A long-term focus on the right macro metrics shows why this market is deeply undervalued

With recent market volatility, many investors are overly focused on the short term when they should be focusing on long-standing macroeconomic drivers that will drive stocks.

Today, we look back through history to see how taxes and inflation dictate market valuations and think about what that means as the market stabilizes.

Investor Essentials Daily:

The Monday Macro Report

Powered by Valens Research

With the nearly unprecedented levels of market volatility, general uncertainty, and fear, it is essential to take a rational look at the market.

Ultimately, here at Valens, we’re trying to make sense of the long-term data rather than get caught up in current market volatility.

We don’t know what the total earnings impact COVID-19 will have on the economy, but we do know that the macro signals say we should be able to handle it.

Corporations still have flexibility with their debt. The cost to borrow is still historically low (adjusted for a lower risk-free rate). Consumers had healthy balance sheets going into this issue. Credit markets are still open.

In addition, we’re in one of the best environments for achieving peak market valuations, which is one of the reasons this most recent bull market lasted for so long.

With the Federal Reserve currently in the spotlight and the presidential election coming up later in the year, this is a great time to understand how changes in taxes and inflation can impact market valuations.

Even though it’s easy to measure the returns in your stock portfolio, that’s not the same as the “real” return you get as an investor. The actual money that ends up in your wallet, the “real” return, is impacted by both taxes and inflation rates.

We can begin with a thought experiment:

Imagine you invest in a stock that generates a 10% return in a year. That year, the Fed matches its 2% inflation target.

Right off the bat, this means inflation eats away 2% of your total or “nominal” returns, leaving you with 8%.

Next, factor that you have to pay a capital gains tax when you want to cash in on your portfolio.

Currently, the highest tax bracket for long-term capital gains and dividends happens to be 20%, meaning in isolation it has the same impact as inflation, leaving the investor with an 8% return rather than 10%.

However, these two variables don’t work in isolation—they compound.

In our experiment, a 2% inflation and 20% capital gains tax would transform a 10% nominal gain to a 6.4% real return.

But if inflation or taxes were lower—or if both were—the real after-tax return would be higher.

Throughout history, inflation and capital gains tax have varied quite a bit. That said, both happen to be on the low end of historical values, and this is a big factor as to why the most recent bull run was historically long.

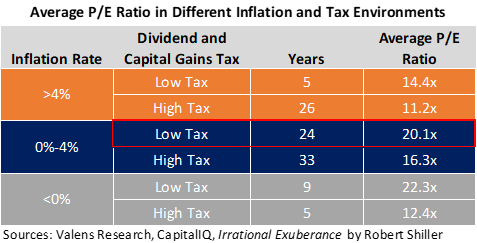

The chart below highlights market valuations under different types of inflationary and tax environments, with our current environment outlined in red.

We’re currently in one of the most historically optimal environments for high market valuations.

After the recent market volatility, as-reported P/E is 17.2x, and Uniform P/E is 17.6x—well below what average valuation levels are for this market environment..

As we’re beginning to see the market stabilize, we will be closely tracking how the Federal Reserve plans to continue inflation targeting, and we’ll continue monitoring how the presidential race may impact capital gains taxes.

In the long-run, these factors will be more powerful in understanding the strength of our next bull market. And why fundamentals warrant much higher market valuations.

Best regards,

Joel Litman & Rob Spivey

Chief Investment Strategist &

Director of Research

at Valens Research