A Nobel Prize winner wants you to think the market is still expensive, Uniform Accounting highlights the market’s multiple is very cheap

All of our analysis starts with adjusted financial metrics. However, not all adjusted financials are equally useful.

Today, we see how a Nobel Prize winner’s prized formula may be less useful than many investors realize.

And how it misrepresents current market valuations.

Investor Essentials Daily:

The Monday Macro Report

Powered by Valens Research

If you regularly read Investor Essentials Daily, you’ve likely noticed all of our analysis uses our proprietary accounting framework, UAFRS, also known as Uniform Accounting.

We don’t try to hide our frustration with as-reported accounting. The differences between GAAP and IFRS are nearly immeasurable, especially when you consider how just about every country using IFRS applies a slightly different version of the standard.

All said, we make approximately 130 adjustments to as-reported accounting statements to convert them to Uniform Accounting.

In some specific cases, we then have to make additional manual adjustments to make profitability comparable across time.

Many of the biggest and most successful investment firms in the world are making the exact same adjustments as us.

Some of them have hired benches of lifelong accounting practitioners, PhDs in math and quantitative economics, and seasoned academics to help restate the financial statements for use in investing.

That being said, we disagree with a few of the preeminent academic theories in economics, especially when they misunderstand the accounting they use to make their assumptions.

In fact, we happen to disagree with one of the most widely used “adjusted” accounting metrics, created by Yale professor Robert Shiller.

Shiller, who won the Nobel Memorial Prize in Economics in 2013, created what he thought was a superior version of the typical P/E ratio.

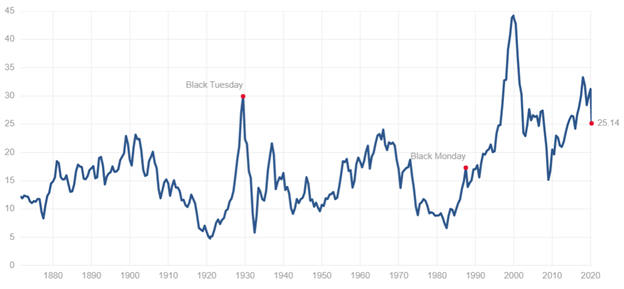

In his 2000 book, Irrational Exuberance, Shiller minted the new ‘cyclically-adjusted P/E ratio’, often referred to as CAPE or the Shiller P/E.

However you refer to it, the concept is that traditional P/E ratios tend to be too volatile because they only consider one year of corporate earnings at a time. This means one catastrophic year like 2008 or 2009 can send valuations out of whack—in other words, valuations are overly-impacted by economic and business cycles.

The Shiller P/E takes current share prices divided by a moving average of the past 10 years of earnings.

To Shiller’s credit, this helps to address a fundamental issue with normal P/E during times of recession.

As we saw during 2008-2009, as-reported P/Es reached historically high levels just as earnings were at their lowest. These are contradictory signals—high P/Es should mean the market is expensive, but the market had just fallen by as much as 56%.

CAPE reduces the impact of one bad year of earnings, as you can see in the following chart showing CAPE for the last 150 years.

That’s a good start, but it’s far from the most important flaw of as-reported P/E.

Just like as-reported P/E, the Shiller P/E makes use of as-reported earnings. There’s a “garbage-in, garbage-out” problem going on here.

If the underlying data is unreliable, distorted, or otherwise wrong, it’s not meaningful to smooth that data.

Furthermore, Shiller P/E uses the last 10 years of earnings. If you’ve ever taken a finance class or read a book on investing, you’ve probably learned that stock prices are based on what investors think companies are going to do in the future, not what they’ve done in the past.

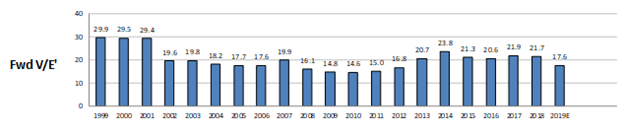

That’s why our Uniform P/E (V/E’) makes use of Uniform forward earnings.

Looking in that context, 2008 and 2009 valuations were very cheap relative to history.

Similarly, valuations right now haven’t dropped to “expensive” levels from “very expensive” levels, they’ve dropped to exceptionally cheap levels relative to history.

It’s tough to reconcile all of the reasons why we don’t think Shiller P/E is a useful valuation tool, but we hope this is useful food for thought to consider that just because a metric is “adjusted” doesn’t mean it’s valuable.

All the best, as always,

Joel Litman & Rob Spivey

Chief Investment Strategist &

Director of Research

at Valens Research