit risk for the company.

In the below chart, the stacked bars represent the firm’s obligations each year for the next five years. These obligations are then compared to the firm’s cash flow (blue line) as well as the cash on hand at the beginning of each period (blue dots) and available cash and undrawn revolver (blue triangles).

As depicted, Agilent has massive cash liquidity and therefore should have no issues handling its obligations going forward. On top of this, even if the firm did not have access to this capital, cash flows alone exceed all operating obligations by a wide margin every year including 2022 and 2025, when the firm has debt maturities.

Rather than a name in distress, Agilent is actually a cash flow machine. Using the CCFP analysis, Valens rates Agilent as an investment grade IG3+ safe credit rating.

This rating corresponds to a default rate just above 1% within the next five years, a more realistic projection once a holistic understanding of the company’s risk is taken into account.

Ultimately, Uniform Accounting and the Credit Cash Flow Prime analysis highlight how Agilent’s credit risk profile is much safer than what rating agencies believe.

By using Uniform Accounting, investors have the proper context to understand whether market yields for bonds really make sense, or provide opportunities for investment.

SUMMARY and Agilent Technologies, Inc. Tearsheet

As the Uniform Accounting tearsheet for Agilent Technologies, Inc. (A:USA) highlights, the Uniform P/E trades at 31.2x, which is above the global corporate average of 25.2x and its historical average of 26.8x.

High P/Es require high EPS growth to sustain them. In the case of Agilent, the company has recently shown a 37% Uniform EPS growth.

Wall Street analysts provide stock and valuation recommendations that in general provide very poor guidance or insight. However, Wall Street analysts’ near-term earnings forecasts tend to have relevant information.

We take Wall Street forecasts for GAAP earnings and convert them to Uniform earnings forecasts. When we do this, Agilent’s Wall Street analyst-driven forecast is a 14% and 13% EPS growth in 2020 and 2021, respectively.

Based on the current stock market valuations, we can use earnings growth valuation metrics to back into the required growth rate to justify Agilent’s $120.17 stock price. These are often referred to as market embedded expectations.

The company needs Uniform earnings to grow by 10% per year over the next three years to justify current stock prices. What Wall Street analysts expect for Agilent’s earnings growth is above what the current stock market valuation requires in 2020 and 2021.

Furthermore, the company’s earning power is 3x the corporate average. Also, cash flows and cash on hand are almost 3x its total obligations—including debt maturities, capex maintenance, and dividends. Together, this signals a low credit and dividend risk.

To conclude, Agilent’s Uniform earnings growth is in line with peer averages and the company is trading in line with peer average valuations.

Best regards,

Joel Litman & Rob Spivey

Chief Investment Strategist &

Director of Research

at Valens Research